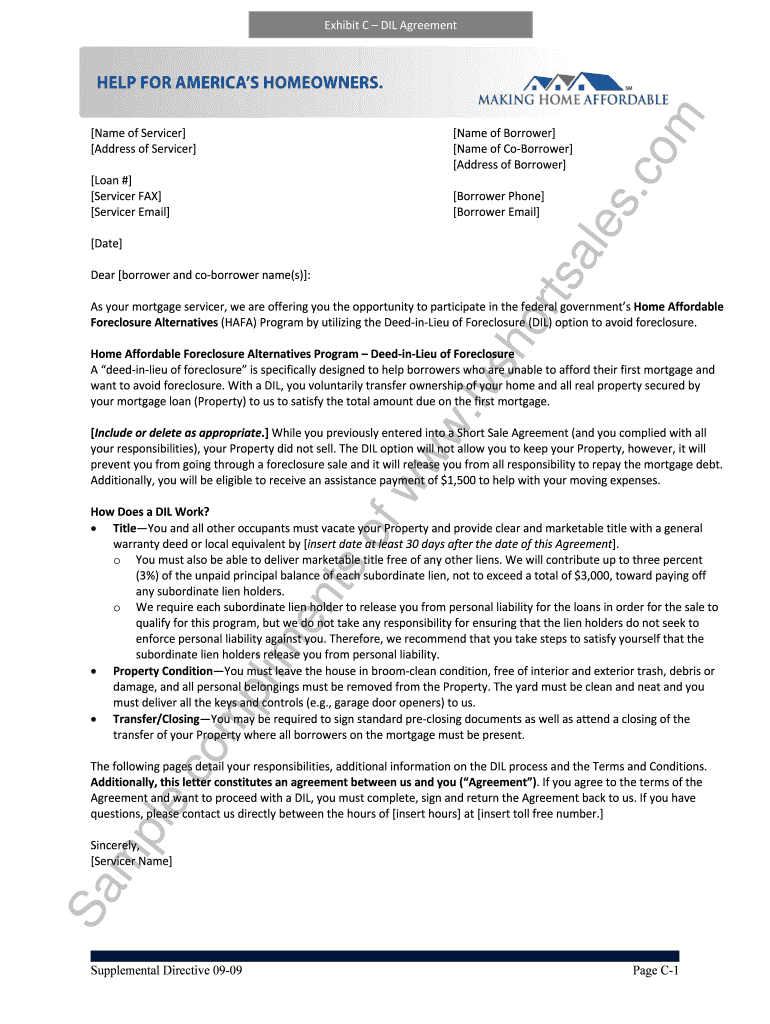

Definition and Meaning

The Deed-in-Lieu of Foreclosure Agreement is a legal document used as a resolution for homeowners who are unable to make mortgage payments. This agreement allows the homeowner to transfer the title of their property back to the lender as an alternative to foreclosure. In essence, the homeowner voluntarily surrenders the property to avoid the negative consequences associated with foreclosure, such as a significant impact on their credit score. By relinquishing the property, the homeowner may potentially receive relief from their mortgage debt, contingent upon the specific terms of the agreement.

Benefits within the Agreement

- Avoidance of Foreclosure: Opting for a deed-in-lieu can mitigate the long-term damage to one's credit that a foreclosure might cause.

- Potential Debt Forgiveness: Some lenders may forgive the remaining mortgage balance, depending on the agreement's clauses.

Key Elements of the Deed-in-Lieu of Foreclosure Agreement

The agreement encompasses several critical components that both parties must carefully consider:

- Transfer of Property Title: The homeowner transfers all interest and rights of the property to the lender.

- Release from Mortgage Obligations: Often, the lender will release the borrower from further financial obligations regarding the mortgage.

- Conditions for Acceptance: Lenders may have conditions, such as maintaining the property or resolving any secondary liens before acceptance.

Examples of Common Clauses

- Condition of Property Maintenance: The agreement may specify the condition in which the property must be kept before it can be returned to the lender.

- Jurisdictional Variations: Provisions in the agreement can vary based on state regulations, impacting process and obligations.

Steps to Complete the Deed-in-Lieu of Foreclosure Agreement

The process involves several structured steps to ensure compliance and a mutual understanding between the involved parties.

-

Preliminary Consultation: Homeowners should consult with a financial advisor or legal expert to evaluate the suitability of the arrangement.

-

Communication with the Lender: Initiate discussions with the lender to express the intent and understand any prerequisites for the agreement.

-

Submission of Required Documents: Provide financial documents, hardship letters, and any additional requested information to the lender.

-

Review of Agreement Terms: Carefully examine the terms presented by the lender, including contingencies and any debt relief details.

-

Sign and Record the Agreement: Once the terms are acceptable, sign the agreement and ensure it is legally recorded to finalize the arrangement.

Who Typically Uses the Deed-in-Lieu of Foreclosure Agreement

This agreement is commonly utilized by homeowners facing financial hardships who are unable to meet their mortgage obligations, especially those who:

- Seek to Mitigate Impact on Credit: Individuals who prioritize minimizing credit damage in lieu of foreclosure.

- Face Significant Property Depreciation: Owners of properties significantly declining in value, compared to the owed mortgage balance.

- Exhausted Other Options: Those who have considered and been unable to qualify for other foreclosure alternatives like mortgage modifications.

Why You Should Consider a Deed-in-Lieu of Foreclosure Agreement

Engaging in a deed-in-lieu of foreclosure agreement can be advantageous under certain circumstances:

- Reduced Stress: Simplifies the process of resolving mortgage default without going through foreclosure.

- Potential Relocation Assistance: Some lenders offer relocation assistance or financial incentives to homeowners who agree to a deed-in-lieu.

- Quicker Resolution: Often resolves more quickly than the lengthy foreclosure process, enabling the homeowner to focus on recovering their financial stability.

State-Specific Rules for the Deed-in-Lieu of Foreclosure Agreement

The regulations surrounding deed-in-lieu agreements can vary significantly depending on the state. Homeowners must ensure compliance with specific state requirements, which may include:

- Redemption Periods: Some states may have a statutory redemption period, offering homeowners a timeline to settle debts even after transferring the deed.

- Lien Resolution: Guidelines on handling additional liens or mortgages vary, possibly affecting eligibility or terms.

Legal Use of the Deed-in-Lieu of Foreclosure Agreement

Understanding the legal context is crucial for anyone considering this agreement. The deed-in-lieu of foreclosure's legality involves:

- Federal and State Regulations: Adherence to the Real Estate Settlement Procedures Act (RESPA) and state-specific real estate laws.

- Enforceability: The agreement must be drafted to meet local jurisdiction requirements to remain enforceable and provide intended relief.

Important Terms Related to Deed-in-Lieu of Foreclosure Agreement

Understanding key terminologies ensures clarity in negotiations and expectations:

- Voluntary Conveyance: The process by which the property is relinquished back to the lender willingly by the homeowner.

- Deficiency Judgment: A judgment against the borrower when the sale of a foreclosed property does not cover the total mortgage balance—though typically waived in deed-in-lieu agreements.

In sum, a deed-in-lieu of foreclosure agreement serves as an alternative mechanism to foreclosure, promoting both credit protection and potential debt relief. With due diligence and understanding of state laws, homeowners can effectively utilize this agreement to manage financial distress.