Definition & Meaning

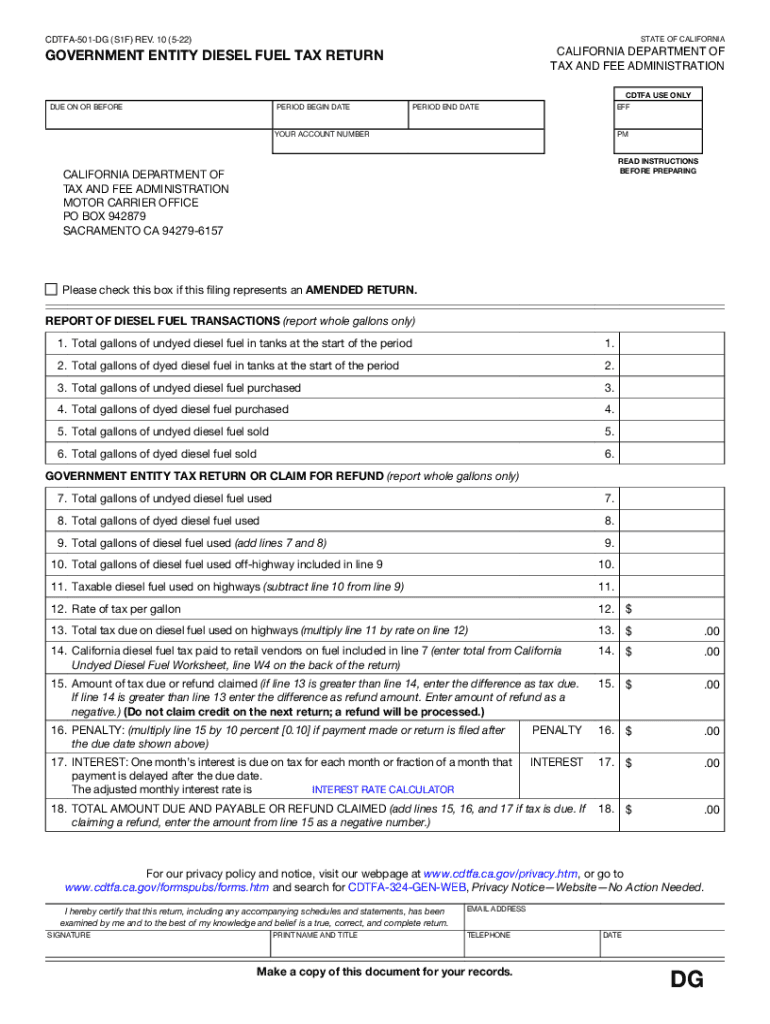

The "Form CDTFA-501-DG Government Entity Diesel Fuel Tax Return" is a specific document issued by the California Department of Tax and Fee Administration (CDTFA). It is designed to facilitate the reporting and payment of diesel fuel taxes by government entities. This form ensures that these entities accurately document their use of both undyed and dyed diesel fuel in motor vehicles operated on California highways. The form's primary objective is to maintain compliance with the state's taxation policies, ensuring that all applicable taxes are duly recorded and remitted.

Key Elements of the Form CDTFA-501-DG

Reporting Fuel Transactions

- Undyed vs. Dyed Fuel: The form distinguishes between undyed diesel, typically used for standard vehicular purposes, and dyed diesel, which is often used for non-standard purposes such as agricultural machinery. Accurate reporting for both types is crucial.

- Volume and Purchases: Entities must provide detailed accounts of the total volume of diesel fuel purchased and used.

- Exemptions and Refunds: If applicable, the form allows for claiming exemptions or refunds, necessitating precise documentation and adherence to stipulations.

Tax Calculations

The form includes comprehensive sections for the calculation of tax dues or refunds. Both require meticulous input to ensure that the government entity is either paying the correct tax amount or claiming an accurate refund based on their diesel usage.

Steps to Complete the Form CDTFA-501-DG

- Gather Required Documentation: Collect all receipts, transaction records, and additional documents detailing diesel fuel purchases and usage.

- Complete Personal Information: Enter the government entity's identification and contact information precisely as registered with the CDTFA.

- Fuel Usage Reporting:

- List detailed transactional data regarding diesel purchases, specifying quantities for undyed and dyed diesel.

- Ensure that exemptions, if any, are presented with supporting documentation.

- Tax Calculation:

- Use the form's calculation sections to determine the total tax amount due or refundable, based on reported diesel usage.

- Double-check computations to prevent errors.

- Review and Submit: Go through the completed form for accuracy before submission. Rectify any inconsistencies found.

Important Terms Related to Form CDTFA-501-DG

- Dyed Diesel: A fuel type prohibited from use in vehicles on public highways due to the absence of highway taxes. Used predominantly for non-commercial purposes.

- Undyed Diesel: Regular diesel requiring standard taxation for use on public roads.

- Government Entity: Any department, agency, or unit at the state or local level employing the form for tax compliance.

Who Typically Uses the Form CDTFA-501-DG

This form is primarily intended for use by government entities within California, ranging from state agencies to local municipal offices. These entities routinely operate vehicles that require diesel fuel for daily operations, thereby necessitating regular tax reporting.

Legal Use of the Form CDTFA-501-DG

Adhering to the legal framework surrounding this form is essential for compliance with California's tax regulations. Accurately reporting diesel usage on Form CDTFA-501-DG ensures that government entities abide by the law, mitigating potential legal disputes or penalties for tax evasion or misreporting.

Filing Deadlines / Important Dates

- Regular Reporting: Typically, government entities need to file this form on a quarterly basis.

- Due Dates: Submissions are generally due shortly after the close of each calendar quarter. It is critical to verify specific deadlines to prevent late submissions, which may incur penalties.

Penalties for Non-Compliance

Failing to submit the Form CDTFA-501-DG on time or submitting inaccurate information can result in fines and other regulatory penalties. Non-compliance can also lead to legal issues, highlighting the importance of timely and precise reporting.

Form Submission Methods

- Online Submission: Government entities can submit the Form CDTFA-501-DG through the CDTFA's official online portal for convenience and efficiency.

- Mail Submission: For traditional procedures, entities can mail the completed form and any accompanying documentation to the CDTFA. Checking for the most updated postal address is recommended.

- In-Person Submission: While less common, entities may choose to submit forms directly at a CDTFA office, ensuring immediate receipt confirmation.