Definition and Purpose of 706-NA

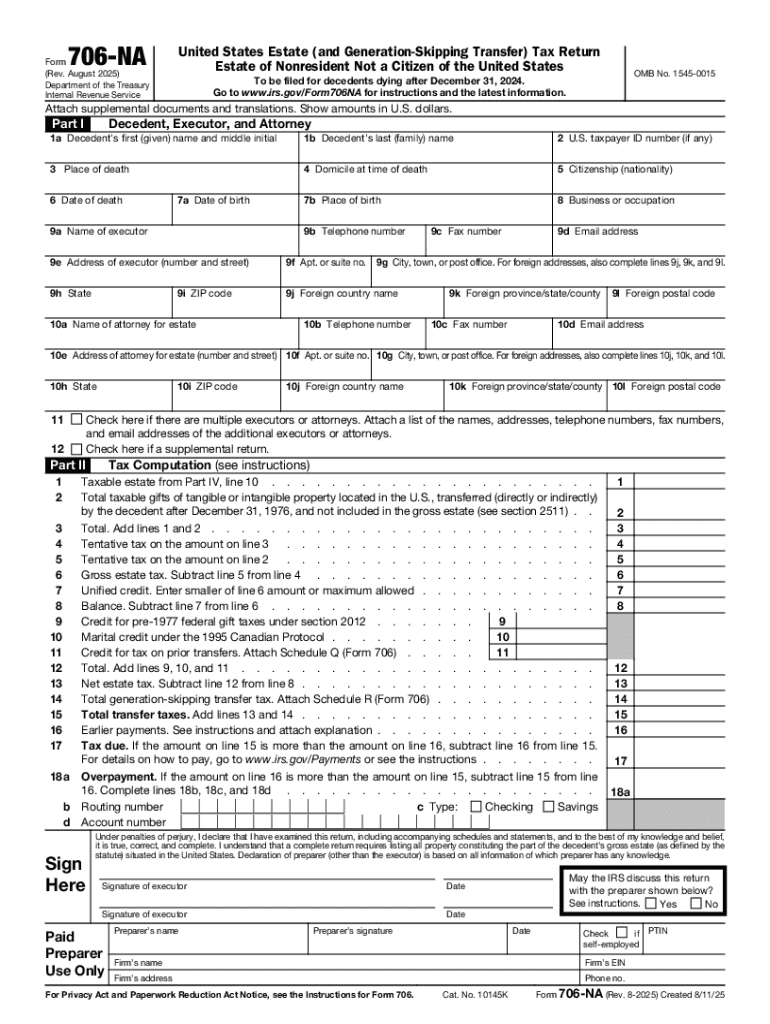

The 706-NA form, Report of Executor, is used in the United States to report estate tax for nonresident decedents who are not U.S. citizens. This form is critical for determining the estate tax liability on the U.S.-situated assets of a deceased individual. Estate taxes are levied on the transfer of the "taxable estate" of a deceased person, which consists of the gross estate less allowable deductions. For nonresidents, only assets located within the U.S. are subject to this tax requirement.

The form ensures that the estate fulfills its tax obligations within the U.S. jurisdiction and is specifically designed to accommodate the differences in how estate taxes apply to nonresident noncitizens. It's important for accurately assessing tax responsibilities, providing an overview of the decedent’s holdings, and ensuring compliance with federal law. Executors handling such estates must navigate the nuances of this form to avoid legal complications.

Steps to Complete the 706-NA

-

Identify Assets: Begin by compiling a detailed inventory of all assets located within the U.S. This includes real estate, financial accounts, and tangible personal property. The valuation of these assets is crucial, often necessitating expert appraisal.

-

Determine Deductions: Calculate allowable deductions, which may include funeral expenses, debts, and taxes paid to foreign governments. These deductions are vital for lowering the estate's taxable value.

-

Complete Part One: Enter information about the decedent, such as name, date of death, and domicile. Accurate details ensure that the application is processed without issues.

-

Fill in Part Two: Asset Descriptions: Provide detailed information about each asset, including location and market value. Use proper descriptions to avoid future disputes.

-

Calculate Taxable Estate: Add the asset values and subtract deductions to determine the taxable estate. This figure represents the estate's financial obligation to the IRS.

-

Review and Amend: Carefully review the form for errors or omissions, as inaccuracies can lead to audits or penalties.

-

Submit: File the form with the Internal Revenue Service by the due date. Retain a copy for records.

Important Terms Related to 706-NA

-

Decedent: The individual who has passed away.

-

Executor: The person responsible for managing the decedent’s estate.

-

Gross Estate: The total value of the decedent’s assets before deductions.

-

Taxable Estate: The value of the estate subject to tax after deductions are applied.

-

U.S. Situs Property: Assets located within the United States, including real estate, tangible items, and interests in U.S. corporations.

Understanding these terms is essential for anyone required to complete the form, as legal definitions may differ from common perceptions.

Legal Use of the 706-NA

The legal framework underpinning the use of the 706-NA is established by U.S. estate tax law. This form is specific to nonresidents who own U.S. property, aiming to ensure that foreign decedents pay taxes similar to those imposed on U.S. citizens and residents. The legal use extends to accurately disclosing the decedent’s U.S.-located holdings and filing within nine months of the date of death, unless an extension has been granted.

Noncompliance can lead to legal penalties, heightened scrutiny, and interest on unpaid taxes. The form must be filed correctly to protect the estate’s representatives from personal liability.

Key Elements of the 706-NA

-

Decedent Information: Background details.

-

Executor Details: Identifying who is submitting the form.

-

Valuation of U.S. Assets: Financial appraisals and descriptions.

-

Deductions and Credits: Calculation to lower taxes.

-

Estate Tax Computation: Detailed calculations reflecting the taxable estate.

Each section has precise requirements that must be accurately fulfilled to ensure the form is legally valid and accepted by the IRS.

Filing Deadlines and Important Dates

The form must be filed within nine months of the decedent's death. Executors can request a six-month extension for filing, but this doesn't extend the time for tax payment. Interest is charged on unpaid taxes from the original due date. Key milestones include the initial filing period and any extensions.

Required Documents

-

Death Certificate: Establishes legal proof of death.

-

Asset Valuations: Appraisals or statements.

-

Deductions Proof: Documentation for all claimed deductions.

-

Previous Tax Returns: If applicable, for reference.

Each document plays a role in substantiating the claims made within the 706-NA form.

Form Submission Methods

The 706-NA can be submitted via mail to the IRS. While digital submission options are limited for this form, ensuring the form is sent with a form of proof of mailing is advisable to confirm timely delivery.

IRS Guidelines and Interpretation

The IRS provides specific instructions for completing the 706-NA, which clarify typical points of confusion such as asset classification and valuation techniques. Their guidance should be consulted frequently to ensure compliance, especially given the unique nature of foreign estates in the U.S. taxation context.

While addressing how to use the information from the guidelines, consider consulting tax professionals experienced in international estates for definitive compliance and advisory support.