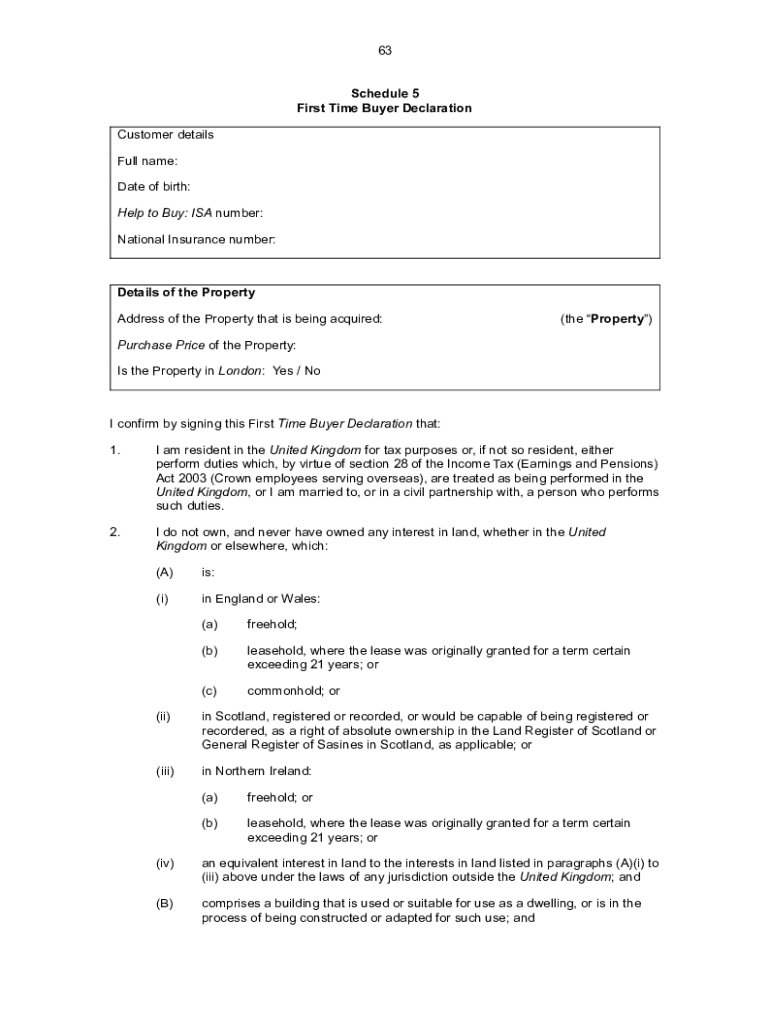

Understanding the Help to Buy: ISA Scheme

The Help to Buy: ISA scheme is designed to assist first-time buyers in acquiring property through savings incentives. It offers a government bonus on contributions made into a special savings account. This scheme is vital for those seeking financial support in entering the property market. Understanding its nuances, including eligibility criteria and application processes, is crucial for prospective users.

Eligibility Criteria for the Scheme

To qualify for the Help to Buy: ISA scheme, applicants must meet specific requirements:

- Be a first-time homebuyer

- Be at least 16 years old

- Have a valid National Insurance number

- Be a resident of the UK These criteria ensure that the scheme targets the right demographic, allowing those at the start of their home ownership journey to benefit.

Steps to Complete the Form

Completing the Help to Buy: ISA scheme form involves several steps:

- Gather necessary personal details, including residency status and previous property ownership.

- Fill out the form with accurate information regarding the property and the buyer's intent to use it as a primary residence.

- Review the form for any errors or incomplete sections.

- Submit the form through the designated channel, ensuring adherence to deadlines.

Required Documents for Submission

Applicants must provide documentation to support their application:

- Proof of identity (passport or driver's license)

- Evidence of residency

- Bank statements or proof of savings This step ensures all information is verified, aiding in a smoother approval process.

Purpose and Benefits of the Scheme

The Help to Buy: ISA scheme is primarily used to:

- Provide financial aid to first-time buyers

- Encourage savings through government bonuses

- Facilitate home ownership for younger individuals or those with limited financial history The underlying purpose is to lessen the financial burden associated with purchasing a home, making it more accessible for those who might otherwise struggle.

Common Use Cases

Typical users of the scheme are:

- Young adults entering the housing market

- Individuals transitioning from rental properties to ownership

- Residents seeking government-assisted financial plans These groups benefit from the tailored financial support offered by the scheme, allowing for more strategic financial planning and savings growth.

Important Terms Related to the Scheme

Familiarity with key terminology enhances understanding and compliance:

- ISA: Individual Savings Account, a tax-free savings option.

- Government Bonus: A 25% bonus on savings contributed to the ISA.

- Residency Status: Verification of the applicant's living status in the UK. These terms are integral to the scheme's operational framework, supporting transparency and informed decision-making.

Examples of Using the Help to Buy: ISA

To illustrate practical application:

- A recent graduate opens a Help to Buy: ISA, saving £200 per month. After two years, they use the government bonus to increase their deposit when buying a modest apartment.

- A couple uses their separate Help to Buy: ISAs to pool savings and bonuses, amplifying their deposit capability for a larger home. Such examples demonstrate the adaptive use of the scheme for varying financial situations, emphasizing its versatility.

Legal Use and Compliance

To legally use the Help to Buy: ISA scheme, adhere to these guidelines:

- Maintain truthful declarations regarding property ownership and residency

- Use the government bonus strictly for its intended purpose during property purchase Failure to comply may result in penalties, impacting eligibility for future government schemes. Users must be diligent in understanding and following the regulations to avoid legal repercussions.

Penalties for Non-Compliance

Not adhering to the scheme's rules can lead to:

- Disqualification from receiving the government bonus

- Repayment of bonuses received under false pretenses These penalties underscore the importance of accuracy and honesty in the application process.

Obtaining the Form

Obtaining the Help to Buy: ISA scheme form involves:

- Visiting the designated institutional or government website

- Requesting a physical copy from participating banks

- Accessing the form through financial advisors or real estate consultants This accessibility ensures that all eligible individuals can easily initiate their application process.

Form Submission Methods

Applicants can submit their completed form through various channels:

- Online platforms associated with bank accounts or financial services

- Directly mailing the form to designated addresses

- In-person submission at participating banks These options provide flexibility, allowing applicants to choose the most convenient method for submission.

Versions and Alternatives to the Scheme

Although the Help to Buy: ISA scheme targets specific needs, alternatives exist for those who do not qualify:

- Lifetime ISA: A broader savings plan with similar benefits for house purchases or retirement savings.

- Shared Ownership Schemes: Allowing purchase of part of the property and paying rent on the remainder, suited for various financial capacities. Understanding these alternatives ensures that potential applicants explore available options effectively, making informed decisions tailored to their financial goals.