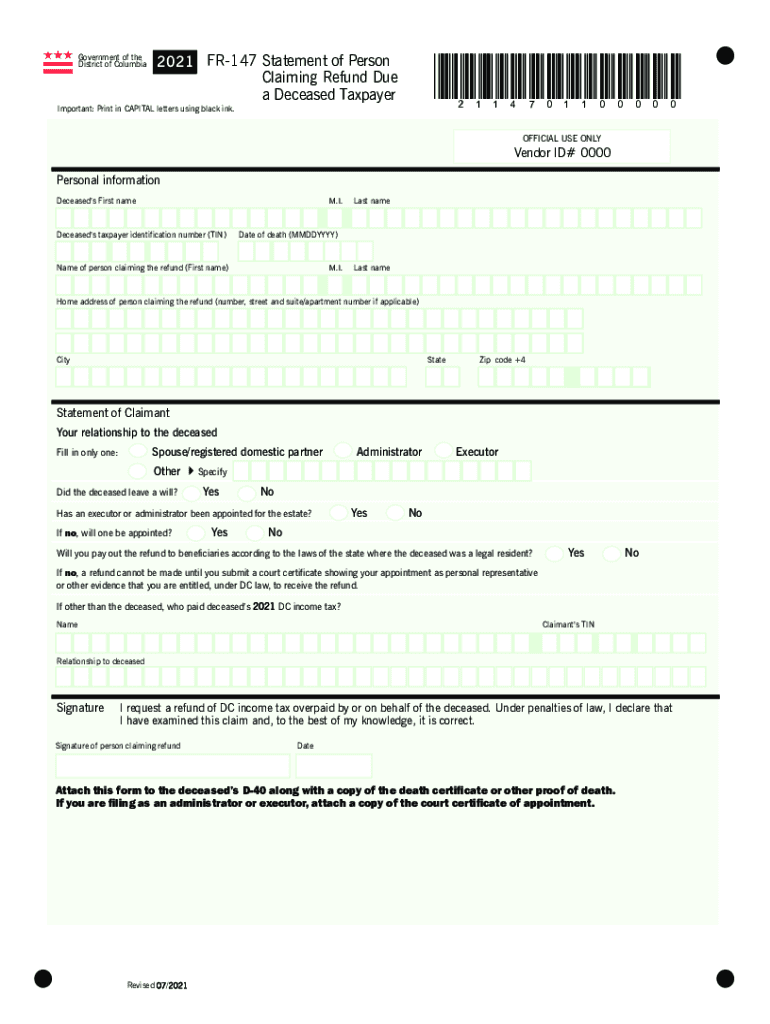

Definition and Purpose of DC Form FR-147

DC Form FR-147 is a specific document utilized by the Government of the District of Columbia to claim a tax refund for a deceased taxpayer. This form must be filled out by an individual who is legally entitled to request the refund on behalf of the deceased. The document serves not only to gather relevant information about the deceased taxpayer but also to establish the claimant's relationship to the deceased and confirm their legal authority to claim the refund. The form is pivotal in ensuring that the tax refund process complies with legal formalities and efficiently addresses the unique circumstances surrounding a deceased taxpayer's finances.

How to Use DC Form FR-147

Filling out the DC Form FR-147 involves a few critical steps to ensure accuracy and compliance with legal requirements:

-

Gather Required Information:

- Collect personal details about the deceased, such as full name, Social Security number, and date of death.

- Compile your personal information as the claimant, including contact details and relationship to the deceased.

-

Legal Authority Confirmation:

- If you are an executor or administrator, ensure that proof of your legal authority, such as a court order or letters testamentary, is available.

-

Document Submission:

- The completed form, along with necessary supporting documents like the death certificate and proof of executor status, should be filed with the appropriate tax authorities in the District of Columbia.

Ensure that each section of the form is thoroughly completed and all attachments are securely included to avoid delays in processing.

Obtaining DC Form FR-147

To obtain the DC Form FR-147, you can visit the official website of the Government of the District of Columbia, where the form is usually available for download. This ensures that you have the most current version of the form. Alternatively, you can request a paper copy from local DC tax offices if you prefer a physical document. Ensure you acquire this form from reliable sources to avoid discrepancies or submission issues.

Steps to Complete DC Form FR-147

Filling out the DC Form FR-147 involves adhering to specific procedural steps to ensure its proper completion:

-

Complete Personal Information Sections:

- Accurately fill in the personal details of the deceased and the claimant.

-

Attach Necessary Documentation:

- Include a copy of the death certificate along with any legal documents demonstrating your authority to act on behalf of the deceased.

-

Review and Finalize:

- Double-check all entered data for accuracy.

- Ensure all necessary signatures are present.

-

Submission:

- File the completed form and attachments through the prescribed channels, either online or via mail.

These detailed steps help facilitate a smooth process in applying for a tax refund on behalf of a deceased individual.

Required Documentation for DC Form FR-147

Submitting the DC Form FR-147 necessitates certain documentation, which is vital for validating the claim and processing the refund:

- Death Certificate: A certified copy is required to verify the status of the deceased.

- Proof of Executor or Administrative Authority: Documentation such as letters testamentary or court orders affirming your right to act on behalf of the deceased.

- Identity Verification: Your personal information, including a government-issued ID, may be required to validate your identity as the claimant.

These documents support your claim and ensure that the refund process abides by legal expectations.

Legal Use and Authority

The legal use of DC Form FR-147 is strictly to facilitate the claiming of tax refunds for deceased individuals. The form is used by parties who hold a legal obligation or authority to manage the deceased's affairs. Utilizing this form without proper authority can result in legal consequences, stressing the importance of having verifiable legal standing when filing the form.

Key Elements of DC Form FR-147

The DC Form FR-147 comprises several crucial elements that both the claimant and any involved parties must complete diligently:

- Deceased’s Information: This section records vital details about the deceased taxpayer.

- Claimant’s Certification: An area for the claimant to assert their relationship and right to file the form.

- Legal Authority Confirmation: This section requires evidence of the claimant's legal standing to represent the deceased.

Each element plays an integral role in ensuring the proper filing and submission of the form.

State-Specific Rules and Considerations

The rules governing the use of DC Form FR-147 are specific to the District of Columbia. While processes may share similarities with other states, the regulations and required submissions are tailored to fit the jurisdiction of DC. Claimants should ensure they are familiar with such local nuances, particularly if they have previously dealt with similar processes outside DC.

Examples of Scenarios Using DC Form FR-147

Several scenarios necessitate the use of the DC Form FR-147:

- Executor of a Will: An executor who needs to finalize the deceased's estate, including any outstanding tax matters.

- Surviving Spouse or Relative: A close family member responsible for settling the deceased's affairs.

- Court-Appointed Administrator: An individual appointed by the court to manage the deceased's estate.

Each scenario involves complex emotional and legal considerations, underscoring the importance of handling the form with care.

Filing Deadlines and Important Dates

Timely submission of the DC Form FR-147 is crucial:

- Deadline for Filing: Specific filing periods may apply post-death, and it is essential to consult the DC tax department for the exact timelines.

- Statutory Requirements: Filing deadlines might depend on the tax year in question and other jurisdictional regulations.

Observing these deadlines ensures the claim is processed efficiently without unnecessary delays.