Definition & Meaning of Form 5471

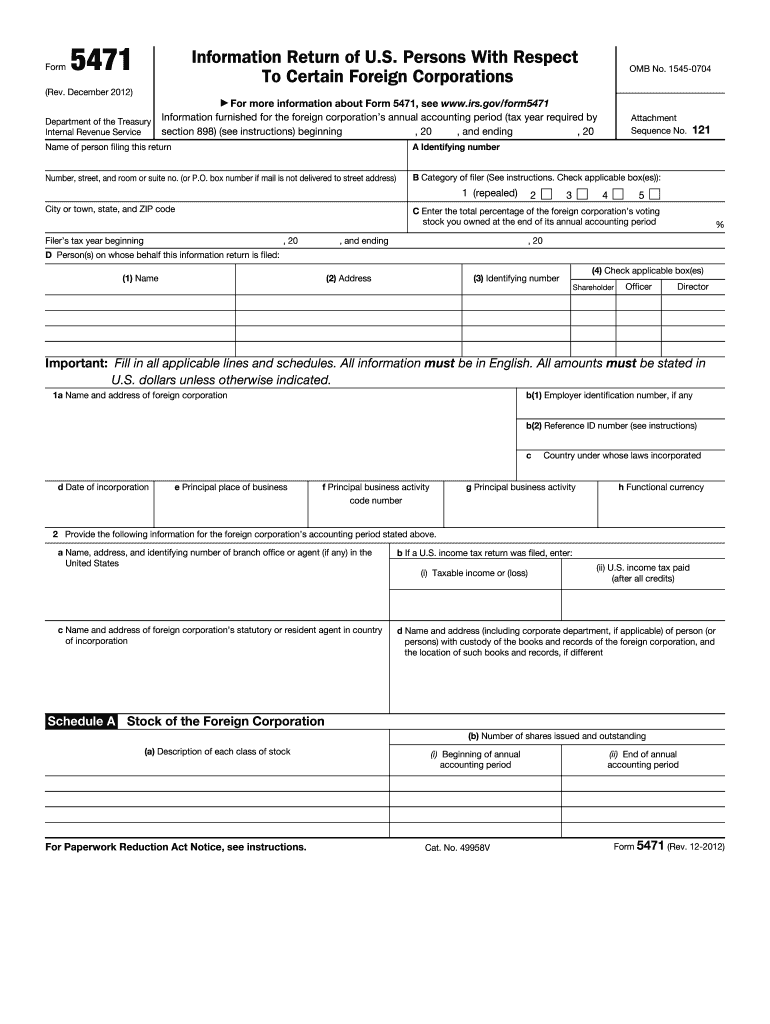

Form 5471 is a mandatory information return required by the U.S. Internal Revenue Service (IRS) for U.S. persons who have certain interests in foreign corporations. This document is essential for reporting financial data, ownership interests, income statements, balance sheets, and shareholder information. It helps the IRS ensure compliance with U.S. tax laws, specifically concerning foreign income reporting. The 2012 version of Form 5471 maintains these requirements and should be understood thoroughly by all applicable U.S. taxpayers.

How to Use the 2012 Form 5471

When using the 2012 Form 5471, it is crucial to complete it accurately, reflecting all necessary financial and ownership details of the applicable foreign corporation. The form is divided into several schedules:

- Schedule B: Reports the acquisition or disposition of foreign stock.

- Schedule C: Details the income statement of the foreign corporation.

- Schedule F: Provides a balance sheet for the foreign corporation.

- Schedule J: Records accumulated earnings and profits.

- Schedule M: Lists transactions between the controlled foreign corporation and its U.S. shareholders.

Each schedule requires careful attention to ensure all sections are thoroughly completed, reflecting the U.S. person's interests and financial relationships with the foreign corporation.

Steps to Complete the 2012 Form 5471

- Gather Necessary Documents: Collect all relevant financial records, shareholder details, and any documentation relating to the foreign corporation's income and expenses.

- Identify Filing Categories: Determine under which category the U.S. person is filing (e.g., Category 1 - 5 filers, based on their level of interest in the foreign corporation).

- Complete Relevant Schedules: Fill out each required schedule accurately; not all schedules may be needed for every filer.

- Report Transactions: Ensure all financial transactions, including those between the U.S. person and the foreign corporation, are reported on the appropriate schedules.

- Review and Verify Information: Thoroughly check the completed form for accuracy and completeness.

- File the Form: Submit the form by the specified deadline, typically with the U.S. person’s income tax return.

Filing Deadlines and Important Dates

The 2012 Form 5471 is due on the same day as the taxpayer's income tax return, including extensions. Typically, this falls on April 15 for individual filers, with a possible extension to October 15 if a timely extension request is filed. It is paramount to adhere to these dates to avoid penalties for late filing.

Penalties for Non-Compliance

Failure to file the 2012 Form 5471 or accurately report required information can result in significant penalties. Common penalties include:

- A base penalty of $10,000 per form per year.

- Additional penalties of up to $50,000 for continued non-compliance after notification.

- Potential reduction of foreign tax credits for the reporting shareholder.

Taxpayers should take proactive steps to ensure compliance, leveraging professional tax advice if needed.

Required Documents

To complete Form 5471, taxpayers should have the following documents:

- Financial statements of the foreign corporation.

- Stock acquisition and disposition records.

- Shareholder registers and agreements.

- Transaction summaries between the foreign corporation and U.S. shareholders.

These records are critical for providing accurate and comprehensive information on the form.

IRS Guidelines for Completing Form 5471

The IRS provides specific instructions for completing Form 5471, emphasizing accuracy and clarity. Key IRS guidelines include:

- Proper classification of filing categories.

- Detailed reporting requirements for each schedule.

- Thorough documentation of financial and ownership interests.

Taxpayers should consult the IRS instructions or a tax professional to ensure all guidelines are followed precisely.

Software Compatibility for Form 5471

Various tax preparation software programs, such as TurboTax and QuickBooks, offer support for completing Form 5471. These programs:

- Provide step-by-step guidance for each part of the form and its schedules.

- Offer error-checking mechanisms to reduce the chance of submission errors.

- Allow for seamless digital submission directly to the IRS.

Using compatible software can streamline the filing process and help ensure compliance with all reporting requirements.