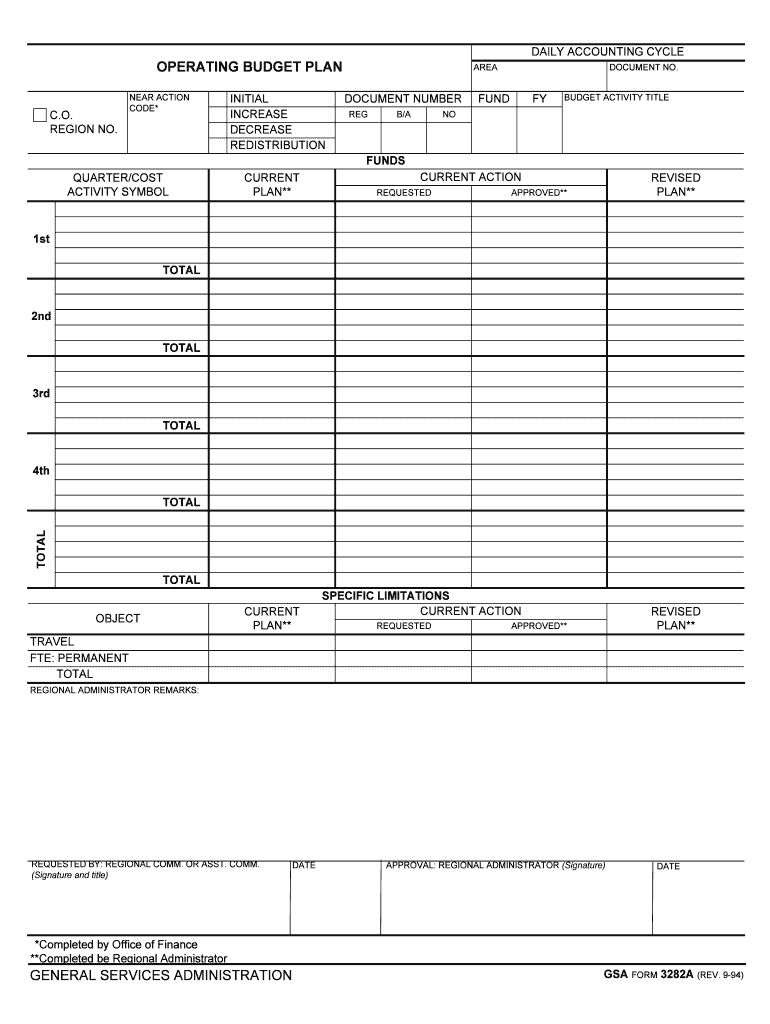

Definition & Meaning

The "Operating Budget Plan" is a financial document that outlines the projected revenue and expenditures for a specific period, typically one fiscal year. It plays a critical role in financial planning processes, providing a framework for allocating resources efficiently within an organization. Organizations use it to track their financial status, plan for future growth, and ensure compliance with financial obligations. This document is crucial for strategic decision-making, allowing businesses to align their operational goals with financial realities.

Steps to Complete the Operating Budget Plan

-

Gather Financial Data: Start by collecting historical financial data, including past budgets, income statements, and cash flow records. This information helps establish baseline projections for future periods.

-

Project Revenues: Estimate the potential revenue by examining past performance, market trends, and economic conditions. Consider different scenarios, such as optimistic, pessimistic, and most likely cases.

-

Estimate Expenses: Break down expenses into categories, such as fixed costs (rent, salaries) and variable costs (utilities, supplies). Using historical data, forecast these expenses for the upcoming period.

-

Analyze Variances: Identify any discrepancies between projected figures and historical data. This analysis helps refine assumptions and improve the accuracy of future budget plans.

-

Review & Approve: Once the budget is drafted, it should be reviewed by relevant departments or committees. After revisions and consensus, the budget is formally approved by organizational leaders.

