Definition and Meaning of Louisiana Revised Statutes Tit 47,297.13

Louisiana Revised Statutes Tit 47,297.13 outlines a tax deduction program aimed at encouraging employers in Louisiana to hire qualified individuals with disabilities. This statute serves as a legislative framework that enables businesses to receive financial benefits by deducting a portion of wages paid to these employees. The intent is to support both economic growth and inclusive employment practices by providing a tangible incentive for businesses to employ individuals who may have been underserved in traditional employment markets.

How to Use the Tax Deduction

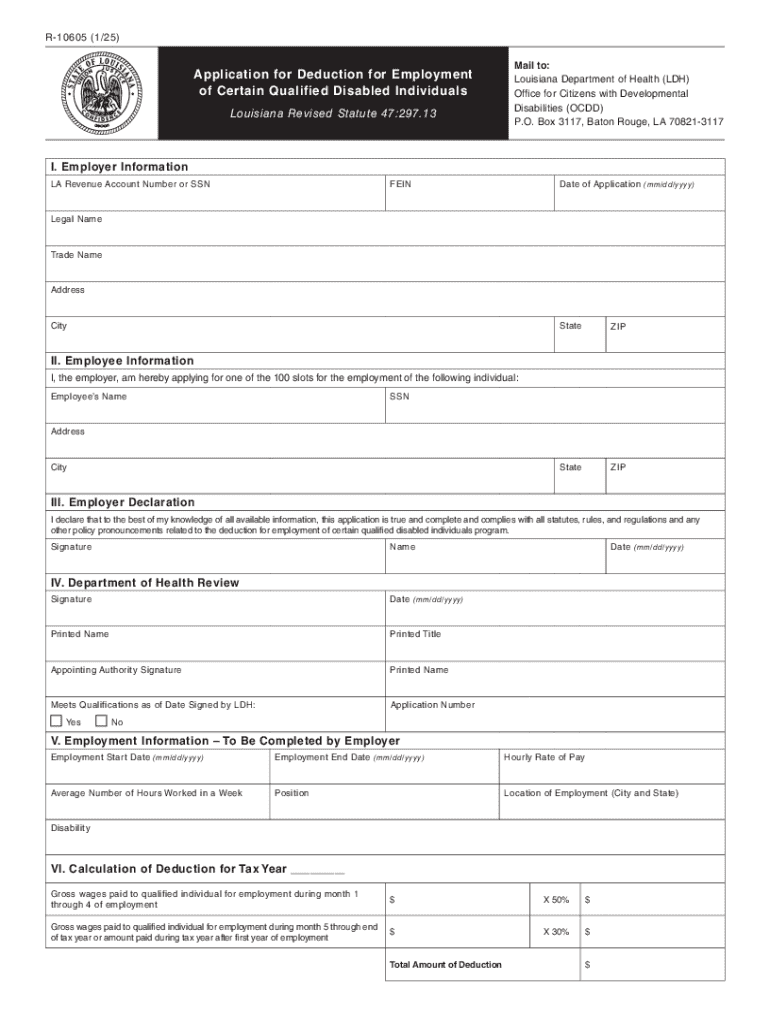

Understanding the process to utilize the tax deduction under Louisiana Revised Statutes Tit 47,297.13 is crucial for employers. Businesses can claim the deduction as part of their annual state tax filings. The deduction is structured to benefit employers financially by allowing them to deduct 50% of the gross wages paid to each qualified employee during the initial four months of employment, followed by a 30% deduction for subsequent months. Employers must ensure compliance with the guidelines in the statute to claim these benefits effectively.

Steps to Complete the Louisiana Revised Statutes Tit 47,297.13 Tax Deduction

- Verify Eligibility: Confirm that both the employer and employee meet the eligibility criteria specified in the statute.

- Gather Necessary Documentation: Ensure all relevant employee information and wage records are properly documented.

- Calculate Deduction: Compute the wage deduction based on the structured percentages (50% for the first four months and 30% thereafter).

- Complete Tax Filing: Integrate the calculated deduction into the state tax filing process.

- Submit Documents: Send all required forms and documentation to the appropriate state authority by the filing deadline.

- Maintain Records: Keep detailed records of all relevant information in case of future audits or inquiries.

Eligibility Criteria for the Deduction

- Employers: Any business operating within the state of Louisiana can potentially take advantage of this deduction.

- Employees: The individual employed must qualify as a person with a disability, as defined within the legal framework.

- Employment Status: The employee must be hired by the employer, and wages should be documented and compliant with the law to qualify for deductions.

Important Terms Related to Louisiana Revised Statutes Tit 47,297.13

- Gross Wages: The total amount paid to a qualified employee before any deductions.

- Qualified Individual: A person with disabilities recognized under state legislation.

- Deduction Limit: The cap on the number of qualified individuals (100 per employer) who can be accounted for under this deduction annually.

Key Elements of the Tax Deduction

- Financial Incentives: Encourages businesses to employ individuals with disabilities through wage deductions.

- Structured Benefits: Provides specific percentages that dictate how much can be deducted based on the employee's tenure.

- Legal Compliance: Requires detailed record-keeping and adherence to state laws to avoid penalties.

Examples of Using the Tax Deduction

A manufacturing business in Baton Rouge hiring ten qualified employees with disabilities can maximize its tax benefits by calculating the wage deductions accurately. For example, if Employee A earns $3,000 monthly, the employer can deduct $1,500 for the first four months and $900 monthly thereafter. This real-world application illustrates how the statute incentivizes inclusivity while offering financial relief.

State-Specific Rules

Businesses must be aware of specific laws and requirements that accompany this tax deduction under Louisiana's jurisdiction. Given that this deduction is state-specific, employers should consult state guidelines and potentially seek legal or accounting advice to ensure full compliance with Louisiana statutes.

Penalties for Non-Compliance

Failure to accurately implement the deduction in accordance with Louisiana Revised Statutes Tit 47,297.13 can result in penalties. Non-compliance can include incorrect deduction calculations, improper documentation, or failure to meet deadlines—each potentially leading to financial penalties or loss of deduction privileges. Proper adherence to the legal framework is essential for employers wishing to benefit from this tax incentive.