Definition & Meaning

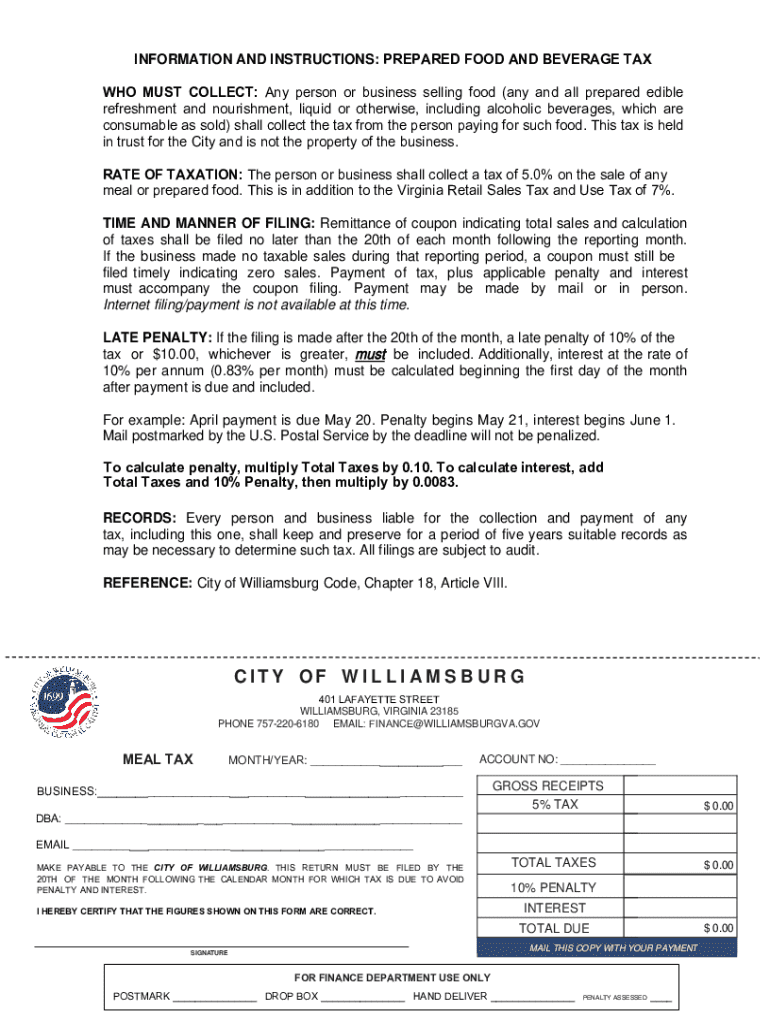

The "INFORMATION AND INSTRUCTIONS: PREPARED FOOD AND BEVERAGE TAX" form is a crucial document for businesses engaged in selling prepared foods and beverages. This form outlines the regulations and requirements for collecting and remitting taxes applicable to these sales. Typically used by local businesses, the form ensures that companies comply with the law by collecting the mandated percentage of tax from their customers, which is then remitted to the local government.

Key Elements

- Tax Rate: The form specifies the tax percentage that businesses must collect from sales. This often includes both a local tax and any applicable state sales tax.

- Remittance Process: Details the method and frequency of tax remittance to the appropriate authorities.

- Record-Keeping Requirements: Explains how businesses should maintain records of their sales and tax remittances, typically for a set period, such as five years.

How to Obtain the Form

Businesses can typically obtain the "INFORMATION AND INSTRUCTIONS: PREPARED FOOD AND BEVERAGE TAX" form through the local municipal government’s website or their tax office. Some jurisdictions may offer downloadable PDFs, while others might provide online forms that can be filled and submitted electronically.

Steps to Access

- Visit the Local Government Portal: Start by accessing the official website of the local government.

- Locate the Tax Forms Section: Navigate to the section dedicated to tax forms and business resources.

- Download or Request: Download the form if available electronically or request a physical copy through contact with the tax office.

Steps to Complete the Form

Completing the "INFORMATION AND INSTRUCTIONS: PREPARED FOOD AND BEVERAGE TAX" form entails precise calculations and accurate data entry to ensure compliance.

Detailed Procedures

- Calculate Total Sales: Determine the total amount collected from prepared food and beverage sales within the reporting period.

- Apply Tax Rate: Use the specified local and state tax rates to calculate the total tax due.

- Fill Out Tax Details Section: Enter sales and calculated tax amounts in the designated sections of the form.

- Verify Information: Ensure all entries are accurate to prevent potential miscalculations and penalties.

- Submit by Deadline: Submit the completed form by the due date along with the tax payment.

Who Typically Uses the Form

The form is primarily used by entities engaged in the food service industry. This includes:

Business Types

- Restaurants: Both casual and fine dining establishments that prepare and serve food.

- Cafés and Coffee Shops: Vendors providing prepared beverages and snack items.

- Catering Services: Businesses that deliver prepared meals for events.

- Bars and Pubs: Establishments focusing on beverage service.

Important Terms Related to the Form

Understanding the terminology associated with the "INFORMATION AND INSTRUCTIONS: PREPARED FOOD AND BEVERAGE TAX" is essential for accurate compliance.

Key Terms

- Prepared Food: Refers to any food item that has been cooked, heated, or prepared for immediate consumption.

- Beverages: Includes both alcoholic and non-alcoholic drinks sold for consumption on or off the premises.

- Tax Remittance: The process of sending collected taxes to the appropriate governmental authority.

Filing Deadlines and Important Dates

Timely submission of the "INFORMATION AND INSTRUCTIONS: PREPARED FOOD AND BEVERAGE TAX" form is critical.

Key Deadlines

- Monthly Filing: Most jurisdictions require businesses to file monthly, usually by the 20th of each month.

- Year-End Reporting: Some regions may require an additional annual summary report by the end of the fiscal year.

Penalties for Non-Compliance

Failure to comply with the requirements or deadlines of the "INFORMATION AND INSTRUCTIONS: PREPARED FOOD AND BEVERAGE TAX" can result in penalties.

Potential Consequences

- Late Fees: A percentage of the tax due may be added as a penalty for late payment.

- Interest on Unpaid Taxes: Accrued interest on overdue tax payments.

- Potential Audits: Businesses failing to comply can be subject to audits, which can further result in additional fines or legal action.

State-Specific Rules

Though the "INFORMATION AND INSTRUCTIONS: PREPARED FOOD AND BEVERAGE TAX" form provides a general framework, individual states may have specific rules that alter how the form is completed or filed.

Regional Variations

- Tax Rates: These may differ based on city or county within a state.

- Exemptions: Certain states may provide exemptions for particular types of food or beverage.

- Filing Frequency: Some states might have different reporting periods, ranging from monthly to quarterly filings.