Type text, add images, blackout confidential details, add comments, highlights and more.

02. Sign it in a few clicks

Draw your signature, type it, upload its image, or use your mobile device as a signature pad.

03. Share your form with others

Send it via email, link, or fax. You can also download it, export it or print it out.

How to use or fill out form 50 246 2014 with our platform

Ease of Setup

DocHub User Ratings on G2

Ease of Use

DocHub User Ratings on G2

Click ‘Get Form’ to open it in the editor.

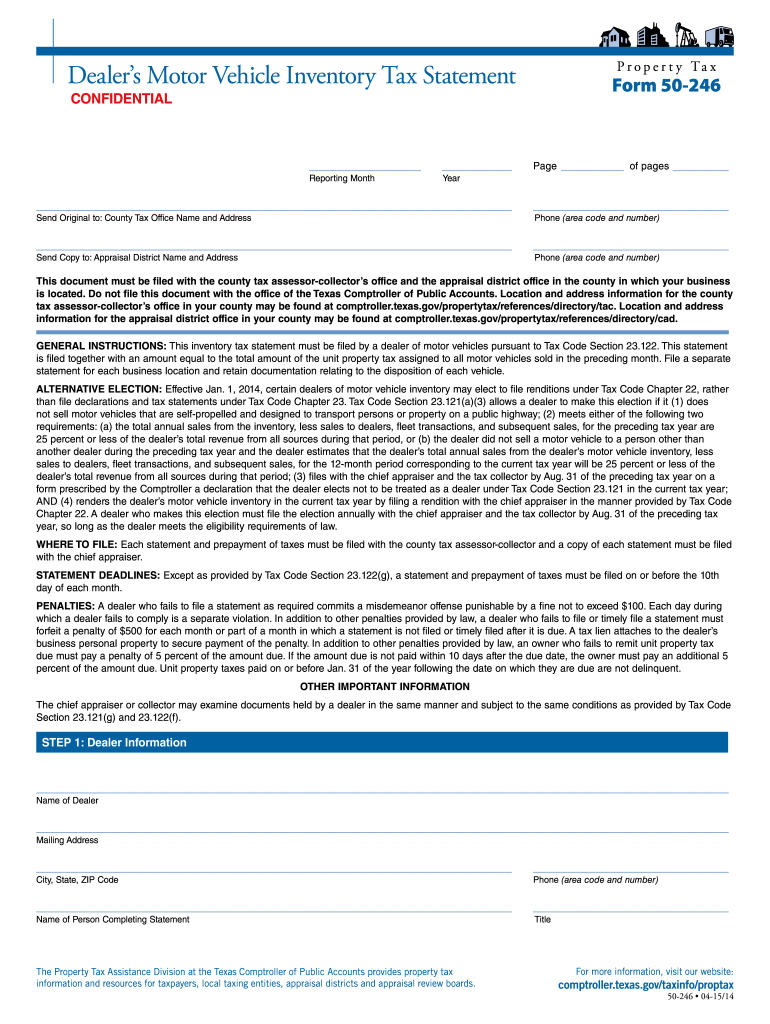

Begin by entering the Dealer Information. Fill in your name, mailing address, city, state, ZIP code, and phone number. Ensure that the name of the person completing the statement is also included.

Proceed to provide your Business Name and Physical Address. If available, include your appraisal district account number and General Distinguishing Number (GDN).

In the Vehicle Inventory Information section, list each motor vehicle sold during the reporting month. Include details such as date of sale, model year, make, vehicle identification number (VIN), purchaser’s name, type of sale, sales price, and total unit property tax.

Next, summarize the Total Units Sold and Total Sales for different categories like Motor Vehicle Inventory and Fleet Transactions. Input both quantity and sales amounts.

Finally, sign and date the form on the last page. Ensure all information is accurate to avoid penalties.

Start using our platform today for free to streamline your form completion process!

GENERAL INSTRUCTIONS: This inventory tax statement must be filed by a dealer of motor vehicles pursuant to Tax Code Section 23.122. This statement.Read more

Feb 3, 2014 The names, logos, emblems, slogans, vehicle model names, and vehicle body designs appearing in this manual including, but not limited.Read more

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.