Definition & Purpose of Form 8288 (Rev January 2026)

Form 8288, known as the U.S. Withholding Tax Return for Certain Dispositions by Foreign Persons, is a key document issued by the Internal Revenue Service (IRS). It is primarily used to report and remit withholding tax on the disposition of U.S. real property interests (USRPI) by foreign persons. This form is essential for ensuring compliance with tax laws under the Foreign Investment in Real Property Tax Act (FIRPTA). FIRPTA mandates that buyers withhold a portion of the sale proceeds when purchasing property from a foreign seller to ensure that taxes are paid on any gain from the sale.

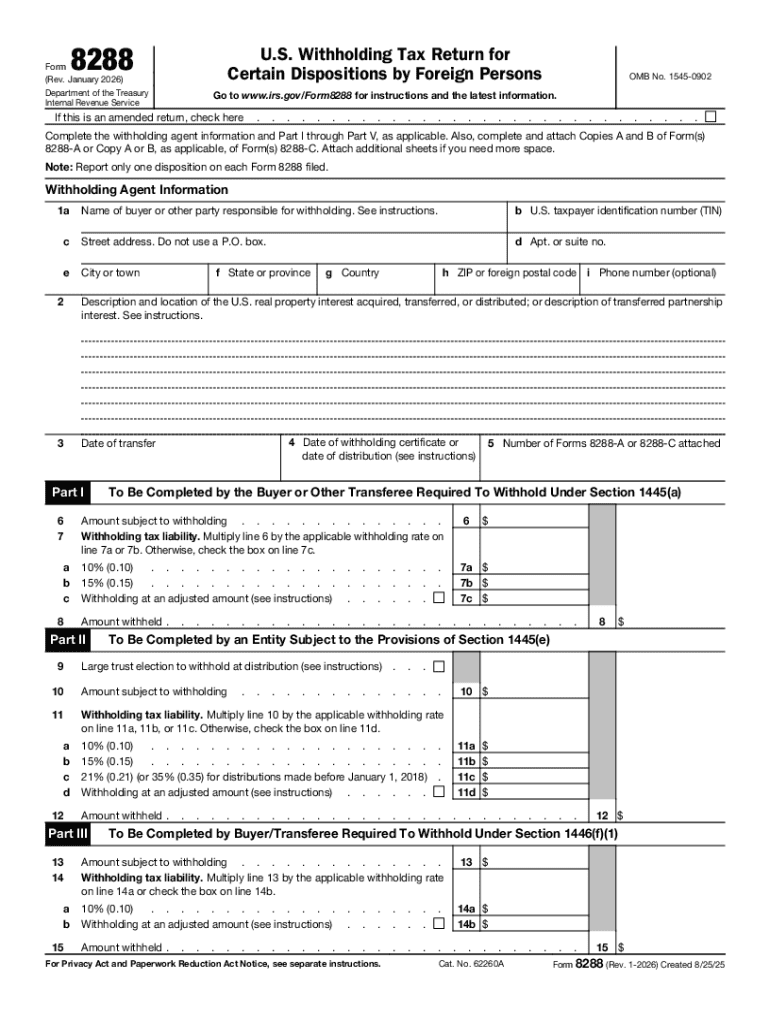

Key Elements of Form 8288

- Payer Information: Details about the withholding agent, often the buyer or intermediary in a transaction involving a foreign seller.

- Payment Information: Precise calculations of the amount withheld, which depends on the transaction details and potential exemptions.

- Property Details: Description and location of the U.S. real property interest sold, aiding in accurate record-keeping and compliance.

Why Use Form 8288?

Compliance with IRS regulations through Form 8288 ensures that taxes due from the sale of U.S. real estate by foreign persons are collected. This prevents legal penalties and establishes transparency in international real estate transactions. U.S. buyers in such transactions must file Form 8288 to protect themselves from potential tax liabilities.

Steps to Complete Form 8288 (Rev January 2026)

Filling out Form 8288 involves multiple steps due to its detailed nature. The following outlines a standard process for completing this form accurately:

- Gather Necessary Information: Collect all relevant details about the property transaction, including personal and contact information for both the seller and buyer, as well as the sales price and date of transaction.

- Determine Withholding Amount: Calculate the appropriate percentage of the sales proceeds that must be withheld according to IRS guidelines. Typically, 15% of the gross proceeds are withheld, but this may vary based on exemptions and specific transactional circumstances.

- Complete Form Sections: Fill out each section of the form with accurate and complete information to avoid processing delays or penalties.

- Review for Accuracy: Double-check all inputs for mistakes. Errors can lead to processing delays or non-compliance penalties from the IRS.

- Attach Required Documentation: Include any necessary supporting documents, such as a copy of the contract of sale or any forms requesting reduced withholding.

- Submit the Form: Submit the completed form and payment to the IRS by the due date, which is typically within 20 days after the date of transfer.

Required Documents

- Contract of Sale: Proof of the real estate transaction and its details.

- Identification Documents: Both foreign seller and U.S. buyer may need to provide identification numbers such as SSN or ITIN.

- Exemption Certificates: If applicable, include documents evidencing any claimed withholding exemptions.

Who Typically Uses Form 8288?

Form 8288 is utilized by:

- Foreign Sellers and U.S. Buyers of Realty: Foreign individuals or entities selling U.S. property and the U.S.-based buyers responsible for withholding and submitting the tax.

- Withholding Agents: Typically, this is the buyer in the transaction, but it can also be a properly designated responsible party.

- Real Estate Professionals: Agents and attorneys who aid in handling real estate transactions with foreign participants.

IRS Guidelines for Form 8288

The IRS provides specific guidelines for completing and submitting Form 8288, which include the proper calculation of withholding tax amounts and the designation of the responsible withholding agent. Adhering to these guidelines is essential for avoiding legal complications.

Filing Deadlines and Important Dates

- General Deadline: Submit Form 8288 within 20 days after the date of transfer of the property.

- Extensions: While there are no standard extensions for payment, requesting reduced withholding may affect timing.

Penalties for Non-Compliance

Failure to comply with filed withholding or incorrectly filing Form 8288 may result in substantial penalties, including fines and interest on withheld payments. Both buyers and withholding agents are held liable for failing to meet IRS requirements, which underscores the importance of timely and accurate filing.

Form Submission Methods

- Mail: Traditional submission of Form 8288 to the IRS requires postal services and adherence to correct mailing addresses as specified by the IRS.

- No Digital Option: Currently, Form 8288 does not have an electronic submission option on the IRS website, making mail the primary method.

Who Issues and Benefits from Form 8288?

The IRS, part of the Department of the Treasury, issues Form 8288. Primarily, U.S. buyers in transactions involving foreign sellers benefit from this form as it ensures they comply with U.S. tax obligations, reducing the risk of financial liabilities.

Business Entity Considerations

- LLC and Corporations: Entities must be aware of their role in transactions involving foreign sellers to accurately process and file Form 8288.

- Partnerships: Partnerships involved in these transactions often need legal or accounting advice to ensure proper compliance with FIRPTA regulations.

By understanding and following these elements of Form 8288, buyers and real estate professionals can navigate property transactions involving foreign persons with a higher degree of accuracy and legal compliance.