Definition & Purpose of Form 1120-POL

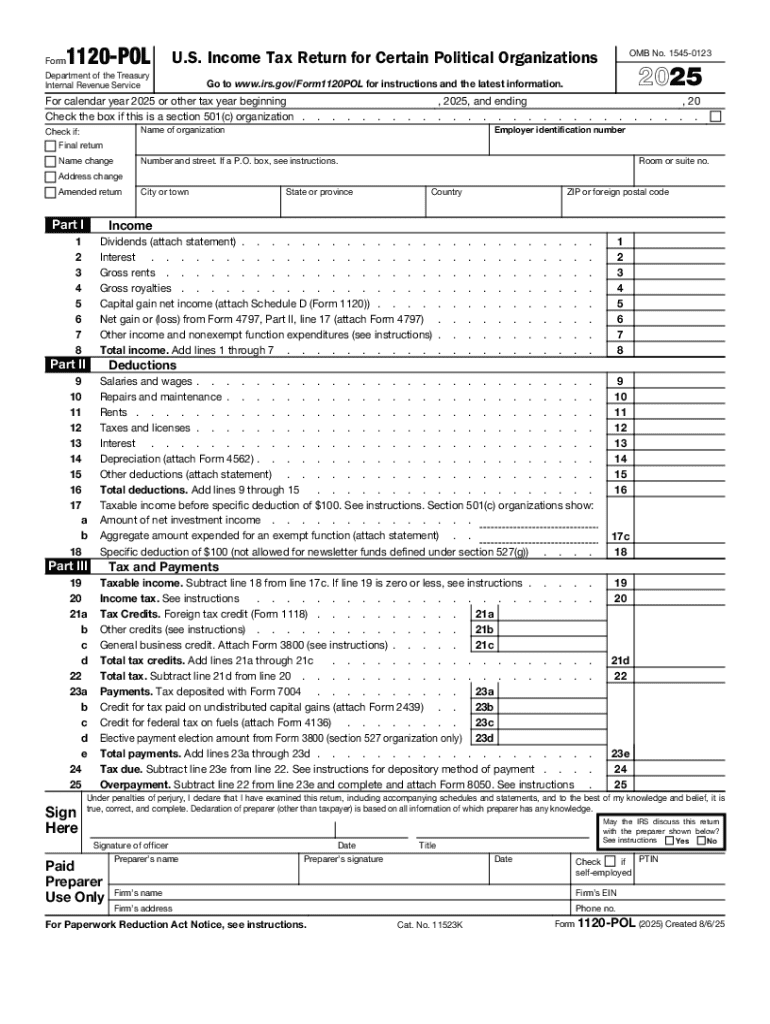

Form 1120-POL is the U.S. Income Tax Return designed for political organizations, including federal, state, and local parties. It is used to report taxable income, deductions, and tax credits, and it serves as a tool for ensuring transparency in political funding. The form is primarily intended for organizations that meet the IRS's criteria for tax-exempt political entities under section 527. The specifics reported on this form include taxable income derived from interest, dividends, and other sources not directly related to the organization's primary political activities.

What Constitutes a Political Organization?

- Defined under section 527 of the IRS code.

- Must primarily operate for the purpose of accepting contributions and making expenditures for an exempt function.

- Includes political parties, campaign committees, and political action committees.

Mandatory Filing Requirements

Organizations are required to file Form 1120-POL if they have any taxable income, defined as the gross income of an organization minus any deductions directly connected to that income. Typically, this focuses on interest or dividends – income not directly related to their exempt political activities.

Steps to Complete Form 1120-POL

Completing Form 1120-POL involves a sequential process to ensure accuracy.

-

Gather Necessary Documents: Assemble all financial documents that detail income, expenses, and deductions relevant to the tax year.

-

Fill Out Preliminary Information: Include the organization's name, address, employer identification number (EIN), and fiscal year details on the form.

-

Report Income: Record all taxable income sources, such as interest and dividends, on the appropriate lines.

-

Deduct Expenses: Identify related deductions that apply to this income; document necessary expenses that are directly attributable to earning the taxable income.

-

Calculate Taxable Income and Tax Liability: Deduct expenses from income to compute taxable income, and apply the appropriate tax rate to determine tax liability.

Ensuring Accuracy

Be attentive to detail in every entry, as even minor discrepancies can lead to an incorrect tax liability. Clarity in this process aids in minimizing potential errors or omissions.

Filing Deadlines and Important Dates

-

Form 1120-POL is due by the 15th day of the fourth month after the fiscal year ends.

-

For organizations following the calendar year, this deadline is April 15.

-

Late filing could result in penalties, making timely submission critical.

Extensions

An automatic extension of up to six months can be requested using Form 7004, though any taxes due must be paid by the original due date to avoid interest and penalties.

Who Typically Uses Form 1120-POL

Form 1120-POL is typically used by:

- Political parties and campaign committees involved in local, state, or federal elections.

- Political action committees (PACs) that engage in contributions and expenditures for political purposes.

Practical Examples

- A state political party receiving significant interest income on its deposit accounts.

- A local campaign committee investing in mutual funds as a reserve strategy for future campaigns.

Key Elements & Sections of Form 1120-POL

Form 1120-POL comprises several crucial sections:

-

Income Section: Where organizations report income not directly related to political campaign activities.

-

Deductions Section: Deduction areas allowing for costs directly associated with generating taxed income to be documented.

-

Tax Computation: The section dedicated to calculating taxes based on reported net income.

Items to Prepare

- Documented evidence of income streams.

- Details of deductible expenses.

- Previous year's tax filings for continuity.

IRS Guidelines and Instructions

The IRS provides comprehensive instructions for Form 1120-POL to assist organizations in completing the tax return accurately.

-

Instructions Cover: Definitions, detailed explanations of each line item, and examples for clarity.

-

Compliance Assurance: Helps organizations align their filing with IRS regulations to avoid penalties and facilitate smooth processing.

Available Form Submission Methods

Organizations have the option to submit Form 1120-POL through various channels:

-

Electronically: Many tax preparation software packages support e-filing.

-

Mail: Paper submissions remain an option, with appropriate mailing addresses clearly outlined by the IRS.

-

In-Person: Direct handover at IRS offices, though less common.

Ensuring Secure Submission

Regardless of the method, always include all necessary schedules and supplements to ensure full compliance and avoid delays.

Penalties for Non-Compliance

Failure to file Form 1120-POL on time, or to include all necessary information, may result in penalties.

-

Late Filing Penalties: Calculated based on the delay period and tax amounts due.

-

Incorrect Information Penalties: Applicable if the additional tax is due post-audit due to incorrect submissions.

Avoidance Strategies

Organizations should prioritize accuracy and punctuality in filing processes to minimize the risk of incurring penalties. Consider setting reminders for upcoming deadlines and maintaining comprehensive records throughout the fiscal year.