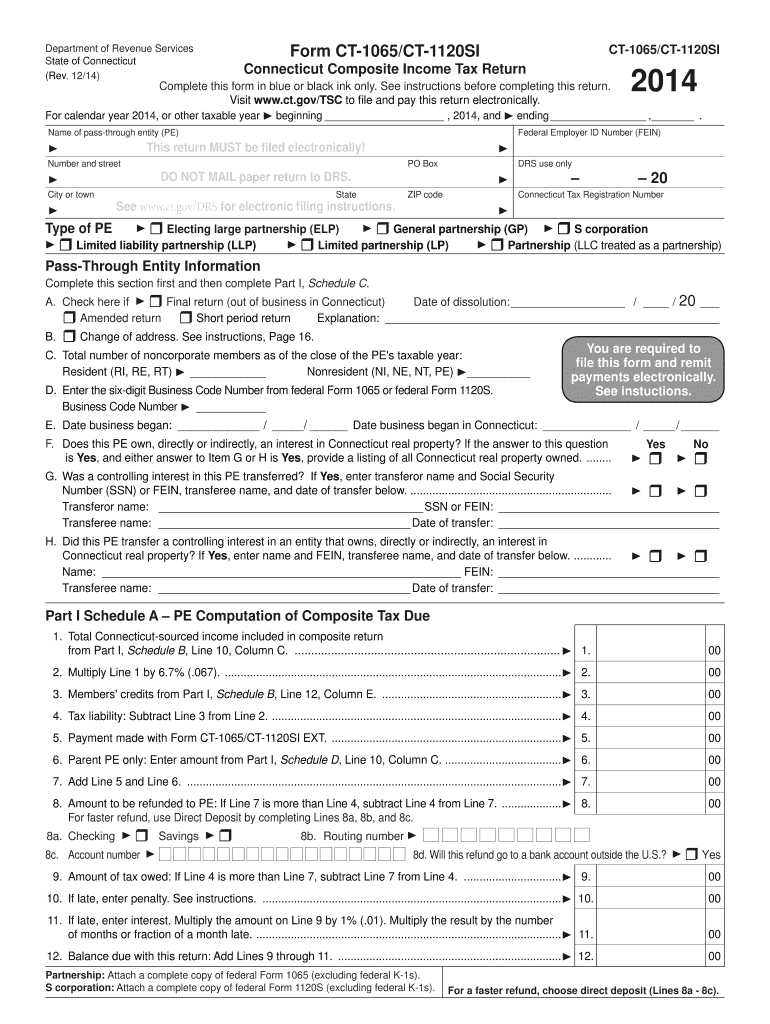

Understanding the 2014 CT-1065 Form

The 2014 CT-1065/CT-1120SI form is the Connecticut Composite Income Tax Return used by pass-through entities such as partnerships and S corporations. It facilitates the reporting of Connecticut-source income on behalf of nonresident members. This form ensures that entities accurately compute taxes and provide necessary member information for compliance with state tax laws.

How to Use the 2014 CT-1065 Form

- Determine Eligibility: Identify if your business qualifies as a pass-through entity and has nonresident members subject to Connecticut-source income tax.

- Collect Member Information: Gather relevant data for all members, including names, addresses, and tax identification numbers.

- Calculate Income: Accurately report Connecticut-source income attributable to each member.

- Compute Tax Liabilities: Use the form to determine the tax liabilities of the entity and its members.

Obtaining the 2014 CT-1065 Form

- Obtain the form from the Connecticut Department of Revenue Services (DRS) website.

- Contact the DRS customer service for mailed copies if electronic access is not feasible.

Steps to Complete the 2014 CT-1065 Form

- Enter Entity Details: Fill in the name, address, and federal employer identification number of the business.

- Report Income: Detail each member’s share of Connecticut source income.

- Provide Attachments: Include any required schedules or supporting documents such as K-1s.

- Review Calculations: Double-check the computations to ensure accuracy in tax liability.

Who Typically Uses the 2014 CT-1065 Form

- Partnerships: Entities with shared profits between partners in different residencies.

- S Corporations: Corporations electing to pass income directly to shareholders to avoid double taxation, with shareholders residing outside Connecticut.

Important Terms Related to the 2014 CT-1065 Form

- Pass-Through Entity: A business structure where income is passed directly to owners or investors, avoiding corporate income tax.

- Nonresident Member: An owner or partner who resides out-of-state but earns income from a Connecticut-based business.

- Composite Income Tax: A tax on the collective income reported by pass-through entities.

Filing Deadlines and Important Dates

- Original Filing Deadline: Aligns with federal partnership tax returns, typically mid-March.

- Extended Filing: Extensions are available but must be accurately filed before the original deadline.

Legal Use of the 2014 CT-1065 Form

- The form legally mandates accurate disclosure of income and tax liabilities.

- Complying with form instructions protects against penalties for non-compliance. Failure to file or incorrect submissions could invite scrutiny by the Connecticut DRS.

Key Elements of the 2014 CT-1065 Form

- Income Sourcing and Allocation: Detailed instructions for reporting Connecticut-source income per member.

- Tax Calculation: Instructs on computing aggregate taxes owed by nonresident members.

- Disclosure Requirements: Details every member's involvement and respective tax liabilities.

Examples of Using the 2014 CT-1065 Form

- Partnerships Operating Nationwide: Utilizing the form to ensure compliance with both state and federal tax obligations.

- S Corporations with Diverse Shareholder Base: Correct reporting and submission to avoid audit triggers.

Filing Methods for the 2014 CT-1065 Form

- Online Filing: Preferred method through the Connecticut DRS online portal for direct submission and quicker processing.

- Mail Submission: Acceptable but may take longer for processing and confirmation; ensure postage is dated before the deadline.

Penalties for Non-Compliance

- Late filing or misreporting can result in fines or collection actions by the state.

- Amended returns are better than non-filing, providing an avenue to correct errors and minimize penalties.