-

Implementation & Monitoring: Implement the budget by aligning departmental activities with the budget plan. Regularly monitor performance against the budget and make adjustments as needed.

Key Elements of the Operating Budget Plan

-

Revenue Projections: Includes expected income from all sources, such as sales, investments, and grants. Accurate forecasting is essential for effective budget planning.

-

Fixed and Variable Costs: Clearly distinguish between costs that remain consistent over time and those that fluctuate with usage or external factors.

-

Capital Expenditures: Account for major purchases or investments in assets, such as property, equipment, and technology, which can impact cash flow and future profitability.

-

Contingency Funds: Allocate a portion of the budget for unexpected expenses to reduce financial strain during emergencies or unforeseen events.

-

Departmental Budgets: Break down the overall budget into specific allocations for each department, ensuring targeted and efficient use of resources.

Who Typically Uses the Operating Budget Plan

Operating budget plans are most commonly used by:

-

Business Executives: To guide strategic planning and make informed decisions about resource allocation.

-

Financial Analysts: For analyzing trends, evaluating financial health, and recommending adjustments to improve financial performance.

-

Department Managers: To control and monitor their respective areas’ spending, aligning with broader organizational goals.

-

Board Members and Investors: To assess the organization's financial strategies and ensure robust fiscal management.

Examples of Using the Operating Budget Plan

-

A Retail Business: Analyzing the budget before launching a new product line, ensuring that projected costs, marketing expenditure, and additional staffing align with expected revenue increases.

-

A Non-Profit Organization: Using the budget to allocate donor funds effectively across various projects, ensuring administrative costs do not exceed allocated limits.

-

A Tech Startup: Preparing an operating budget to secure venture capital funding, demonstrating a clear financial roadmap and prudent resource allocation.

Legal Use of the Operating Budget Plan

For many organizations, the operating budget plan is not just a management tool but a legal document that must comply with financial regulations. It may be subject to internal audits and is often required for:

-

Grant Applications: Non-profits must demonstrate fiscal responsibility, typically shown through a detailed budget plan, to qualify for government or private grants.

-

Regulatory Compliance: Public companies must adhere to financial reporting standards, using comprehensive budget plans to provide transparency to shareholders and regulatory bodies.

-

Contractual Obligations: Various contracts may require regular budget reporting to demonstrate adherence to financial commitments.

Software Compatibility

The operating budget plan can be crafted using various software tools to enhance accuracy and facilitate collaboration. These tools include:

-

Spreadsheet Applications: Programs like Microsoft Excel and Google Sheets offer robust capabilities for creating customized templates, running calculations, and conducting "what-if" scenarios.

-

Accounting Software: Platforms such as QuickBooks and TurboTax allow businesses to seamlessly integrate financial transactions into the operating budget, ensuring real-time updates and insights.

-

Document Management Systems: Services like DocHub facilitate the sharing, review, and approval process of budget plans, protecting sensitive information with encryption and secure access protocols.

State-specific Rules for the Operating Budget Plan

While operating budget plans maintain a universal structure, certain elements may vary based on state-specific regulations:

-

Tax Regulations: Each state may have unique tax codes impacting how revenue and expenses are reported within an operating budget.

-

Grant Compliance: State-level grants may impose specific requirements for budget formats, categories, and financial disclosures.

-

Non-Profit Reporting: Non-profit organizations may adhere to additional state-mandated financial reporting guidelines, impacting the structure and content of their budget plans.

Business Types That Benefit Most from Operating Budget Plans

Different business entities derive distinct advantages from using structured operating budget plans:

-

Large Corporations: Utilize detailed budgets to coordinate cross-departmental activities and assess risk and return on investments.

-

Small Businesses: Benefit from operating budgets by streamlining expenditures, projecting growth, and securing financing based on proven financial projections.

-

Non-Profit Entities: Rely on budget plans for transparency and accountability in fund allocation to maintain donor trust and satisfy regulatory oversight.