Understanding the 2022 M1LTI Long-Term Care Insurance Credit

The 2022 M1LTI, Long-Term Care Insurance Credit, is a form used by Minnesota residents to claim a credit related to long-term care insurance premiums on their state tax returns. This credit is available for eligible individuals who have paid premiums for qualifying long-term care insurance policies.

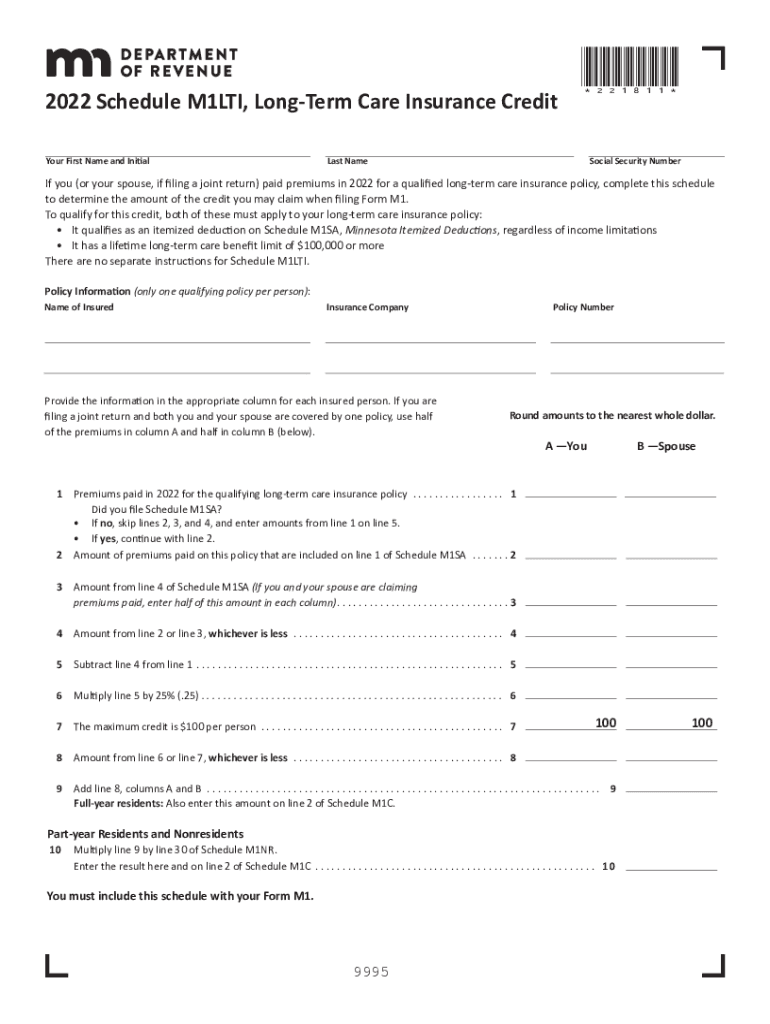

Eligibility Criteria for the 2022 M1LTI

Eligibility for the 2022 M1LTI Long-Term Care Insurance Credit requires that the insurance policy:

- Qualifies as an itemized deduction.

- Has a lifetime benefit limit of at least $100,000.

- Covers either the taxpayer or their spouse if filing jointly.

This means the policy must meet specific standards set by both the IRS and Minnesota state regulations.

Steps to Complete the 2022 M1LTI Form

- Gather Necessary Documents: Ensure you have all relevant documentation, such as policy statements and proof of premium payments.

- Download the Form: Obtain the M1LTI form from the Minnesota Department of Revenue’s website.

- Fill Out Personal Information: Include your full name, Social Security Number, and filing status.

- Enter Premiums Paid: On the specific lines provided, enter the total premiums paid during the tax year for the qualifying policy.

- Calculate the Credit: Follow the instructions on the form to compute your allowable credit based on the input data.

- Sign and Submit the Form: Ensure all information is accurate, sign the form, and submit it as part of your tax filing.

Important Terms Related to the 2022 M1LTI

- Itemized Deduction: A tax deduction for eligible expenses, which can include long-term care insurance premiums.

- Lifetime Benefit Limit: The maximum amount an insurance policy will pay over its existence, which must be at least $100,000.

- Qualifying Policy: An insurance policy that meets specified criteria defined by state tax regulations.

State-Specific Rules for Minnesota

In addition to meeting federal requirements, the Minnesota-specific guidelines dictate that:

- The claimant must be a resident of Minnesota for the tax year.

- The policy should comply with both state insurance standards and the IRS tax code.

How to Obtain the 2022 M1LTI Form

The 2022 M1LTI form can be downloaded from:

- The official website of the Minnesota Department of Revenue.

- Many tax preparation software platforms, such as TurboTax or QuickBooks, that support Minnesota state filings.

Filing Deadlines and Important Dates

- File the M1LTI form by the same deadline as your Minnesota state tax return, generally April 15th, unless special circumstances apply.

- Check for any extensions or changes to the tax filing deadline on the Minnesota Department of Revenue’s website.

Examples of Using the 2022 M1LTI

Consider a taxpayer who has paid $2,000 in premiums for a qualifying long-term care insurance policy during the tax year. By completing the 2022 M1LTI form, they can calculate their eligible credit and apply it toward reducing their state tax liability.

Penalties for Non-Compliance

Failing to comply with the requirements of the 2022 M1LTI form can result in:

- Denial of the credit claimed on your tax return.

- Possible penalties or interest on your tax due if incorrect or incomplete information is submitted.

Differences Between Digital and Paper Versions

While a paper version of the M1LTI form can be submitted, using an electronic version via approved e-filing services offers advantages:

- Faster processing times.

- Reduced likelihood of errors with built-in checks within tax software.

By thoroughly understanding and accurately completing the 2022 M1LTI Long-Term Care Insurance Credit form, taxpayers can take advantage of available credits, helping to lower their overall tax responsibility.