Definition & Meaning

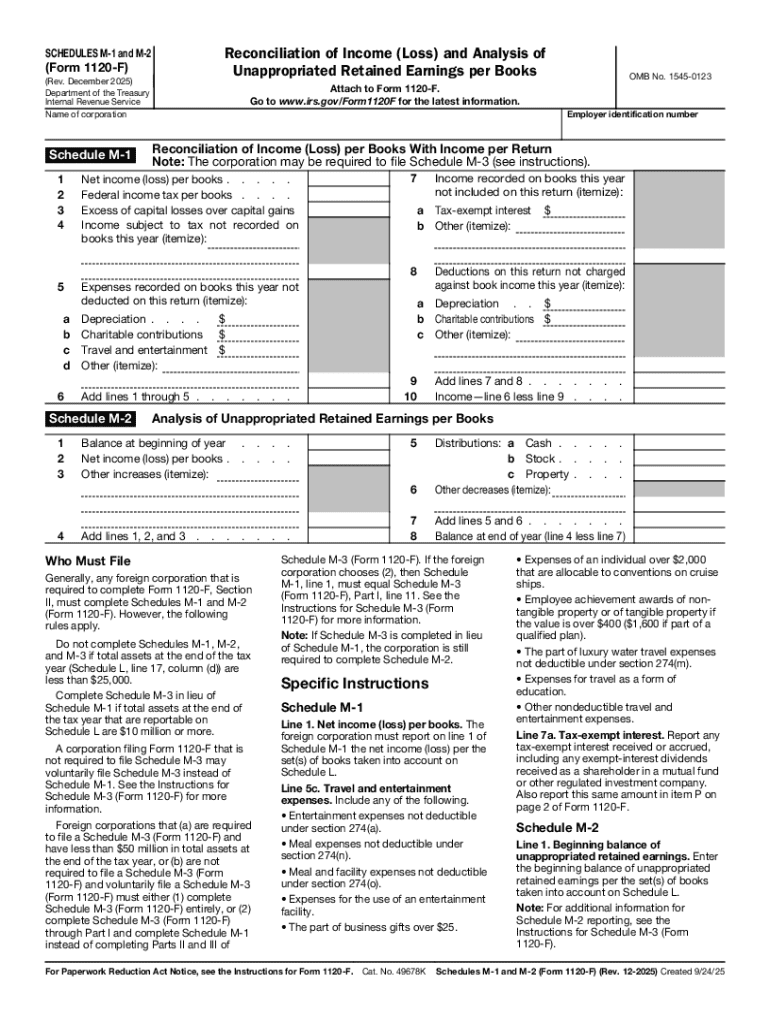

The Schedules M-1 and M-2 (Form 1120-F) (Rev December 2025) are crucial components of the U.S. tax filing system for foreign corporations doing business in the United States. Schedule M-1 reconciles the book income with taxable income before the net operating loss (NOL) and special deductions. This reconciliation ensures that any differences between a corporation's financial accounting and tax reporting are transparent and explained. Schedule M-2, on the other hand, analyzes changes in the company's unappropriated retained earnings, reflecting dividends paid and adjustments made during the year. These schedules are essential for thorough and accurate tax reporting.

- Schedule M-1: Focuses on reconciling income and deductions according to tax law versus book records.

- Schedule M-2: Addresses changes in retained earnings from the beginning to the end of the tax year.

Understanding these definitions helps filers ensure compliance and accuracy in their U.S. tax responsibilities.

Who Typically Uses the Schedules M-1 and M-2 (Form 1120-F) (Rev December 2025)

Foreign corporations operating in the United States generally must complete these schedules as part of their tax filing requirements. These entities may engage in trade or business within the U.S. or derive income connected to such operations. By using Schedules M-1 and M-2, these corporations help the IRS gain a comprehensive understanding of their financial activities in the country.

- Large Foreign Corporations: Those with significant U.S.-based operations or subsidiaries.

- Tax Preparers and Accountants: Professionals responsible for filing corporate taxes on behalf of international clients.

The relevance of Schedules M-1 and M-2 is to provide clarity on reported incomes and retained earnings that support accurate tax assessments.

Important Terms Related to Schedules M-1 and M-2 (Form 1120-F) (Rev December 2025)

Familiarizing yourself with key terms can streamline the completion of this form. Key terms include:

- Book Income: Revenue recorded in the financial statements of the corporation, based on accounting principles rather than tax rules.

- Taxable Income: Income calculated in compliance with U.S. tax laws, which considers allowable deductions and credits.

- Net Operating Loss (NOL): A scenario where tax-deductible expenses exceed taxable revenues, which can impact future taxable income.

- Unappropriated Retained Earnings: Profits not distributed as dividends and retained for future corporate growth or debt repayment.

These terms underpin the calculations and reconciliations needed when filing the form, ensuring accurate reporting and verification.

Steps to Complete the Schedules M-1 and M-2 (Form 1120-F) (Rev December 2025)

Completing these schedules requires careful attention to detail and a structured approach:

- Gather Financial Statements: Start with your annual financial reports and statements to obtain book income figures.

- Reconcile Book to Taxable Income: On Schedule M-1, identify and adjust for differences between your book income and taxable income.

- Include any non-deductible expenses or additionally taxable revenues.

- Analyze Retained Earnings: On Schedule M-2, list changes in retained earnings due to net income, dividends, and other adjustments.

- Cross-Verify Entries: Ensure all figures match corresponding entries in Form 1120-F.

- Complete Supporting Sections: Include any additional schedules or statements that may be relevant to your specific tax situation.

By following these steps, foreign corporations can efficiently prepare their Schedules M-1 and M-2, ensuring compliance with IRS requirements.

IRS Guidelines

The IRS provides specific instructions on how to fill out Schedules M-1 and M-2 accurately. These guidelines emphasize the importance of maintaining comprehensive documentation and clarity in reporting. Filers must:

- Adhere to Prescribed Formats: Use IRS-provided formats to ensure uniformity.

- Attach Required Documentation: Include necessary supporting documents and schedules to substantiate figures reported.

- Be Public and Accurate about Financial Disclosures: Transparency in financial operations and tax liabilities is essential for compliance.

Familiarity with IRS guidelines can prevent common errors and ensure filing correctness.

Filing Deadlines / Important Dates

Timing is critical in the tax filing process. For foreign corporations, typical deadlines align with the larger tax calendar:

- April 15: Standard filing deadline for calendar year tax returns, unless an extension has been filed.

- October 15: Extended deadline for those who applied for a six-month extension.

Meeting these deadlines is crucial to avoid penalties or interest on overdue taxes. Extensions must be requested proactively, typically by filing IRS Form 7004.

Penalties for Non-Compliance

Failure to comply with the requirements of Schedules M-1 and M-2 can result in various penalties:

- Filing Penalties: Late submissions may incur financial penalties, increasing with the severity of the delay.

- Accuracy-Related Penalties: Significant underreporting or misstatement of income can lead to additional fines.

- Interest Charges: Unpaid taxes due to incorrect reporting might accumulate interest until the full amount is paid.

Understanding these potential penalties underscores the importance of accurate and timely form completion.

Software Compatibility (TurboTax, QuickBooks, etc.)

Many corporations utilize tax software to facilitate the completion of these complex schedules. Compatibility information includes:

- TurboTax: Assists with importing data and automatically calculating entries for seamless filing.

- QuickBooks: Integrates financial data, helping to prepare reconciliations required for Schedules M-1 and M-2.

Utilizing compatible software simplifies data organization and ensures calculations adhere to IRS requirements.