Definition and Meaning of Schedule R (Form 990)

Schedule R (Form 990) is a critical document used by organizations to report their relationships with related entities to the IRS. It serves to disclose information about affiliations with disregarded entities, related tax-exempt organizations, partnerships, corporations or trusts, and any inter-entity transactions. This form ensures transparency in financial interactions and organizational relationships throughout the tax year. By detailing these associations, Schedule R helps maintain compliance with IRS regulations and facilitates a clear understanding of an organization’s operational structure.

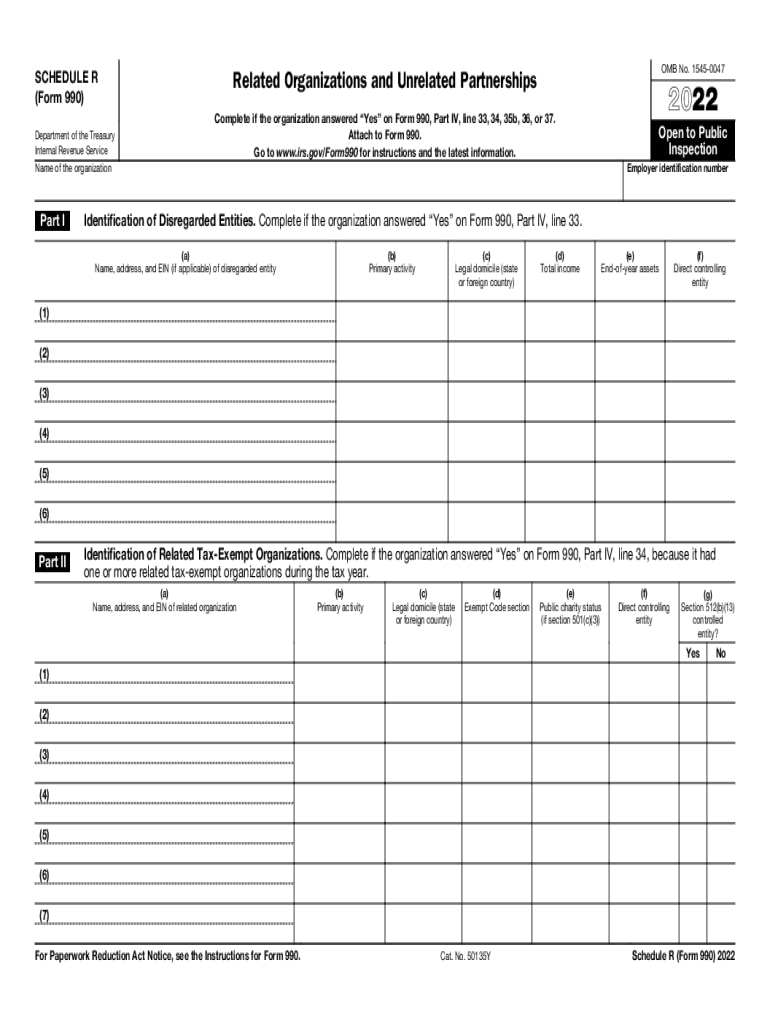

How to Use Schedule R (Form 990)

Schedule R should be utilized by tax-exempt organizations that engage with related entities. The form requires comprehensive reporting on every entity the organization has a relationship with, detailing financial interactions, shared resources, and any substantial control or influence exerted over interconnected organizations.

- Section 1: Document disregarded entities and their contributions.

- Section 2: Report financial and operational exchanges with related tax-exempt organizations.

- Section 3: Detail partnerships, corporations, or the trusts that are related to your organization.

- Section 4: Highlight any significant transactions, specifying the nature and magnitude of those exchanges.

Each section of Schedule R must be completed accurately to ensure IRS compliance and avoid potential audits or penalties.

Obtaining Schedule R (Form 990)

Organizations can access Schedule R (Form 990) directly from the IRS website, where it is available for download in PDF format. To ensure the information is up-to-date and correctly formatted, users should verify they are downloading the latest version of the form, which is typically designated by the publication year. Additionally, tax software platforms generally offer integrated access to Schedule R, streamlining the process for users of those services.

Steps to Complete Schedule R (Form 990)

Completing Schedule R involves several detailed steps:

- Identify Related Entities: Review all entities that your organization interacts with to determine those that qualify as related.

- Gather Required Information: Compile financial data, operational details, and any agreements reflecting inter-entity relationships.

- Fill Out Relevant Sections: Complete each part of the form that pertains to different entity types:

- Disregarded Entities (Section 1)

- Related Organizations (Section 2)

- Partnerships and Trusts (Section 3)

- Transactions (Section 4)

- Review and Verify: Double-check the form for accuracy, ensuring all required fields are filled and information provided is consistent with organizational records.

Who Typically Uses Schedule R (Form 990)

Schedule R is predominantly used by tax-exempt organizations that have extensive interactions with other entities. These entities include:

- Nonprofits with subsidiary organizations.

- Charities engaged in partnerships or joint ventures.

- Educational institutions with franchised or subsidiary campuses.

Such relationships often necessitate full disclosure to maintain compliance and organizational transparency.

Key Elements of Schedule R (Form 990)

Some of the key components of Schedule R that require specific focus include:

- Disregarded Entities: Single-member LLCs that are accounted for as part of the parent organization.

- Controlled Organizations: Entities under substantial control or influence by the filer.

- Transaction Details: Specifics on financial or material exchanges, including loans, leases, or other agreements, ensuring comprehensive disclosure.

IRS Guidelines for Schedule R (Form 990)

The IRS provides detailed guidelines on completing Schedule R, emphasizing full disclosure of all related transactions and ensuring the inclusion of all relevant financial data. Organizations must adhere to these guidelines to prevent discrepancies and ensure a smooth filing process. The IRS mandates accurate representation of inter-entity dealings, which can significantly impact tax assessments and organizational oversight.

Filing Deadlines and Important Dates for Schedule R (Form 990)

The Schedule R form must be submitted alongside Form 990 by the 15th day of the fifth month following the organization’s fiscal year-end. For many organizations, this deadline falls on May 15. However, extensions can be requested using Form 8868, which provides additional time for submission, usually an extra six months.

Penalties for Non-Compliance

Failing to accurately complete and file Schedule R can result in significant penalties. The IRS imposes fines for omissions, errors, or any fraudulent intentions. Penalties may include monetary fines and, in severe cases, the revocation of tax-exempt status. Organizations must ensure meticulous completion and timely submission to avoid these consequences.