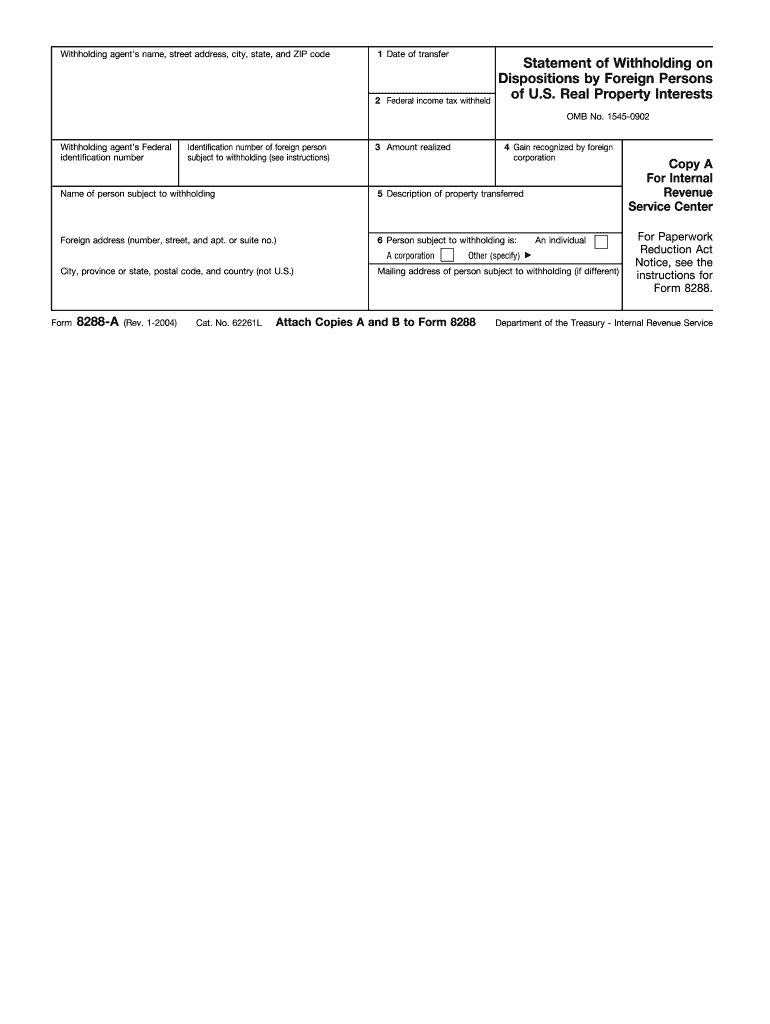

Definition and Purpose of Form 8288-A

Form 8288-A, Rev January 2004, is a critical document used by withholding agents when reporting the withholding tax on dispositions of U.S. real property interests by foreign persons. This form is associated with the Internal Revenue Service (IRS) regulations and ensures compliance with tax obligations related to the sale or transfer of specific real estate properties involving foreign sellers. It provides essential information for both the IRS and the involved parties regarding the amount of tax withheld.

- Objective: To document withholding amounts on real property transactions involving non-U.S. residents.

- Audience: Primarily used by withholding agents, which may include real estate brokers, attorneys, or realtors involved in these transactions.

- Revisions: Updates reflect changing IRS requirements and ensure up-to-date compliance.

How to Use Form 8288-A

Form 8288-A serves as a report and receipt for the withholding of income tax when non-resident aliens or foreign entities sell U.S. real property interests. Understanding the proper use of this form is crucial for ensuring legal compliance.

- Recording Transactions: Withholding agents must complete Form 8288-A during transactions involving foreign sellers to record tax withholdings accurately.

- Providing Copies: The withholding agent submits the form to the IRS and provides copies to the foreign seller for their records.

- Role of the Realtor: Realtors play a significant role in facilitating the completion and submission of the form, ensuring all parties have the necessary information.

Steps to Complete Form 8288-A

Accurate completion of Form 8288-A requires attention to detail and a clear understanding of the necessary information. Here's a guide on how to fill it out:

- Enter Basic Information: Begin with the seller's name, address, and taxpayer identification number (TIN).

- Identify the Buyer: Provide the buyer's information, including their TIN if applicable.

- Specify the Property: Include details about the property sold, such as location and description.

- Calculate Withholding: Accurately enter the amount of tax withheld based on IRS-recommended rates.

- Sign and Date: The withholding agent must sign and date the form to validate its authenticity.

Who Typically Uses Form 8288-A

Form 8288-A is used by several key players involved in real estate transactions when non-U.S. persons are sellers:

- Withholding Agents: These can be real estate brokers, closing attorneys, or any party responsible for closing the real estate transaction.

- Foreign Sellers: Non-U.S. resident individuals or entities need this form as it provides proof of tax withheld.

- U.S. Buyers: Though not the typical user, they should be aware of the form's role in the transaction process.

Key Elements of Form 8288-A

Familiarity with the main components of Form 8288-A is essential for effective execution:

- Seller and Buyer Information: Essential for identifying the parties involved in the transaction.

- Property Description: Ensures that the correct property is associated with the withholding.

- Tax Withholding Amount: Critical for both the IRS and the seller to know the exact amount of tax applied to the transaction.

Filing Deadlines and Important Dates

Compliance with specific deadlines is necessary to ensure the proper filing of Form 8288-A:

- Submission Timeline: Generally, the form must be submitted to the IRS within 20 days of the date of transfer of the property.

- Copy to the Seller: Provide the foreign seller with their copy within the same period to ensure they have the documentation needed for their records.

Penalties for Non-Compliance

Failure to comply with the guidelines regarding Form 8288-A can result in significant penalties:

- Financial Penalties: Withholding agents may face fines for late filing, incorrect calculations, or failure to remit proper withholding to the IRS.

- Legal Repercussions: Non-compliance could lead to further IRS actions, including collections or audits, impacting the agent and involved parties.

IRS Guidelines for Form 8288-A

The IRS provides specific instructions for accurately completing and submitting Form 8288-A, which are essential for legal compliance:

- Tax Rates: The IRS specifies the withholding tax rates applicable to different types of transactions.

- Filing Procedures: Detailed steps are outlined by the IRS for both initial submission and amendments if corrections are necessary.

- Withholding Certificate: There are processes for applying for a withholding certificate if the seller seeks an adjustment to the withheld amount based on exemptions or overpayments.

Understanding and adhering to these guidelines and aspects ensures that all parties involved in property transactions with foreign sellers fulfill their tax and legal obligations efficiently.