Definition and Purpose of the Closing Statement Form

The closing statement form is an essential component in real estate transactions, particularly in the United States. This document outlines the financial agreements between the buyer and the seller, ensuring that all parties have a clear understanding of the incoming and outgoing funds. Key information typically includes the sales price, expenses, and any necessary adjustments or balances that the parties need to account for, whether payable or receivable. By clearly documenting the financial details, the closing statement form helps prevent disputes and ensures legal compliance in real estate transactions.

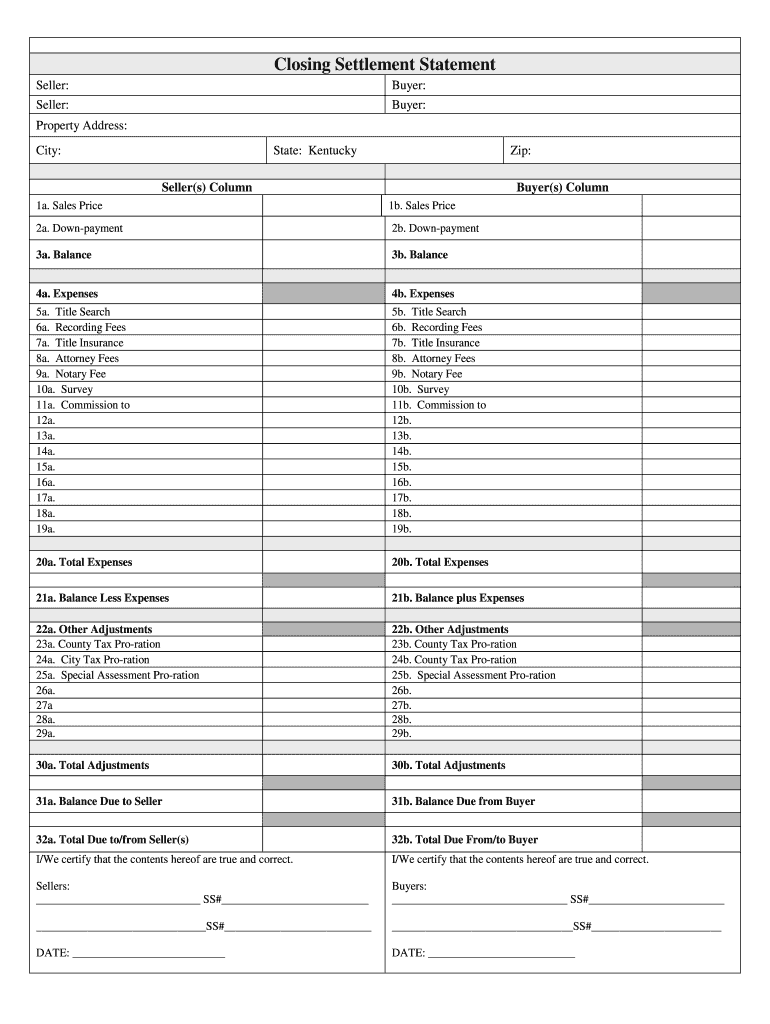

Key Components

- Sale Price: The agreed-upon amount for the property.

- Down Payment: The initial payment made by the buyer toward the purchase price.

- Expenses: Costs related to the transaction, such as inspection fees, closing costs, and taxes.

- Adjustments: Any necessary changes to the financial details, which can include things like prorated property taxes or utility bills.

- Balances: Outlines any remaining amounts payable to or receivable from the involved parties.

Importance

Ensuring that each section of this form is accurate and complete is crucial for both legal and financial reasons. An accurate closing statement form protects all parties involved by recording the exact terms of financial obligations and agreements. It serves as a legal document, should any questions arise post-transaction.

Steps to Complete the Closing Statement Form

Filling out a closing statement form requires careful attention to detail to ensure all financial transactions are correctly noted. The steps generally follow a standard procedure but may vary slightly depending on jurisdiction.

-

Identify Parties: Clearly list the names and contact information of the buyer and seller, along with any agents involved.

-

List the Purchase Price: Provide the final purchase price as agreed upon in the purchase agreement.

-

Include Financial Details: Add items such as the down payment, earnest money deposit, and loan amounts.

-

Document Expenses: Itemize all relevant costs, including broker fees, legal services, appraisal fees, and title insurance.

