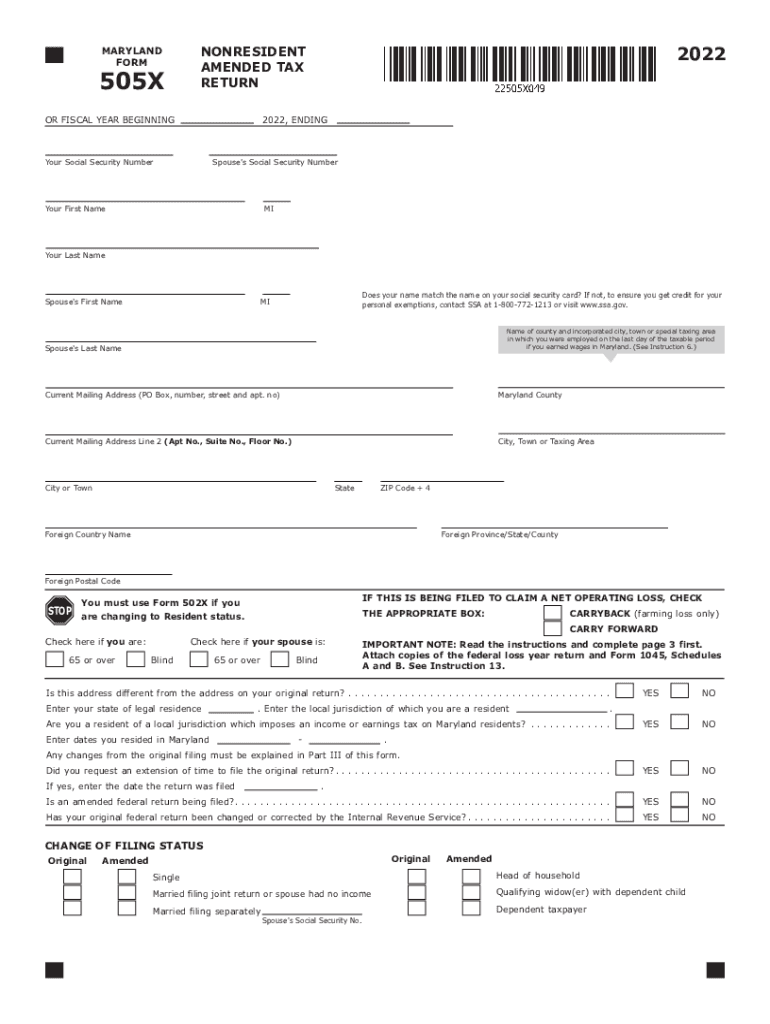

Definition & Meaning of the Form 505X49 011023 A

Form 505X49 011023 A, often abbreviated to 505X49, refers to a specific type of document pertinent to nonresident amended tax returns in the United States. Primarily used for Maryland's state tax system, it serves as a means for taxpayers to correct or update their previously filed income tax returns. This form includes several sections to accurately capture changes to income, deductions, credits, and other essential details required by the state's tax authorities.

How to Use Form 505X49 011023 A

To effectively utilize the form, taxpayers should follow these steps:

- Review Your Original Tax Return: Examine the initial return you filed to identify areas that need correction.

- Identify Modifications: Clearly outline the adjustments you wish to make, such as changes in income, new deductions, or recalculated credits.

- Complete the Form: Fill in the amended details in the corresponding sections of the 505X49 form. Ensure all calculations and data entries are double-checked for accuracy.

- Attach Supporting Documents: If necessary, include additional forms or documentation to substantiate your amendments.

- Submit the Form: Follow the designated submission method, whether it be mailing the document or uploading it through an online tax filing system.

Commonly, individuals who discover discrepancies or omissions in their previously filed tax returns use this form to ensure compliance and accuracy in their tax obligations.

Steps to Complete Form 505X49 011023 A

Effectively navigating the completion of the form involves detailed attention to each of its components:

- Section 1: Personal Information: Provide accurate details, including your name, contact information, and social security number.

- Section 2: Income Changes: Record any changes in reported income and attach any relevant documentation for substantiation.

- Section 3: Adjustments and Deductions: List and justify any new deductions or adjustments to previously reported amounts.

- Section 4: Tax Credits: Amend any credit claims, ensuring accuracy with supporting evidence.

- Final Review and Submission: Confirm the information is accurate and complete before submitting the form to the appropriate tax authority.

Each step should include a meticulous review process to prevent errors that could lead to delays or complications.

State-Specific Rules for Form 505X49 011023 A

Maryland has unique requirements for the completion and filing of this form:

- Timeframe for Submission: Taxpayers must file an amended return within three years of the original filing date or two years from the date the tax was paid, whichever is later.

- State-Specific Tax Credits: Certain credits are unique to Maryland residents and must be accurately reflected.

- Attachments Required: Maryland may require additional documents such as state-specific forms or proof of residency.

Who Typically Uses Form 505X49 011023 A

The form is essential for:

- Nonresidents with Maryland Income Sources: Individuals who do not principally reside in Maryland but have state-source income.

- Taxpayers Discovering Errors: Those who need to correct mistakes on previously filed returns.

- Applicants for Additional Credits/Deductions: Individuals who qualify for added benefits after the initial submission.

Legal Use of Form 505X49 011023 A

Legally, the form must be used to report accurate changes to previously submitted state tax returns. Incorrect or fraudulent use can lead to penalties, including fines or legal action. It is vital that any amendments are honest and verifiable.

Examples of Using Form 505X49 011023 A

Consider these scenarios:

- Scenario 1: Income Increase: An independent contractor earns additional income post-filing and uses the form to report the expansion.

- Scenario 2: New Deduction Opportunities: Discovering eligibility for a state-specific educational deduction prompts amending the original tax return.

- Scenario 3: Credit Adjustment: A taxpayer becomes aware of eligibility for a credit previously unclaimed.

These real-world situations highlight how and why taxpayers might need to file amended returns using Form 505X49.

Filing Deadlines / Important Dates

The standard deadline is three years from the original tax return filing date. If paying additional tax, ensure timely payment to avoid interest or penalties. It is crucial for taxpayers to observe these deadlines to maintain compliance and avoid unnecessary penalties.

Penalties for Non-Compliance

Failing to file an amended return when required or submitting incorrect information can lead to penalties, including:

- Financial Penalties: Fines based on the amount of tax owed.

- Interest Fees: Accrual of interest on unpaid taxes detected after initial filing.

- Legal Consequences: Potential legal proceedings for fraudulent reporting.

Taxpayers must ensure submissions are punctual and accurate to mitigate these risks.