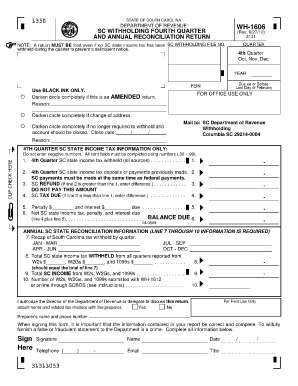

Definition & Meaning

The Accessible Sales and Use Tax Return is a crucial form for businesses operating within the United States, designed to facilitate the reporting and remittance of sales and use taxes to the appropriate fiscal authorities. This form captures detailed information about the sales transactions subject to taxation, allowing businesses to ensure compliance with tax obligations. Each state may have nuances in how sales and use taxes are calculated, making it essential for businesses to understand the specific requirements for their jurisdiction.

Key Features

- Purpose: The form serves to report sales and use taxes collected from customers during transactions.

- Scope: Includes all taxable sales, use of goods, and services within a specific reporting period.

- Jurisdictional Variance: State-specific adjustments can affect the filing requirements significantly.

Understanding Use Tax

Use tax applies when sales tax hasn't been collected—typically in cases of out-of-state purchases for in-state use. Businesses must accurately record and report these instances to ensure lawful compliance.

How to Use the Accessible Sales and Use Tax Return

Using the Accessible Sales and Use Tax Return starts with understanding its components and filling them out accurately. This process ensures compliance with both state and federal tax laws, reducing the risk of errors and penalties.

Steps to Utilize the Form

- Data Collection: Gather all transaction records, including sales invoices and purchase receipts.

- Accurate Calculations: Ensure correct calculations of taxable amounts and applicable tax rates.

- Form Completion: Carefully fill out sections detailing the nature of sales, exempt transactions, and total taxable sales.

Calculation Example

- Tax Rate Identification: Check state-specific tax rates for both sales and use tax.

- Taxable Sales Calculation: Determine the total amount of taxable sales in the reporting period.

- Use Tax: Calculate use tax on out-of-state purchases applicable for use within the state.

Steps to Complete the Accessible Sales and Use Tax Return

Completing the tax return form accurately involves a series of methodical steps to ensure all necessary information is correctly entered. This process involves precision in accounting for sales and adherence to state-specific guidelines.

Detailed Completion Steps

- Verification of Information: Double-check business details for accuracy—name, address, tax identification number.

- Sales Entry: Document all sales transactions, including dates and amounts.

- Exemption Handling: Specify any exempt sales, providing documentation where required.

- Final Calculation: Calculate total taxes owed, ensuring all deductions and exemptions have been applied.

Example Scenario

A business located in Colorado sells both taxable and exempt goods. By differentiating these sales appropriately on their return, they ensure only taxable sales are reported and subject to tax.

Important Terms Related to Accessible Sales and Use Tax Return

Understanding the terminology associated with the Accessible Sales and Use Tax Return can provide clarity and enhance accuracy when completing the form.

Key Terms

- Taxable Sales: Sales transactions subject to taxation as determined by state laws.

- Exempt Sales: Transactions that are excluded from sales tax, often involving specific products or buyers.

- Reporting Period: The timeframe for which transactions are recorded in the tax return, typically monthly or quarterly.

Practical Examples

- Taxable Sales: Retail sales to end consumers.

- Exempt Sales: Wholesale transactions or sales to non-profit organizations.

State-Specific Rules for the Accessible Sales and Use Tax Return

Each U.S. state has distinct regulations governing the sales and use tax process, affecting how businesses prepare and submit their tax returns. These rules can impact everything from tax rates to form submission methods.

Variations Across States

- Colorado: Some local jurisdictions may impose additional taxes beyond the state sales tax.

- California: The state requires electronic filing for certain businesses.

- Texas: Exemptions might apply for agricultural and manufacturing businesses.

Compliance Tips

- Regular Updates: Stay informed about legislative changes in state tax codes.

- Professional Consultation: Engage with tax professionals for complex multi-state operations.

Penalties for Non-Compliance

Filing the sales and use tax return incorrectly or failing to file on time can lead to several penalties. Understanding these repercussions can motivate businesses to maintain compliance and accuracy.

Types of Penalties

- Late Filing: Fines for not submitting the tax return within the designated deadline.

- Underpayment: Additional charges for wrongly reporting sales figures or tax amounts.

- Interest Charges: Accumulating interest on unpaid taxes over time.

Avoidance Strategies

- Timely Filing: Establish a schedule to prepare and file returns well ahead of deadlines.

- Professional Audits: Regularly audit financial records to ensure all sales and use tax is reported correctly.

Software Compatibility (TurboTax, QuickBooks, etc.)

Maximizing efficiency in handling sales and use tax returns can be achieved by leveraging software that integrates well with existing business systems. Compatibility with accounting software offers numerous advantages.

Compatible Software

- QuickBooks: Streamlines data entry with pre-populated forms for accurate tax calculations.

- TurboTax: Offers features to import transactional data directly from accounting records and compute taxes due.

Benefits of Integration

- Error Reduction: Automation reduces manual input errors and ensures accurate data transfer.

- Efficiency Boost: Faster completion of tax returns with automatic calculations and reporting.

Business Entity Types and the Accessible Sales and Use Tax Return

Different types of business entities have unique concerns and requirements when filing the Accessible Sales and Use Tax Return. Understanding these differences is crucial for accurate filing.

Applicable Entity Types

- LLC (Limited Liability Company): Offers flexibility in how sales are reported and taxed.

- Corporations: May face specific regional tax regulations affecting their filing process.

- Partnerships: Require coordination among partners for filing on behalf of the business.

Filing Considerations

- LLC: Each member's share of sales may need reporting for tax liability distribution.

- Partnerships: Accurate allocation of income and credits is essential for tax purposes.