-

Adjust for Prepaid Items: Include adjustments for prepaid taxes or homeowner's association fees, and detail any expenses shared by the buyer and seller.

-

Review and Sign: Both parties need to review the document critically, ensuring that all entries are correct before signing to validate its accuracy.

Practical Tips

- Double-check calculations to prevent errors in financial reporting.

- Keep communication open with involved parties to promptly address discrepancies.

- Utilize software tools that integrate with popular tax and accounting applications to streamline the completion process.

State-Specific Rules for the Closing Statement Form

Closing statement forms may have state-specific requirements, given that real estate practices can vary across the United States. Some states have unique protocols that must be adhered to during property transactions.

Kentucky Example

In Kentucky, the closing statement form must reflect all financial exchanges involved in the transaction. This includes local tax implications and state-specific disclosures related to the property. Transactions often require signatures from both buyer and seller as an affirmation of the statement's accuracy.

Additional Considerations

- Research Local Laws: Verify any state-specific disclosures or representations required on the form.

- Seek Legal Advice: Consulting with a legal professional can ensure compliance with state-specific requirements.

- Check for Updates: Real estate laws can evolve, making it crucial to use the most current version of forms and adhere to the latest regulations.

Legal Use and Implications

Using the closing statement form appropriately ensures compliance with legal standards in real estate transactions. This form not only acts as a blueprint for the financial interchange between the buyer and seller but also complies with governmental regulations, providing protection to all parties involved.

Compliance and Regulation

- Uniform Practices: Real estate transactions often follow standardized forms to ensure consistency and fairness in documenting financial exchanges.

- Government Standards: Adherence to federal and state laws, such as the ESIGN Act for digital transactions, mandates legal sanctioning of documents.

- Audit Trail: Creates a record of all details involved in the transaction, which is necessary for both personal and legal review.

Consequences of Failure

Failure to properly complete or sign a closing statement form can lead to legal disputes, financial penalties, or delays in property ownership transfer. Ensuring accuracy and completeness is not just best practice but a legal necessity.

Variations and Alternatives

In real estate, there might be variations or updated versions of the closing statement form that reflect changes in the law or new financial practices. Familiarity with the current form type and any alternatives is vital.

Common Types

- Standard Closing Statement: The most frequently used format in residential transactions, laying out the particulars of sales and expenses.

- HUD-1 Settlement Statement: This variant is occasionally used for certain real estate transactions, documenting similar details with a slightly different format.

Digital vs. Paper

- Digital versions of closing statement forms are becoming more prevalent due to their ease of use, efficiency, and ability to integrate into existing software systems.

- Paper copies continue to be used in some contexts, especially to meet legal requirements or personal preferences for hard-copy documentation.

Digital Compatibility and Software Integration

The digital revolution in real estate documentation has seen increased use of software tools that support closing statement forms. These provide enhanced flexibility, security, and efficiency in processing and storing real estate transaction data.

Popular Software Compatibility

- TurboTax and QuickBooks: Tools like these often incorporate features that allow you to import real estate financial data directly from digital forms into tax or accounting applications.

- DocHub: Offers capabilities for editing, signing, and sharing forms directly within the platform, eliminating the need to switch between multiple applications.

Benefits of Digitization

- Enhanced Security: Digital signatures comply with federal standards, providing legality and authenticity.

- Efficiency: Instant document processing and sharing simplifies the traditional workflow.

- Accessibility: Cloud-based systems offer access from any device, anywhere, increasing convenience for all parties.

Who typically uses the Closing Statement Form

The primary users of the closing statement form are the parties involved in a real estate transaction. Each party plays specific roles, requiring them to engage with this crucial document.

Key Stakeholders

- Buyers: Individuals or entities purchasing the property who need to verify all costs and payments.

- Sellers: Property owners responsible for acknowledging expenses and receiving payment.

- Real Estate Agents: Facilitators between buyers and sellers who must ensure the form accurately reflects the agreed terms.

- Legal Professionals: Attorneys reviewing for legality and completion to meet statutory requirements.

- Lenders: Financial institutions providing loans will often require a closing statement to finalize the loan.

Understanding who uses the form and their responsibilities ensures all parties complete and understand their roles in real estate transactions effectively.