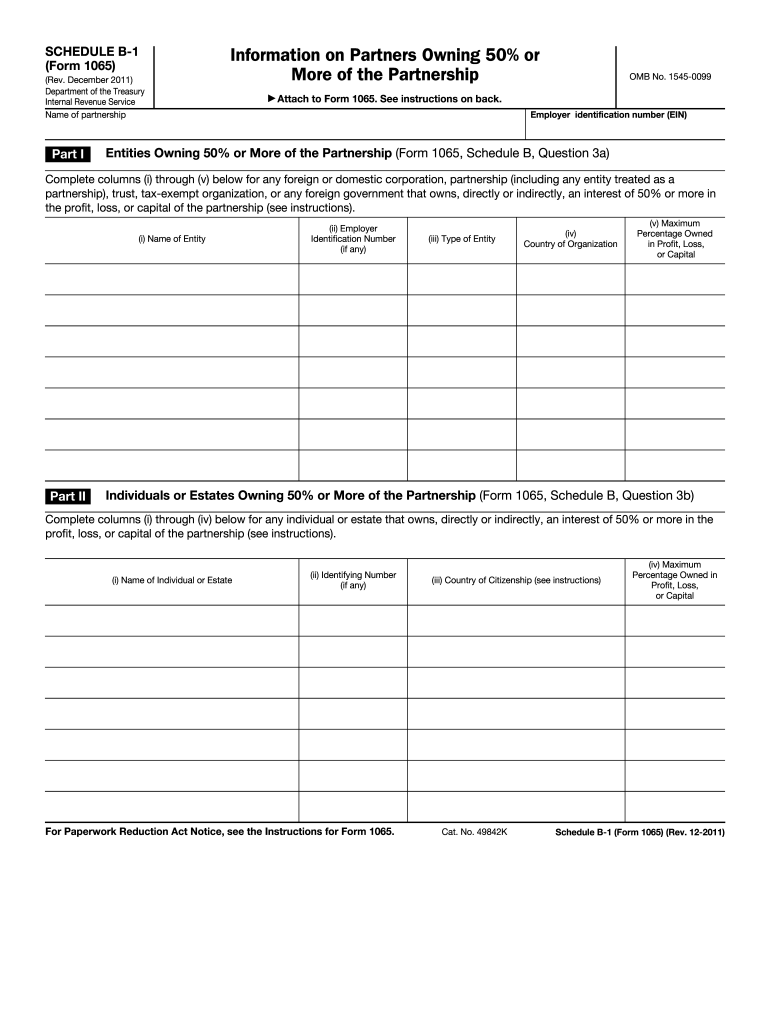

Definition & Meaning

Form B-1 from 2011, a crucial document within the IRS framework, serves as a detailed reporting tool primarily used by business entities for compliance purposes. This form is essential for documenting significant financial arrangements, especially for partnerships required to disclose financial dealings. On Form B-1, 2011, entities must provide in-depth information about their fiscal operations, income distributions, or details on ownership changes in compliance with IRS mandates.

How to Use Form B-1 2011

Utilizing Form B-1, 2011 correctly involves a systematic approach to ensure all required information is accurately presented. Form users should focus on detailing financial transactions and partnerships, specifying data such as profit distribution percentages and capital ownership. Business entities can streamline the completion process by ensuring each section is thoroughly filled out, double-checking for any applicable tax regulations and requirements. Moreover, users should verify their entries against IRS guidelines to confirm the integrity and completeness of the information provided.

Steps to Complete the Form B-1 2011

-

Gather Required Information: Collect all necessary documentation related to partnership agreements, ownership interests, and financial transactions.

-

Fill Out Basic Details: Enter fundamental details, including taxpayer identification numbers and registered addresses.

-

Report Financial Data: Provide detailed financial disclosures, including ownership percentages and changes in partnership interests.

-

Review IRS Guidelines: Consult IRS instructions specific to Form B-1 to ensure compliance with reporting standards.

-

Double-Check Entries: Recheck each entry for accuracy and completeness to avoid discrepancies or omissions.

-

Submit the Form: Use the chosen method of submission, ensuring it aligns with IRS rules for timeliness and format.

Key Elements of Form B-1 2011

In Form B-1, 2011, several key components demand careful attention. These include sections clarifying partners' financial stakes, identifying shifts in partner interests, and accurately documenting fiscal transactions. By aligning each entry with IRS stipulations, users can enhance the form's efficacy in achieving compliance objectives. Key areas often require additional scrutiny to ensure data is both comprehensive and precise, minimizing the risk of non-compliance.

Who Typically Uses Form B-1 2011

Primarily used by partnerships and corporations that require detailed reporting of profit or capital interest changes, Form B-1, 2011, acts as an essential compliance instrument. This form is invaluable for businesses needing to submit information on major financial stakeholders, particularly those with a fifty percent or higher share in profits or losses. This ensures accountants, tax preparers, and corporate administrators rely heavily on Form B-1 for accurate record keeping and regulatory adherence.

Important Terms Related to Form B-1 2011

- Partnership Interest: Refers to the stake that partners hold in a business, directly affecting their profit or loss entitlements.

- Profit-Sharing Agreement: A legal arrangement detailing how profits are distributed among partners.

- Capital Account: Represents a partner’s equity in a business, often reflecting their investment and retained earnings.

- Compliance: Adhering to legal standards and guidelines set forth by the IRS regarding business and partnership disclosures.

IRS Guidelines

The IRS provides comprehensive guidelines for completing Form B-1, 2011, focusing on correct reporting of financial arrangements and compliance with federal tax legislation. These guidelines stress the importance of accuracy and transparency in financial disclosure, assisting users in maintaining adherence to taxation laws. Consulting these guidelines ensures users approach form completion effectively, mitigating risks associated with incomplete or erroneous filings.

Filing Deadlines / Important Dates

Adhering to filing deadlines is critical for the timely submission of Form B-1, 2011. Typically, deadlines align with the tax filing dates of the parent business entity, often corresponding to the March 15 or April 15 deadlines, depending on whether individuals are filing as part of a partnership or corporation. These important dates serve as key milestones within the tax calendar, guiding users in timely documentation and submission endeavors.

Penalties for Non-Compliance

Failure to comply with the IRS regulations regarding Form B-1, 2011, attracts significant penalties, affecting both individuals and business entities. Potential repercussions include monetary fines and potential legal scrutiny, contingent on the severity and nature of violations. Ensuring form accuracy and timely submission are indispensable in mitigating these risks and maintaining regulatory compliance.