Related links

HTML - Department of Justice

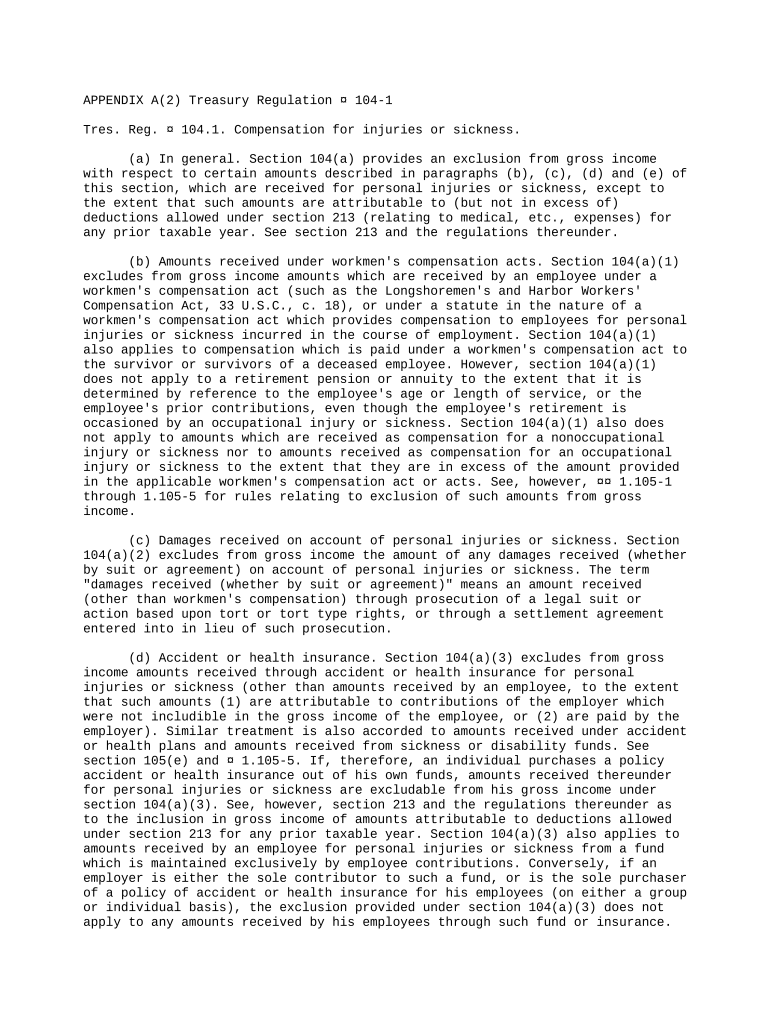

104(a)(2) (stating that damages received ``on account of personal physical injuries or physical sickness are excludable from gross income for purposes of

Learn more

26 CFR 1.104-1 - Compensation for injuries or sickness.

(1) In general. Section 104(a)(2) excludes from gross income the amount of any damages (other than punitive damages) received (whether by suit or agreement

Learn more

Marshall Islands - sawadee.wiki

Until 1999 the islanders received US$180M for continued American use of Kwajalein atoll, US$250M in compensation for nuclear testing, and US$600M in other

Learn more