Type text, add images, blackout confidential details, add comments, highlights and more.

02. Sign it in a few clicks

Draw your signature, type it, upload its image, or use your mobile device as a signature pad.

03. Share your form with others

Send it via email, link, or fax. You can also download it, export it or print it out.

How to use or fill out mortgage 05m with our platform

Ease of Setup

DocHub User Ratings on G2

Ease of Use

DocHub User Ratings on G2

Click ‘Get Form’ to open the mortgage 05m in the editor.

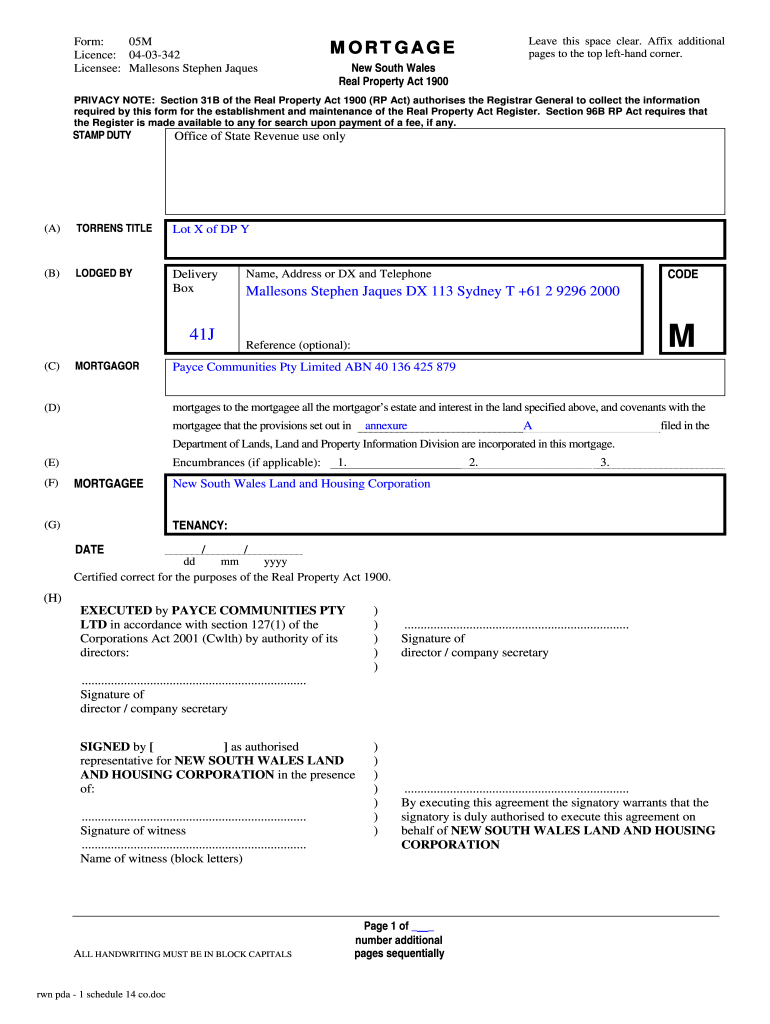

Begin by filling in the 'MORTGAGOR' section. Enter the name, address, and contact details of the mortgagor, ensuring all handwriting is in block capitals as specified.

In the 'MORTGAGEE' section, provide the necessary details for the mortgagee. This may include multiple entries if applicable.

Complete the 'DATE' field by entering the date of execution in dd/mm/yyyy format.

Ensure that signatures are provided by both directors or company secretaries in accordance with section 127(1) of the Corporations Act 2001 (Cwlth).

Finally, add a witness signature and their name in block letters to validate the document.

Start using our platform today to fill out your mortgage 05m form online for free!

by A Morse 2013 Cited by 12 Mortgage restructurings were very stable and low before at less than 2% of delinquent loans. After the foreclosure moratorium more than 15% ofRead more

Dec 9, 2023 ALTA Endorsement Form 6-06 Variable Rate Mortgage (05/01/07). ALTA Endorsement Form 6.2-06 Variable Rate Mortgage - Negative Amortization. (05/Read more

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.