Definition & Meaning

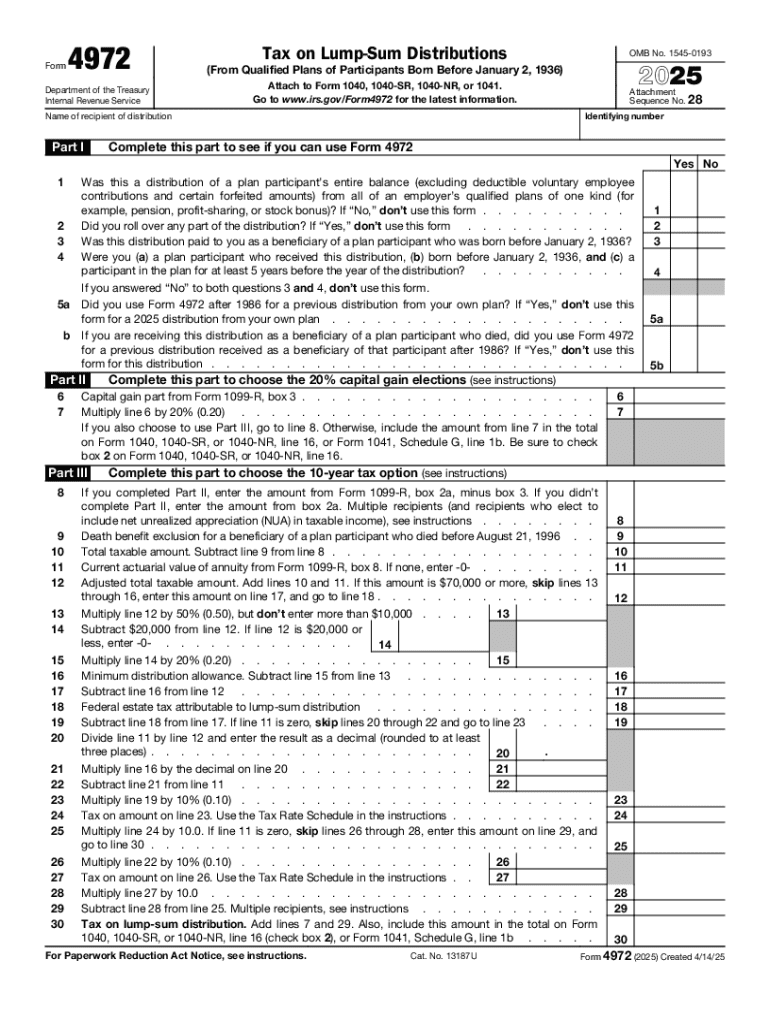

The Tax on Lump-Sum Distributions: Attach to Form 1040 refers to filing requirements for individuals who receive large, one-time payments from retirement plans. These payments are considered lump-sum distributions, and specific tax rules apply to them. Using Form 4972, taxpayers can calculate their tax on these distributions, often benefiting those born before January 2, 1936. It's crucial to report these correctly to avoid paying excess taxes as ordinary income.

Eligibility Criteria

To use the provisions available for lump-sum distributions, taxpayers need to meet specific eligibility criteria. These include being a participant in a retirement plan born before January 2, 1936. Additionally, the distribution must not have been rolled over to another retirement account. Only certain retirement plans qualify, including but not limited to pensions, profit-sharing, and stock bonus plans. Understanding these conditions ensures the correct application of tax benefits.

Steps to Complete the Tax On Lump-Sum Distributions: Attach To Form 1040

-

Gather Financial Information: Collect details on the lump-sum distribution amount and any related tax documents.

-

Determine Eligibility: Check if you qualify for special tax treatment options, such as the 20% capital gain election.

-

Calculate the Tax: Use Form 4972 to compute the tax owed, choosing between the 20% capital gain election or the 10-year tax option.

-

Fill Out Form 4972: Accurately complete all required sections, ensuring to input calculations correctly.

-

Attach to Form 1040: Include Form 4972 with your completed Form 1040 submission.

-

Double-Check Entries: Ensure figures are accurately transcribed and consistent with other tax documentation.

Important Terms Related to Tax On Lump-Sum Distributions: Attach To Form 1040

- Lump-Sum Distribution: A one-time payment received from a retirement plan.

- Ordinary Income: Regular pay subject to typical income tax rates.

- Capital Gain Election: An option to tax part of a distribution as a long-term capital gain.

- 10-Year Tax Option: Spreading the tax impact over ten years to reduce annual tax burden.

IRS Guidelines

The IRS provides clear guidelines on how lump-sum distributions must be reported. Form 4972 offers options like the 10-year tax option to ease immediate tax impact. Following IRS instructions precisely ensures compliance and optimal tax benefits. Misreporting can lead to audits and additional liabilities.

Filing Deadlines / Important Dates

The typical deadline for filing taxes, including Form 1040 with the attached Form 4972, is April 15th, unless it falls on a weekend or holiday. In such cases, the deadline shifts to the next business day. Timely filing is crucial to avoid penalties and interest charges.

Required Documents

- Form 4972: For calculating the lump-sum distribution tax.

- Form 1040: Standard individual tax form where the 4972 must be attached.

- Distributions Statement: Issued by your plan or employer, detailing received lump-sums.

- Earnings Statements: If the distribution impacts your taxable income or capital gains.

Penalties for Non-Compliance

Failing to accurately report lump-sum distributions or attach necessary forms can result in severe penalties. These include fines for underpayment, increased interest on owed taxes, and potential audits. Ensuring the thorough completion of both Form 4972 and Form 1040 mitigates these risks.

Digital vs. Paper Version

Modern taxpayers have the option to file using digital platforms or traditional paper submissions. Digital filing provides rapid confirmation and tracking via IRS-approved software. However, paper forms allow for traditional filling out methods, ideal for those with limited digital access or preferences. Regardless of method, the need for precise figures remains unchanged.

Examples of Using the Tax On Lump-Sum Distributions: Attach To Form 1040

- Retired Individual: A retiree over 80 receives a lump-sum distribution from a pension plan and uses Form 4972 to apply the 10-year tax option.

- Inherited Retirement Plan: A beneficiary born before 1936 inherits an eligible retirement plan, allowing for special tax treatment upon distribution.

- Corporate Rollover Failure: An employee fails to roll over their lump sum into a retirement account, thus needing to report it using Form 4972 for tax calculation.

Legal Use of the Tax On Lump-Sum Distributions: Attach To Form 1040

The legal use of Form 4972 is governed by federal laws designed to provide tax relief on specific distributions. Properly applying these rules affords reductions in tax liabilities, enabling compliant processing as per IRS regulations. Non-compliance could not only lead to penalties but also legal scrutiny.

Software Compatibility (TurboTax, QuickBooks, etc.)

Many tax preparation software solutions, such as TurboTax and QuickBooks, incorporate features to assist in filling out Form 4972. These tools often guide users through the process, highlighting potential benefits and compliance checks. Ensuring compatibility with your chosen software can streamline the tax filing process.