Understanding Pension Income Splitting in Canada

Pension income splitting in Canada allows eligible spouses or common-law partners to jointly elect to allocate up to 50% of eligible pension income to the other partner for tax purposes. This strategy can help reduce the overall tax burden for a couple by taking advantage of the lower tax bracket of one spouse.

Eligibility Criteria

- Age Requirements: At least one of the spouses or partners must be eligible to receive pension income as defined by Canadian tax laws.

- Form Submission: Both partners need to agree on the split and submit joint election forms along with their individual tax returns.

- Income Types: Eligible income often includes periodic payments from pensions and registered retirement income funds (RRIFs).

Key Elements of Pension Income Splitting

- Maximum Split: Couples can elect to split up to 50% of eligible pension income.

- Tax Implications: The splitting doesn’t affect overall income but reallocates income for tax purposes, potentially lowering the tax rate.

- Agreement Requirement: Both partners must consent to the elected split, and it must be properly documented in their tax filings.

Steps to Complete the Pension Income Splitting Process

- Determine Eligibility: Verify that both partners meet the criteria.

- Calculate Split Amount: Decide on the portion of the pension income to be split.

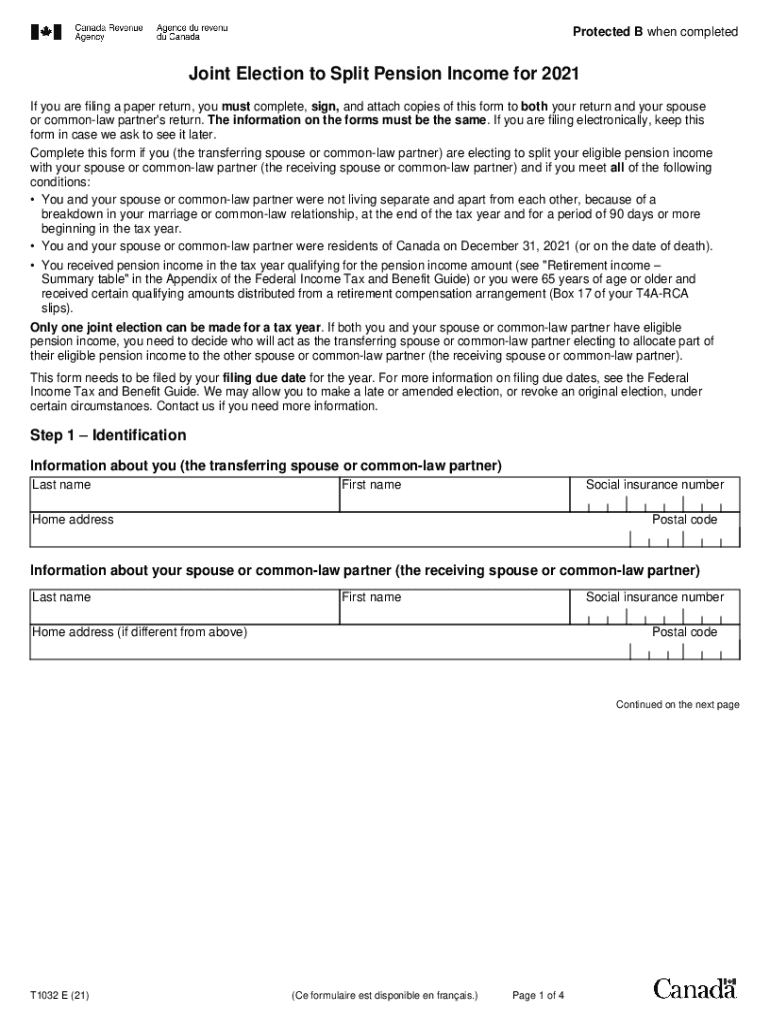

- Fill Out Necessary Forms: Complete the T1032 Joint Election to Split Pension Income form.

- Submit with Tax Returns: Attach the completed form to each partner's annual tax return submission.

- Review and Finalize: Double-check figures and ensure both partners' tax returns reflect the elected split.

Legal Use and Compliance

The use of pension income splitting must adhere to the guidelines set out by the Canada Revenue Agency (CRA). Failure to comply can result in penalties and interest charges. It's crucial to maintain accurate records supporting the election and to submit completed schedules with tax returns.

Important Terms Related to Pension Income Splitting

- Pension Income: Includes various retirement income streams that qualify for splitting.

- Joint Election: The formal agreement and election filed by both partners.

- RRIF: Registered Retirement Income Fund, a type of income often included in splitting.

Filing Deadlines and Important Dates

- Tax Season Timeline: Ensure all forms related to pension splitting are submitted by the standard tax filing deadline of April 30th.

- Extension Possibilities: Extensions may be available under certain circumstances, but specific requirements must be met for consideration.

Examples of Using Pension Income Splitting

- Scenario 1: Spouse A has a high pension income while Spouse B has minimal individual retirement income, splitting would reduce the combined tax liability.

- Scenario 2: Both partners have similar pension incomes but different marginal tax rates, allocation might still benefit due to credits or deductions.

Penalties for Non-Compliance

- Financial Penalties: Incorrect filings can lead to additional taxes, interest, and sizable penalties.

- Adjustment Audits: CRA may conduct audits that can result in adjustments to previously filed returns if non-compliance is detected.

By understanding and efficiently navigating the pension income splitting process, eligible Canadians can optimize their tax situation and enhance their retirement income strategy.