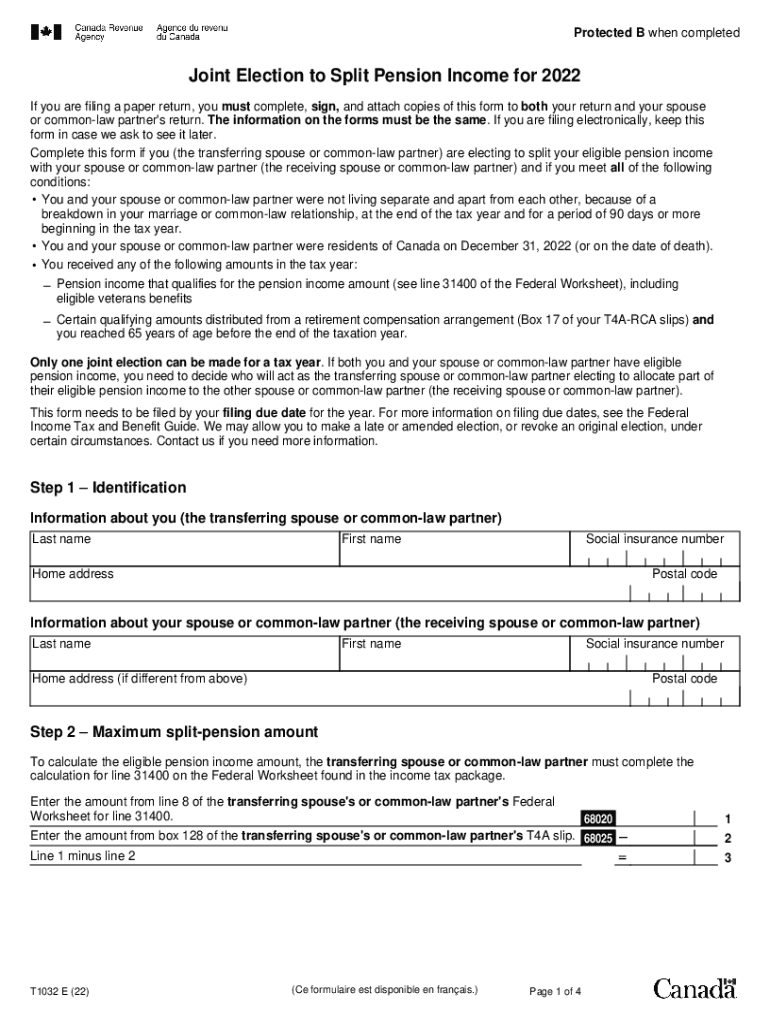

Understanding Pension Income Splitting

Pension income splitting is a financial strategy that allows married couples or common-law partners to share up to 50% of their eligible pension income. This approach helps optimize the couple's tax situation by shifting income from the higher-earning partner's tax bracket to the lower-earning partner's bracket, potentially reducing the overall tax liability. Couples who utilize this method may achieve tax savings by taking advantage of the progressive nature of the tax system in the United States.

Eligible Income Sources

- Private pensions: Typically include qualified retirement plans like 401(k)s and IRAs.

- Government pensions: Social security benefits can be considered, although specific tax treatments apply.

- Annuities: Payments received from certain annuities may qualify for splitting.

- Exclusions: Some sources, like foreign pensions or non-registered savings, may not be eligible.

Steps to Split Your Pension Income

- Determine eligibility: Verify that both partners meet the criteria, such as being residents for tax purposes and not being separated due to a relationship breakdown.

- Gather necessary documents: Collect statements from all pension sources to understand the total income available for splitting.

- Calculate the splitable amount: Identify the maximum amount of pension income that can be shifted. Typically, up to 50% is allowed.

- Complete tax preparation documents: Utilize a tax software or consult a tax professional to ensure the information is processed correctly.

- Submit with tax return: Ensure that the election to split income is declared in both partners' tax returns.

Legal Considerations and Compliance

Pension income splitting is governed by specific tax regulations. It is vital to comply with all legal requirements to avoid any complications or penalties.

Key Legal Aspects

- Joint election requirement: Both partners must agree and choose to split the pension income in their tax filings.

- Documentation: Maintain thorough records of pension income sources and the agreed split percentage.

- Potential audits: Ensure accuracy in documentation and reporting, as discrepancies could lead to audits and subsequent penalties.

Eligibility Criteria for Pension Income Splitting

Eligibility hinges on meeting specific criteria determined by the tax authorities and can vary slightly based on jurisdiction.

Core Eligibility Requirements

- Marital status: Must be legally married or in a recognized common-law partnership for tax purposes.

- Tax residency: Both partners must be considered as tax residents of the United States.

- Qualification of pension income: Only income from eligible pension sources can be split.

Key Terms in Pension Income Splitting

Understanding the terminology associated with pension income splitting can clarify the process and obligations involved.

Relevant Terms

- Spouse/Common-law partner: Defined for tax purposes as individuals living in a recognized partnership or marriage.

- Qualified pension income: Includes government and private pensions that meet criteria for inclusion in the split.

- Tax residency: Status determining the tax obligations and benefits in the United States.

Practical Examples of Pension Income Splitting

Exploring real-world scenarios where pension income splitting applies can provide insight into its advantages and practical application.

Example Scenarios

- Scenario A: John and Mary, with John as the primary income earner, use pension splitting to lower their joint tax liability.

- Scenario B: Retiree couple Tom and Sarah maximize their tax benefits by shifting income from Tom’s higher tax bracket to Sarah’s lower bracket.

Form Submission Methods and Deadlines

Submitting the appropriate tax documentation on time is crucial for implementing pension income splitting.

Submission and Timing

- Methods: Forms can typically be submitted online through authorized e-filing systems or via mail with physical forms.

- Deadlines: Must submit with annual tax returns by the tax filing deadline, generally April 15th in the United States.

Differences Between Digital and Paper Versions

Choosing between digital and paper methods of managing pension splitting can affect convenience and efficiency.

Comparing Methods

- Digital Submissions: Offer quicker processing, confirmation of receipt, and the convenience of online filing.

- Paper Forms: May be preferred for individuals who require physical evidence or have inadequate access to digital services.

IRS Guidelines and Compliance

The IRS provides comprehensive guidelines that taxpayers must follow to ensure proper handling and compliance when splitting pension income.

Compliance Overview

- Adherence to IRS rules: All information related to pension income must align with IRS guidelines to be accepted in tax filings.

- Updates and changes: Taxpayers should stay informed on annual changes to tax laws that may impact pension income splitting strategies.

By following these guidelines and thoroughly understanding each aspect of pension income splitting, taxpayers can make informed decisions that may lead to significant tax savings while ensuring compliance with all relevant regulations.