Definition and Meaning of Qualified Dividends and Capital Gain

The term "qualified dividends and capital gain" refers to dividends and capital gains that meet specified conditions under U.S. tax law, allowing them to be taxed at a lower rate compared to ordinary income. Qualified dividends are those received from holdings in U.S. corporations or qualified foreign corporations, provided that the investment duration meets minimum holding period requirements. For capital gains, qualifying refers to the classification of an asset's sale as a long-term capital gain if held for more than one year, thereby benefiting from favorable tax treatment.

Examples of Qualified Dividends

- Dividends from investments in a domestic corporation

- Dividends from foreign corporations eligible under U.S. tax treaties or foreign investments with ADRs

- Special dividends from mutual funds or ETFs that meet IRS qualifications

Capital Gain Considerations

- Gains from selling stocks held for over a year

- Profits from real estate transactions where the property was owned for a long-term period

- Long-term gains from bond sales, subject to specific tax regulations

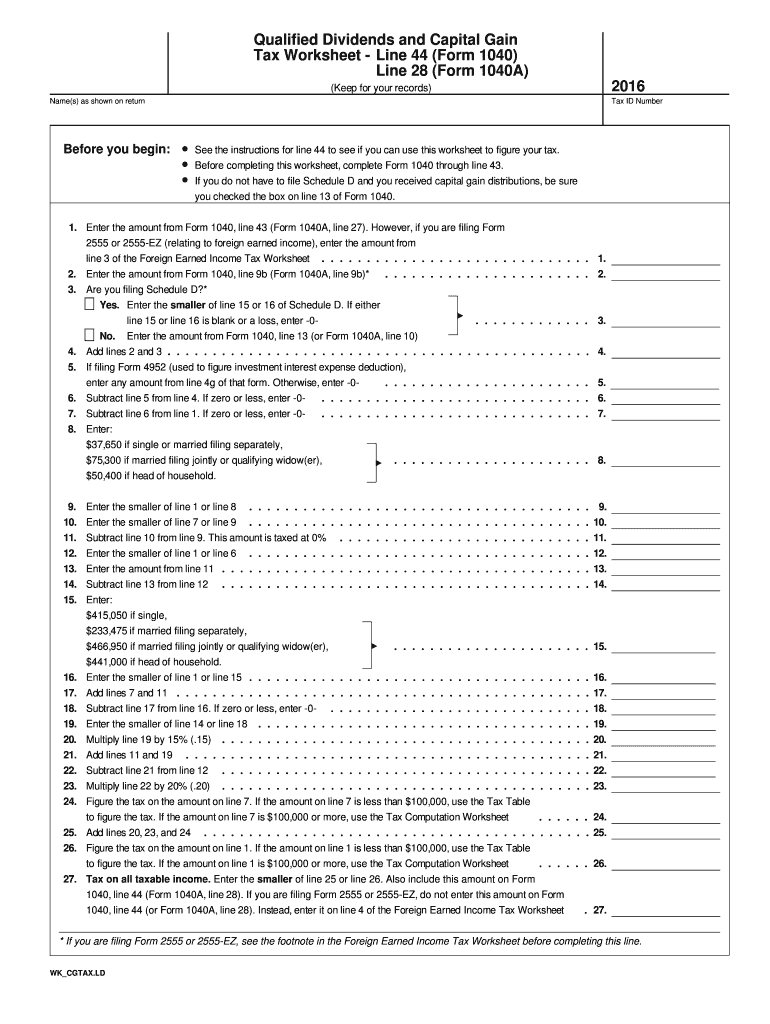

Steps to Complete the Qualified Dividends and Capital Gain Worksheet

Completing the Qualified Dividends and Capital Gain Tax Worksheet requires detailed attention to entries on IRS forms. Follow these steps for precise calculations:

- Determine Filing Status: Identify whether you are filing as single, married filing jointly, head of household, etc.

- Calculate Total Income: Sum all sources of income, including qualified dividends and capital gains.

- Review Schedule D Usage: Assess if you need to file Schedule D, which reports capital gains and losses.

- Examine Tax Bracket Impact: Depending on your taxable income, calculate the rate applicable to your qualified dividends and capital gains.

- Work Through the Worksheet: Follow each step on the worksheet, entering amounts on specified lines related to your filing status and conditions.

- Complete Tax Form 1040 or 1040A: Enter results on your final tax return.

Key Elements of Qualified Dividends and Capital Gain Worksheet

This worksheet plays a critical role in determining tax liability related to dividends and capital gains. Key elements include:

- Form 1040, Line 9b: Use this to report qualified dividends specifically.

- Form 1040, Line 13: For reporting capital gains, whether Schedule D is necessary or not.

- Income Thresholds: Based on filing status, threshold impacts tax rates on dividends and gains.

- Holding Period Requirements: A minimum holding duration to qualify dividends/capital gains for reduced rates.

IRS Guidelines for Qualified Dividends and Capital Gains

The IRS provides specific guidelines for understanding and reporting qualified dividends and capital gains:

- Publication 550: Comprehensive details on taxation of investment income and expenses.

- Publication 17: General tax guide for individuals, covering dividend and capital gain taxation.

- Schedule D Instructions: Provides guidance on completing Schedule D, linked to Form 1040 or 1040A.

Important Considerations

- Tax Rate Alignment: Understanding when gains move into higher or lower tax brackets is crucial.

- Form Filing Accuracy: Ensure all lines are correctly filled to avoid IRS audits or penalties.

Required Documents for Reporting

Accurate filing entails gathering various documents. Essential documents include:

- 1099-DIV Forms: From investment companies, reporting dividends paid

- 1099-B Forms: For reporting gains and losses from brokered asset sales

- Previous Tax Returns: As a point of reference for continuity and accuracy

Penalties for Non-Compliance

Non-compliance with taxation requirements on qualified dividends and capital gains can lead to significant penalties:

- Late Filing Fees: If your return is filed after the due date without an extension.

- Filing Misinformation Penalties: Incorrect entries on forms or worksheets may incur fines.

- Interest on Amounts Due: Accrued interest on taxes owed if not settled by the deadline.

Eligibility Criteria for Favorable Tax Treatment

Eligibility for reduced tax rates is determined by several factors:

- Investment Holding Period: Dividends or capital assets must meet IRS-defined periods.

- Source of Dividends: Must originate from a qualified entity as defined by the IRS.

- Owner Residency status: Affects eligibility and potential treaty benefits.

Taxpayer Scenarios for Practical Understanding

Various taxpayer scenarios exemplify how qualified dividends and capital gains affect taxes:

Scenario 1: Retired Individual

- Income Mix: Predominantly from dividends, reflecting a need to strategically manage tax impact.

- Tax Planning: Leveraging long-term capital gains for extended financial planning.

Scenario 2: Self-Employed Individual

- Diversified Investments: May balance capital gains against taxable self-employment income.

- Schedule D Relevance: Critical for accurate reporting of business-related investment transactions.

These structured insights into qualified dividends and capital gains equip taxpayers with the necessary knowledge to navigate their filings effectively, ensuring compliance and optimizing tax outcomes.