Definition and Meaning of the First B Notice Backup Withholding Notice

The first B notice, also known as the backup withholding notice, is an essential document issued by the Internal Revenue Service (IRS) to inform payers when there are discrepancies regarding a taxpayer identification number (TIN). Specifically, it is utilized when an incorrect or missing TIN is reported, prompting the IRS to require the payer to withhold a specific percentage of payments made to the payee.

This form serves several important functions:

- Inform the Payee: It notifies the payee of the issue with their provided TIN and educates them about the implications regarding their tax obligations.

- Compliance Requirement: It ensures that the payer complies with federal regulations by enforcing backup withholding procedures.

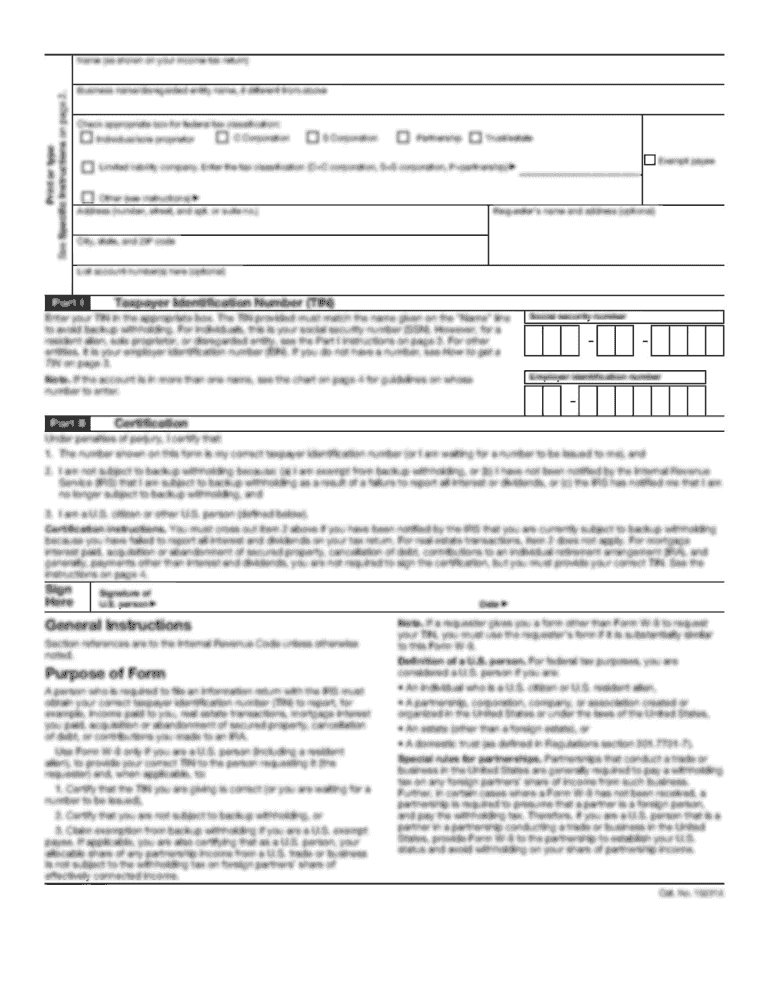

- Request for Action: The notice generally prompts the recipient to verify their TIN, correct any errors, and submit the appropriate documentation, such as Form W-9, to rectify the situation with the IRS.

The first B notice is crucial for maintaining proper tax reporting and withholding practices for both individuals and businesses in the United States.

How to Use the First B Notice Backup Withholding Notice

Utilizing the first B notice effectively involves several critical steps for both the payer and payee.

- Review the Notice: Upon receipt, carefully review the first B notice to understand the specific issues related to the TIN.

- Correct TIN Details: If the recipient identifies an error, they should correct their TIN and complete the applicable IRS forms, usually Form W-9 or W-8.

- Respond Promptly: Timely action is essential. The recipient must respond within a specified timeframe indicated in the notice to avoid redundancy in backup withholding.

- Submit Documentation: The payee should submit the updated TIN to the payer, who must then stop backup withholding once the correct information is received and processed.

- Maintain Records: Both parties should keep copies of all communications and submissions related to the first B notice for compliance and future reference.

By following these steps, payers and payees can mitigate potential tax complications stemming from inaccurate TIN reporting.

IRS Guidelines for the First B Notice Backup Withholding Notice

The IRS outlines specific guidelines regarding the issuance and handling of the first B notice. These guidelines include:

- Issuance Protocol: Payers must issue a first B notice upon receiving a CP2100 or CP2100A notice from the IRS, which indicates discrepancies in reported TINs.

- Timeliness: Payers are required to issue the first B notice to the payees within a reasonable timeframe, typically within thirty days of receiving the IRS notification.

- Backup Withholding Rate: If the TIN remains incorrect, the payer must implement backup withholding at a rate of twenty-four percent on specific payments, including interest, dividends, and certain other reportable payments.

- Follow-Up Requirements: If no updated TIN is provided after issuing the first B notice, the payer may send a second B notice, further emphasizing the need for compliance.

Understanding these guidelines ensures that both payers and payees adhere to IRS regulations, reducing the risk of penalties associated with incorrect withholding practices.

Key Elements of the First B Notice Backup Withholding Notice

The first B notice includes several key elements designed to convey important information to the recipient.

- Payer Information: Details about the payer, including their tax identification information and contact details.

- Recipient Information: The payee's name, address, and the reported TIN that prompted the notice.

- Reason for the Notice: A clear explanation of the specific issue regarding the TIN, typically indicating that it is either missing or does not match IRS records.

- Action Required: Instructions outlining the necessary steps that the payee must take to resolve the issue, including correcting the TIN and re-submitting forms such as W-9 or W-8.

- Consequences of Inaction: A brief overview of the potential ramifications if the required actions are not taken, such as continued backup withholding.

These elements provide clarity to the recipient and help ensure compliance with IRS requirements.

Who Typically Uses the First B Notice Backup Withholding Notice

Various stakeholders use the first B notice in different contexts, primarily involving tax reporting and compliance.

- Payers: Businesses or individuals responsible for making payments that are subject to backup withholding, such as banks issuing interest payments or companies distributing dividends.

- Payees: Recipients of payments who need to comply with IRS requirements by providing correct TINs to avoid undue withholding.

- Tax Professionals: Accountants and tax preparers who assist clients in managing their tax obligations and require accurate documentation and communication regarding IRS notices.

- Government Entities: Agencies and organizations that oversee tax compliance and enforce regulations may reference the first B notice in their dealings with payers and payees.

Recognizing these users aids in understanding the broader context in which the first B notice operates within the U.S. tax system.

Penalties for Non-Compliance Related to the First B Notice Backup Withholding Notice

Failure to comply with the requirements set forth by the first B notice can lead to significant penalties for both payers and payees.

- For Payers: If a payer neglects to issue the first B notice or continues to make payments without a valid TIN, they may face penalties from the IRS. This can include fines for failing to withhold taxes, as well as potential legal action for non-compliance with federal regulations.

- For Payees: Individuals or businesses that do not respond to the notice by providing the correct TIN may be subject to increased withholding rates. They could also face issues during tax filing, affecting potential refunds and incurring additional tax liabilities.

- Legal Implications: Persistent non-compliance can lead to audits by the IRS, which may uncover additional discrepancies requiring resolution and possibly incurring further penalties.

Understanding these penalties emphasizes the importance of prompt action and adherence to IRS requirements when dealing with the first B notice.