Definition and Purpose of the PA-65

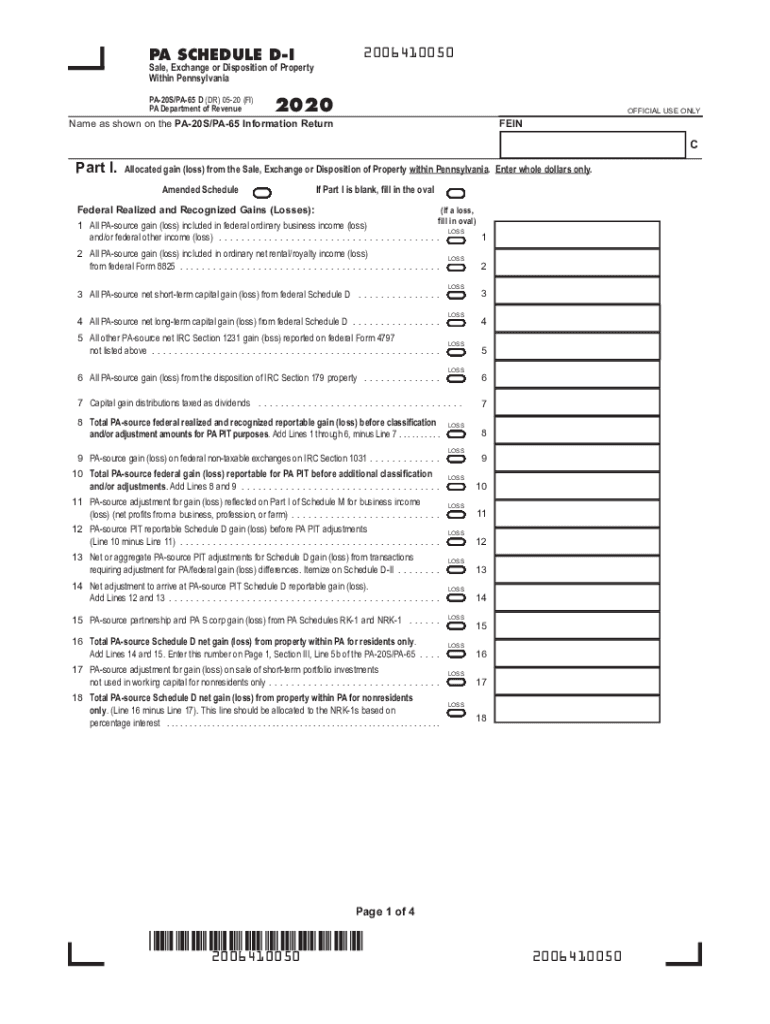

The "pennsylvania 65," commonly referenced as the PA-20S/PA-65, is a crucial document used by Pennsylvania S corporations, partnerships, and limited liability companies for reporting gains or losses from transactions involving property. Whether these transactions occur within or outside Pennsylvania, the form captures essential details to ensure compliance with state and federal tax regulations. By accurately distinguishing between Pennsylvania-source and non-Pennsylvania-source gains, businesses can achieve appropriate tax reporting and avoid discrepancies.

Key Elements of the PA-65

- Property Transactions: The form details transactions related to the sale, exchange, or disposition of property, highlighting the need for accuracy in reporting gains or losses.

- Distinction Between Sources: Clearly outlines the process for differentiating between gains sourced from within Pennsylvania and those from other states.

- Tax Treatment Adjustments: Provides instructions for making necessary adjustments due to differences in federal and state tax treatments, ensuring compliance with both jurisdictions.

How to Use the PA-65

Understanding how to use the PA-65 is fundamental to any business entity required to file this form in Pennsylvania. The process begins with accurately gathering data from federal income tax forms, which then informs the basis of the PA-65.

Step-by-Step Completion Process

- Data Gathering: Assemble all pertinent records of property transactions, with particular emphasis on those affecting federal tax forms.

- Source Classification: Classify each gain or loss as either Pennsylvania-source or non-Pennsylvania-source.

- Form Completion: Use gathered data to fill out the necessary sections of the PA-65, making careful distinctions where required.

- Adjust for Tax Differences: Implement any adjustments for state versus federal tax treatment variances.

- Submit the Form: Once completed, ensure timely submission via the chosen method.

Steps to Complete the PA-65

Completing the PA-65 requires a thorough understanding of its sections and careful attention to detail. Errors or omissions can result in compliance issues or financial penalties.

- Preparation Phase: Collect all transaction documentation and ensure records of gains and losses are updated.

- Gains and Losses Reporting: Allocate each transaction to the correct category, focusing on the accurate depiction of Pennsylvania-source information.

- Adjustments and Calculations: Calculate necessary adjustments for any differences in recognized gains or losses between federal and state systems.

- Final Review and Submission: Conduct a comprehensive review of the filled form to ensure accuracy before submission.

Legal Use and Importance of the PA-65

The PA-65 is not just a compliance document; it plays a significant role in the legal and fiscal accountability of businesses operating in Pennsylvania.

- Legal Compliance: Adhering to the guidelines ensures that businesses remain compliant with state tax laws and avoid penalties.

- Accurate Financial Reporting: The form is integral to maintaining precise financial records, supporting both internal auditing processes and external financial reporting requirements.

Business Entity Types Using the PA-65

The PA-65 specifically targets particular business entities, making it an essential resource for compliant financial operations.

Entities That Use the PA-65

- S Corporations: Businesses that operate as S corporations need to report property transactions affecting state taxes.

- Partnerships: Partnerships must distinguish state-source gains for equitable tax distribution among partners.

- LLCs: Limited liability companies structured to report gains similar to partnerships or corporations utilize the PA-65 for transparency and accuracy.

State-Specific Rules for the PA-65

Tax regulations can vary significantly from state to state, and Pennsylvania has its own set of rules regarding the filing and utilization of the PA-65.

Unique Pennsylvania Regulations

- Governor's Adjustments: Pennsylvania may require modifications or adherence to specific state tax resolutions.

- Proportional Allocations: Rules governing how different parts of a business's financials get reported based on Pennsylvania-source information are detailed on the form.

Filing Deadlines and Important Dates

Timeliness is essential for tax compliance, making awareness of filing deadlines crucial for businesses utilizing forms like the PA-65.

Deadlines to Keep in Mind

- Annual Filing Date: Typically aligned or shortly after the federal tax filing deadline, modified based on state-specific requirements.

- Extensions: Information on gaining extensions are typically included, although following initial deadlines is encouraged.

Required Documents for PA-65 Submission

Gathering and preparing the necessary documentation is a key starting point when completing the PA-65 form.

Important Documentation

- Federal Tax Forms: Use federal returns to verify gains and losses reported.

- Transaction Records: Details of each property transaction must be clearly documented.

- Adjustments Documentation: Clear record of any adjustments made between federal and state requirements.

In-depth knowledge of the PA-65 and a methodical approach to its completion ensures Pennsylvania businesses fulfill their fiscal obligations efficiently and correctly. This detailed breakdown offers guidance for properly managing and understanding the requirements associated with the PA-65 form.