Definition and Purpose of the ES-40

The ES-40 form is issued by the Indiana Department of Revenue and is specifically used for making estimated tax payments for the year 2025. Designed to facilitate the process of paying taxes in advance, the form is crucial for taxpayers who anticipate a tax liability at year-end and wish to manage their payments more effectively over time. By projecting their owed taxes throughout the fiscal year, individuals and businesses can avoid large, lump-sum payments during tax season, or penalties associated with underpayment.

How to Use the ES-40

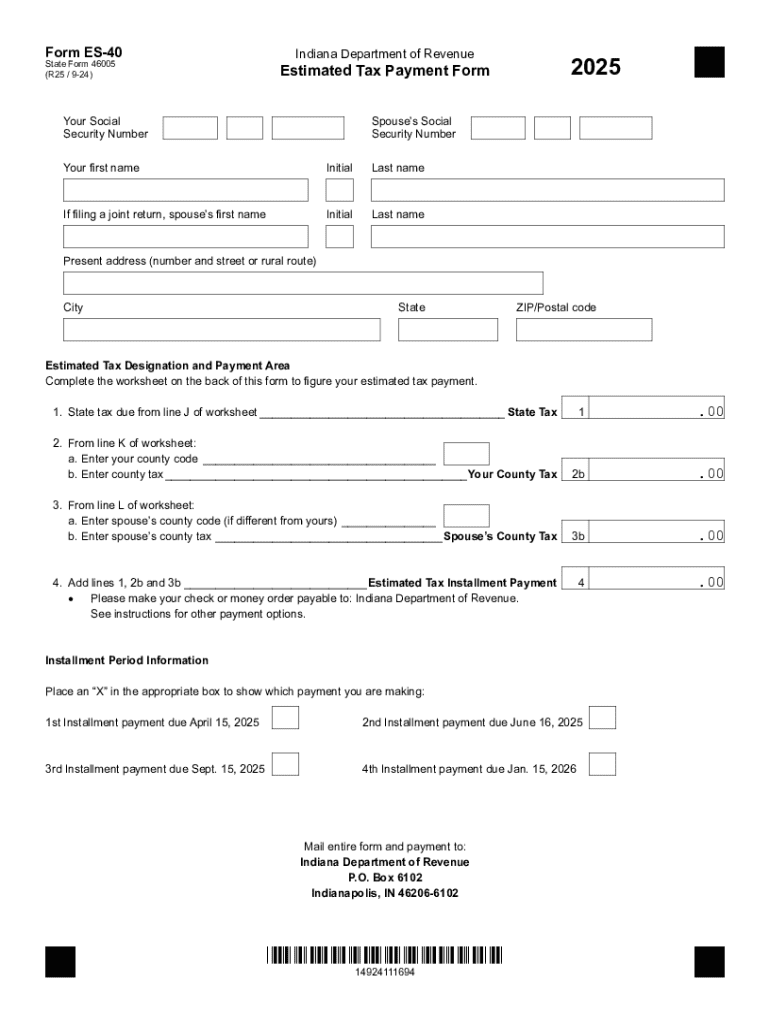

Using the ES-40 form involves a series of steps to ensure that estimated tax payments are accurately calculated and submitted. Taxpayers must complete a worksheet that is integral to the form, which guides them in determining their estimated tax liability. This involves evaluating income sources, deductions, and credits that apply for the tax year. Once calculated, taxpayers can use the provided payment instructions to remit their taxes in four scheduled installments. Understanding each step is essential for compliance and financial planning, helping to avoid errors or potential underpayment penalties.

Steps to Complete the ES-40

Completing the ES-40 involves:

-

Gathering Financial Documents: Include income statements, previous tax returns, and any relevant deduction or credit information.

-

Estimating Income and Deductions: Utilize the worksheet on the form to project your taxable income, calculated by subtracting eligible deductions from gross income.

-

Calculating Tax Liability: Apply the projected income figure against the estimated tax rates for Indiana to determine the expected liability.

-

Dividing Payments: Split the annual tax liability into four equal parts, representing the quarterly payments required.

-

Writing Payments: Clearly fill out the payment voucher for each installment, ensuring accuracy in taxpayer information and payment amounts.

-

Submission: Follow the form’s instructions to send your payment, either via mail or electronic means, by the specified due dates.

Taxpayers should make refinements to their estimates as needed throughout the year if income levels or tax laws change.

Important Terms Related to the ES-40

Understanding key terminology associated with the ES-40 can enhance the accuracy of tax payments, including:

- Estimated Tax: The method of prepaying taxes on income not subject to withholding.

- Tax Liability: The total amount of tax owed to the state, based on taxable income.

- Deductions and Credits: Financial reductions that decrease taxable income or overall tax due.

- Installments: Quarterly payments made to satisfy estimated tax obligations throughout the year.

These terms help frame the financial and procedural aspects of estimated tax payment, ensuring tax compliance.

Legal Use and Compliance with the ES-40

The ES-40 is legally grounded in the requirement for taxpayers in Indiana who expect to owe taxes to remit estimates quarterly. The section of U.S. tax law that governs estimated payments stipulates adhering to these payment cycles to avoid underpayment penalties. Compliance involves correctly calculating payments and meeting deadlines. Law mandates that taxpayers maintain accurate records throughout the year, justifying the estimated amounts used on the form.

Filing Deadlines and Important Dates

Timely submission is crucial for the ES-40 to avoid penalties:

- Quarter One: Payment due on April 15th.

- Quarter Two: Payment due on June 15th.

- Quarter Three: Payment due on September 15th.

- Quarter Four: Payment due on January 15th of the following year.

Each payment deadline reflects the end of a fiscal quarter. Meeting these deadlines is imperative to remain in compliance with Indiana's tax regulations.

Required Documents for the ES-40

Key documents necessary for accurate completion of the ES-40 include:

- Income Statements: Pay stubs, royalty contracts, rental income records.

- Prior Year Tax Returns: To predict taxable income and access prior usage of deductions and credits.

- Documentation of Deductions and Credits: Proof of eligible expenses and claims.

Having these documents prepared and reviewed aids in enhancing accuracy and minimizing errors in tax estimates.

Penalties for Non-Compliance

Non-compliance with ES-40 requirements can result in:

- Underpayment Penalties: If taxpayers do not pay at least 90% of the current year’s tax liability through withholding or estimated payments.

- Interest Charges: Levied on unpaid estimated taxes, calculated on the outstanding balance.

- Additional Penalties: For missing payments on listed deadlines without valid extensions or exemptions.

Adhering to prudent review processes and timely submissions reduces risk of penalties.