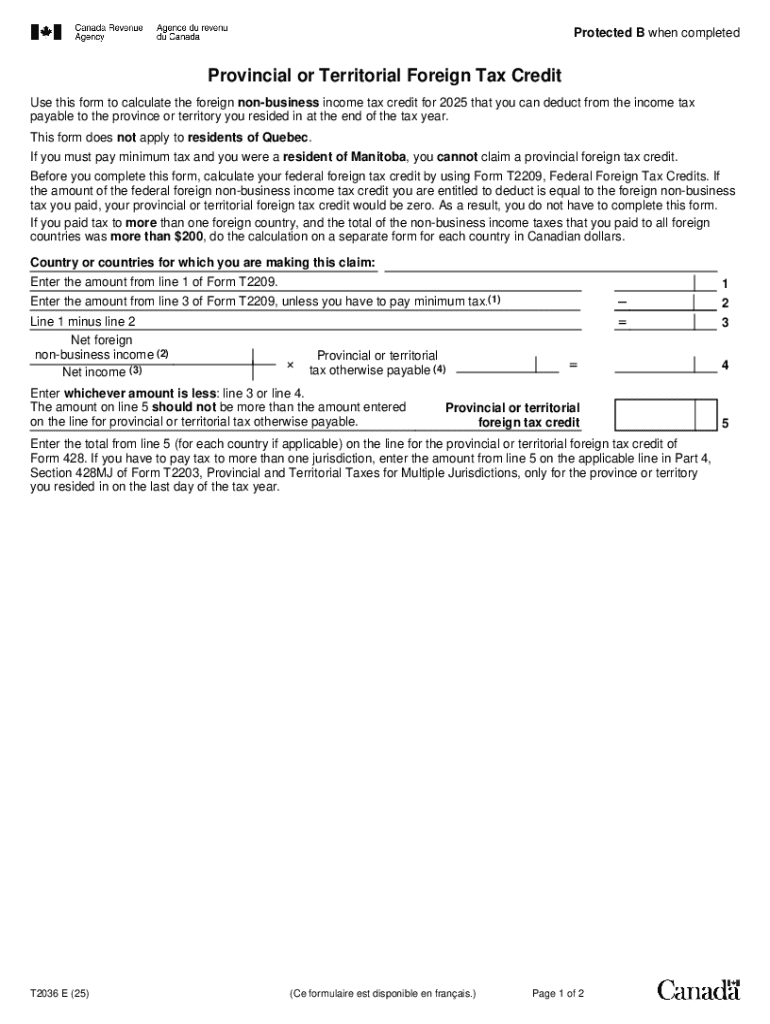

Definition and Meaning

The Provincial or Territorial Foreign Tax Credit Form is utilized by taxpayers to calculate and claim foreign nonbusiness income taxes paid to a foreign country, which can be deducted from the income tax payable in their respective province or territory. This form allows individuals to avoid double taxation on the same income, aligning with the principles of international tax treaties that the United States adheres to.

Key Elements of the Form

- Calculation of Foreign Tax Credit: The form includes specific sections dedicated to computing the foreign nonbusiness income tax credit, which helps minimize your tax liability by accounting for taxes paid abroad.

- Income Sources: You are required to list all foreign income sources from which taxes were paid, ensuring accurate documentation of earnings and taxes.

- Deductions and Credits: Details are provided for potential deductions and credits available beyond the basic foreign tax credit.

Steps to Complete the Provincial or Territorial Foreign Tax Credit Form

-

Gather Required Documents: Collect documents such as foreign income reports, tax receipts, and any relevant tax assessment documents from foreign authorities.

-

Complete Personal Information: Input your personal details, such as your name, address, and taxpayer identification number, in the designated sections of the form.

-

Calculate Eligible Foreign Taxes: Use the provided spaces to calculate the total amount of foreign nonbusiness income tax that qualifies for the credit.

-

Input Foreign Income Details: Enter specifics about your foreign income sources, such as types of income (e.g., dividends, employment), amounts, and countries of origin.

-

Finalize and Review the Form: Ensure that every section is correctly filled out, double-checking for any mistakes or omissions.

-

Submit the Form: Depending on your preference and availability, submit the form through the designated channels, which can include online submissions, mail, or in-person delivery.

Required Documentation

- Foreign Income Statements

- Foreign Tax Receipts

- Proof of Payment to Foreign Authorities

Eligibility Criteria

Individuals

- U.S. citizens or residents subject to income tax liabilities in the U.S.

- Must have paid nonbusiness income tax to a foreign country that aligns with the tax treaties.

Income Types

- Nonbusiness income, such as dividends, interest, or capital gains, must originate from foreign sources and be documented adequately.

Taxpayer Scenarios

Self-Employed Individuals

Self-employed individuals operating internationally may claim the foreign tax credit to reduce their tax dues on global earnings.

Retired Individuals

If retired individuals receive foreign pension income, they can use this form to minimize the tax impact of their international retirement funds.

Filing Deadlines and Important Dates

- Typically aligned with the general federal tax filing deadlines, which is April 15 for most taxpayers. It is crucial to check for any extensions granted in specific tax years due to unusual circumstances, such as natural disasters or pandemic-related adjustments.

Penalties for Non-Compliance

Failing to file this form correctly, or submitting it late without requesting an extension, may result in penalties, including interest on unpaid taxes and potential forfeiture of tax credits.

How to Obtain the Form

- The Provincial or Territorial Foreign Tax Credit Form can be obtained through the IRS website, ideally accessed online for the most recent and updated version.

- Forms are also available at local IRS offices and can be mailed upon request if access to online resources is limited.

How to Use the Form

Online Platforms

- Several tax preparation software options, like TurboTax or QuickBooks, facilitate the completion of this form by guiding users through step-by-step processes, ensuring all necessary fields are filled correctly.

Traditional Methods

- Hard copies can be filled manually and submitted via traditional mail or delivered directly to a regional tax office.

Variations and State-Specific Rules

Variations

- While the core principles of the foreign tax credit remain uniform across the U.S., specific provinces or territories may have variations in their form, reflecting localized tax laws or cooperative agreements with foreign governments.

State-Specific Regulations

- Taxpayers should check with state tax agencies for any additional rules or forms to be completed in conjunction with the federal form, as some states have their adjustments or credits that apply to foreign income taxes.

Software Compatibility

Integration with Major Tax Software

- Compatibility with reputable tax software ensures ease of form submission and accuracy, as these platforms typically update their modules to reflect the latest tax law changes automatically.

Manual and Automated Features

- Users can choose between automated calculations provided by software or manually input data when using traditional methods, ensuring flexibility in filing preferences.

By addressing these elements comprehensively, individuals and businesses can ensure effective utilization of the Provincial or Territorial Foreign Tax Credit Form, aligning with tax regulations while optimizing their tax obligations.