Definition and Meaning

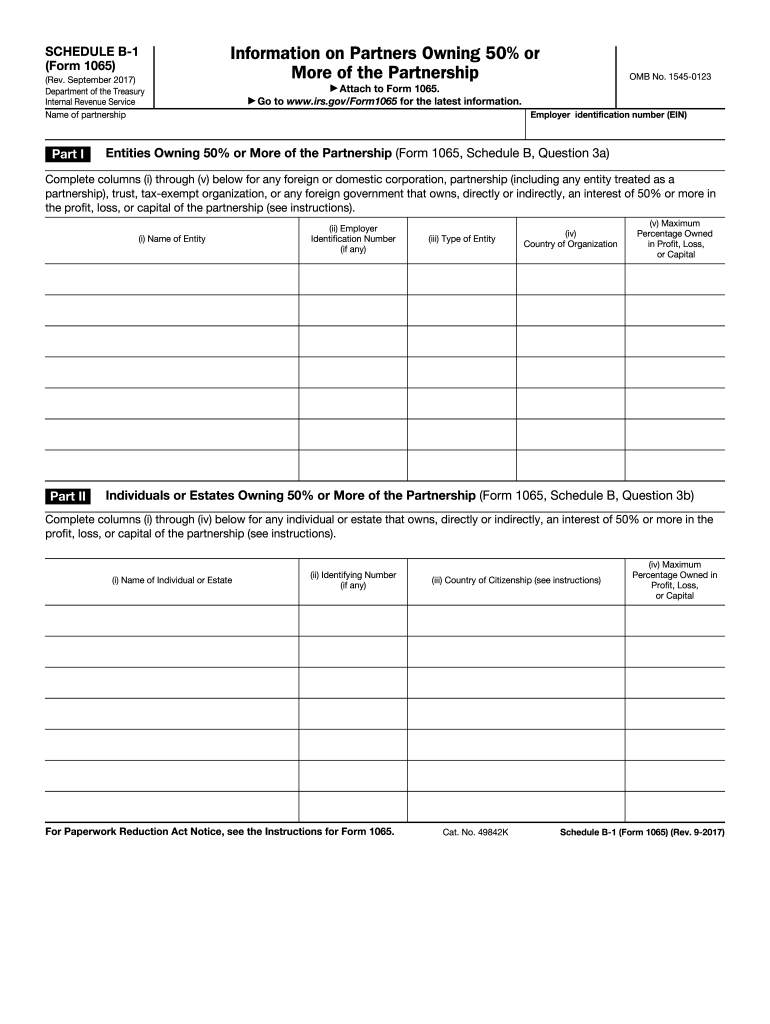

Schedule B-1 (Form 1065) is a document used by partnerships to report the details of partners owning 50% or more of the profit, loss, or capital. This form is crucial for maintaining transparency about substantial ownership interests within partnerships, ensuring that such information is disclosed to the Internal Revenue Service (IRS) as part of compliance requirements. The form includes sections that require detailed information about the entities or individuals meeting this ownership threshold.

Purpose of the Schedule B-1

The primary purpose of Schedule B-1 is to provide the IRS with an accurate reflection of ownership distribution among partners in a partnership. By disclosing specific details about significant stakeholders, the form helps safeguard against tax evasion and ensures comprehensive compliance with federal tax laws. It also assists in the accurate allocation of income, expenses, and credits among partners.

Important Terms Related to Schedule B-1 Instructions

Understanding the terminology related to Schedule B-1 is crucial to accurately completing and filing the form. Key terms include:

- Partnership: An arrangement where two or more entities manage and operate a business in accordance with agreed terms.

- Partner's Share: Refers to the proportion of profit, loss, and capital that each partner is entitled to according to the partnership agreement.

- Threshold Percentage: The percentage of ownership (50% or more) that requires partners to be reported on Schedule B-1.

- K-1 Form: Another IRS form used by partnerships to report each partner's share of income, deductions, and credits.

Steps to Complete the Schedule B-1 Instructions

Properly completing the Schedule B-1 form involves several critical steps:

-

Identify Partners: Begin by identifying all partners who hold 50% or more of the partnership's profit, loss, or capital.

-

Gather Information: Collect detailed information on each applicable partner, including name, address, and taxpayer identification number (TIN).

-

Accurate Documentation: Ensure all reported information is accurate and reflects the current ownership percentages as stipulated in the partnership agreement.

-

Review and Verify: Double-check the completed form for any errors or omissions that might trigger compliance issues or IRS audits.

-

Attach to Form 1065: Once completed, attach Schedule B-1 to the partnership's Form 1065 for submission to the IRS.

Particular Considerations

-

Multiple Partnerships: Partnerships that are part of a tiered arrangement or hold interests in multiple partnerships should carefully assess each entity's ownership to determine filing requirements.

-

Amendments: If ownership changes occur, consider whether an amended return is necessary to correct previously submitted information.

Penalties for Non-Compliance

Failure to complete and submit Schedule B-1 accurately can result in significant penalties. The IRS imposes fines for underreporting ownership stakes as part of broader efforts to enforce compliance. Partnerships may also face additional scrutiny or audits, leading to potential corrections and penalties.

Common Pitfalls

Some common mistakes that lead to penalties include:

-

Omitting Owners: Failing to disclose any partner meeting the 50% threshold.

-

Incorrect Information: Providing inaccurate or outdated information regarding partner ownership.

-

Late Filings: Submitting Schedule B-1 past the deadline without prior extensions.

Digital vs. Paper Version

There are both digital and paper versions of Schedule B-1. Many filers prefer digital submissions due to the convenience and efficiency provided by electronic filing platforms, particularly for large partnerships with complex ownership structures.

Benefits of Digital Submission

-

Speed and Accuracy: Electronic submissions are often faster and reduce the chance of errors.

-

Record-Keeping: Digital systems provide better record-keeping capabilities, allowing partnerships to maintain detailed electronic copies of all filings.

Challenges

- Technology Requirements: Entities must ensure they have compatible software and digital signatures for secure electronic submission.

IRS Guidelines

The IRS provides comprehensive guidelines on how to correctly complete and file Schedule B-1. These guidelines are essential for understanding specific requirements and ensuring compliance.

Sources of Official Information

-

IRS Website: The primary source for up-to-date forms and filing instructions.

-

Publication 541: Offers in-depth tax information for partnerships, including details pertinent to Schedule B-1.

Updates and Alerts

Partnerships should regularly review updates from the IRS, especially in the context of changing tax laws or instructions that might affect the filing requirements for Schedule B-1.

Filing Deadlines and Important Dates

Schedule B-1 is typically filed alongside Form 1065 by the 15th day of the third month following the end of the partnership's tax year. This can vary for partnerships with fiscal years differing from the calendar year.

Extensions and Considerations

-

Extension Requests: Partnerships can apply for extensions if more time is needed to prepare accurate filings. This allows additional leeway while ensuring compliance.

-

State Requirements: Some states may have specific deadlines or additional filing obligations, which should be considered alongside federal requirements.

Business Entity Types and Variations

While Schedule B-1 is specific to partnerships, understanding the nuances related to different business entity types is important.

Eligible Entities

-

LLCs: Limited Liability Companies classified as partnerships for tax purposes must file Schedule B-1 if they meet the ownership criteria.

-

Corporations: Traditional corporations (C and S Corps) have different reporting requirements and do not utilize Schedule B-1.

Comparative Scenarios

Entities should carefully evaluate their classification and tax obligations to understand how Schedule B-1 fits into their broader tax filings and compliance strategy.