Definition and Purpose of the K-120 Form

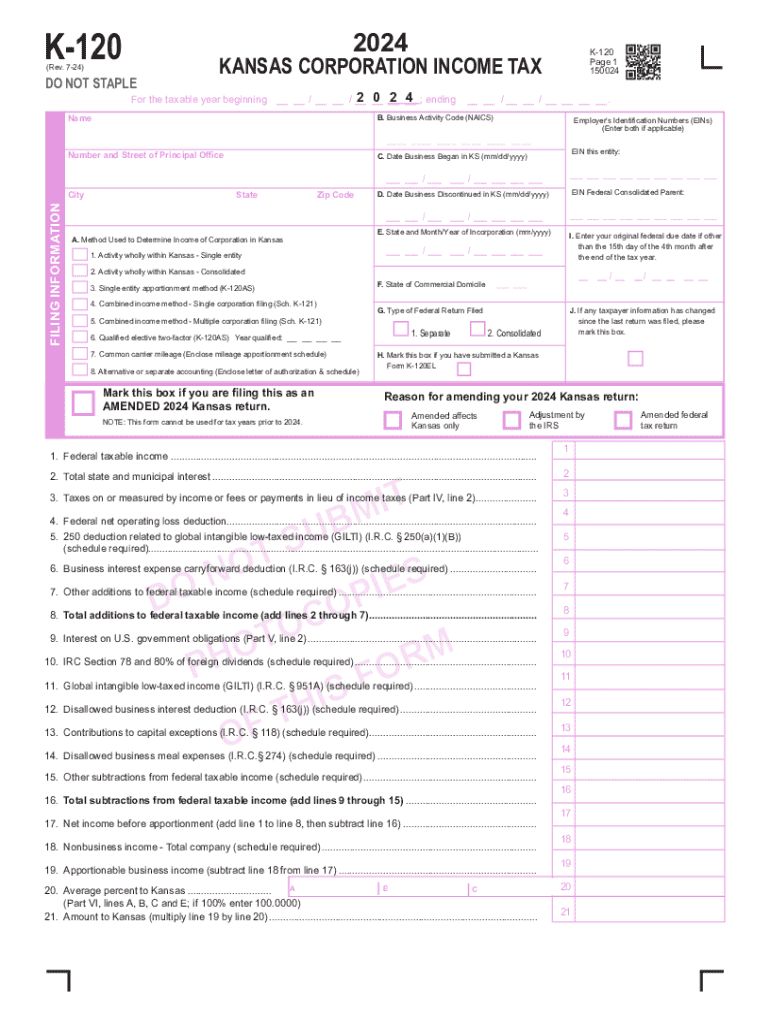

The K-120 form is a crucial document used for filing the Kansas Corporation Income Tax for the tax year 2024. Specifically designed for corporate entities operating within Kansas, this form collects comprehensive information required for calculating and reporting state income tax obligations. It includes sections for income determination, apportioning income, and claiming applicable tax credits. Notably, this form requires corporations to disclose business activities, income sources, and organizational changes since the previous filing. The primary purpose of the K-120 is to ensure accurate tax reporting and compliance with Kansas state taxation laws.

Steps to Complete the K-120 Form

-

Gather Necessary Documents: Before completing the K-120, collect all relevant financial documents, including previous tax returns, income statements, and records of any business changes or transactions.

-

Filing Information: Start by filling in the basic information section. This includes the corporation’s legal name, address, Federal Employer Identification Number (FEIN), and other identification details relevant to the tax filing.

-

Income Determination: Calculate the corporation's taxable income. This involves itemizing all income sources and applying deductions as prescribed by Kansas tax law.

-

Apportionment and Allocation: If the corporation operates in multiple states, calculate the portion of income attributable to Kansas. This is crucial for accurately reporting state-specific income.

-

Calculate Tax and Credits: Determine the tax due based on the calculated income. Then, apply any eligible nonrefundable and refundable tax credits to reduce the overall tax liability.

-

Final Review and Submission: Ensure all sections are complete and accurate. Submit the form by the specified deadline either online, via mail, or in-person delivery.

Eligibility Criteria for the K-120 Form

Corporations operating in Kansas, regardless of size or industry, are required to file the K-120 form if they earn any income that is subject to state tax. Key eligibility criteria include:

- Corporations domiciled or operating in Kansas

- Entities with income sourced from within the state

- Corporations required to report any changes in business structure or operations

Eligibility also extends to entities that are required to apportion income due to multi-state operations.

Key Elements of the K-120 Form

The K-120 form is composed of distinct sections, each tailored to capture detailed financial information:

- Filing Information: Identification and contact details of the corporation.

- Income Determination: Breakdown of total income and deductions.

- Apportionment Details: Methods for determining Kansas-specific income.

- Tax Calculation: Procedures for calculating taxable income and applicable rates.

- Credits and Payments: Details on tax credits and payment information for refunds or liabilities.

Important Terms Related to the K-120

To effectively complete the K-120, it is vital to understand specific terms:

- Apportionment: Method used to assign income to the state of Kansas for tax purposes.

- Nonrefundable Credits: Tax credits that reduce liability but do not result in a refund if they exceed the tax owed.

- Refundable Credits: Tax credits that can result in a refund if they exceed tax liability.

Filing Deadlines and Important Dates

The K-120 form must be filed annually by the standard corporate tax return deadline. For the tax year 2024, the due date is April 15, 2025. Corporations not meeting this deadline may face penalties for late submissions. Extensions may be granted upon request, but interest may accrue on any unpaid taxes.

Penalties for Non-Compliance with the K-120

Failing to file the K-120 form by the deadline can result in significant penalties. These can include:

- Late Filing Penalty: A percentage of the tax due applied monthly for failure to file on time.

- Interest on Unpaid Taxes: Accrues daily on any taxes not paid by the due date.

- Additional Penalties: Imposed for providing misinformation or attempting to evade tax obligations.

Avoidance of these penalties ensures compliance and safeguards the corporation’s reputation.

State-Specific Rules for the K-120

Kansas imposes specific rules regarding income apportionment and tax credits that differ from federal tax guidelines. Understanding these distinctions is critical:

- Kansas Apportionment Formula: Unique method for determining the portion of income attributable to Kansas operations.

- State-Specific Credits: Availability of credits that are unique to Kansas, impacting the overall tax liability.

Comprehensive understanding of these rules aids in accurate filing and maximizes potential tax benefits.