Definition & Meaning

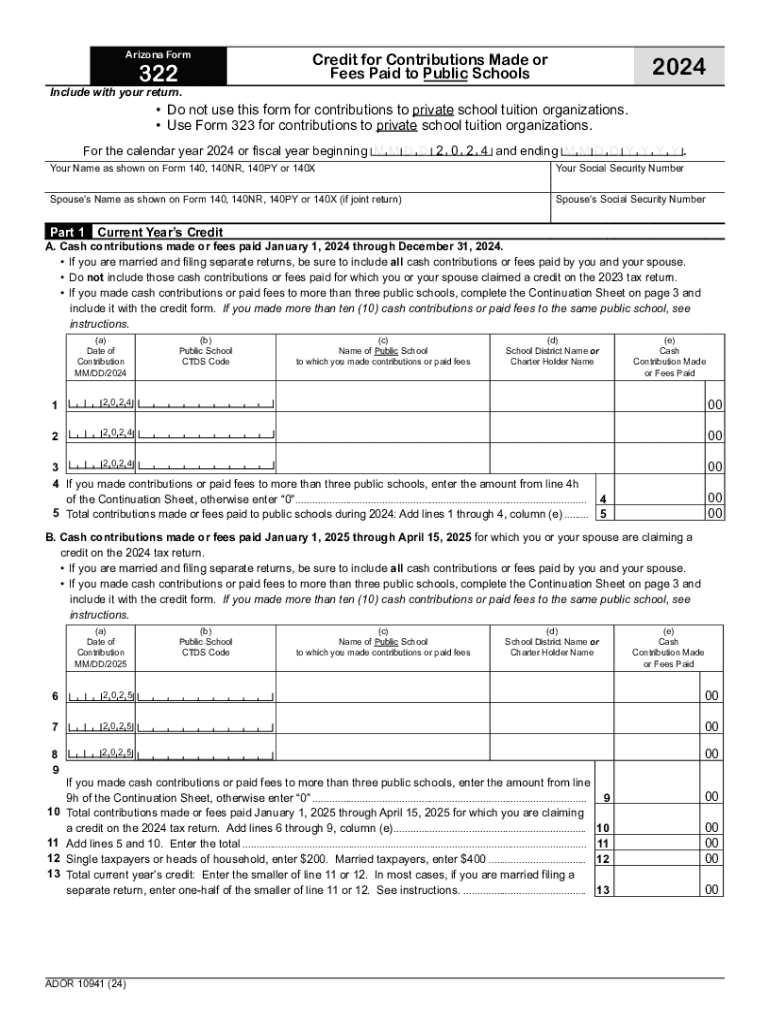

Arizona Form 322 is a tax document specifically devised for Arizona taxpayers who wish to claim a credit for contributions made to public schools within the state. This form plays a critical role in enabling taxpayers to reduce their state tax liability by supporting public education. The credit is available for both individual and joint filers and covers cash contributions made to support extracurricular activities or character education programs.

How to Use the Arizona Form 322

To effectively use Arizona Form 322, taxpayers must submit the form as part of their state tax return. It requires detailing the contributions made to qualifying school programs within the tax year. Steps for usage include identifying eligible contribution amounts, completing the necessary fields on the form, and attaching it to the Arizona state tax return. The accuracy of the information provided and adherence to filing deadlines are crucial to avoid processing delays or errors.

Steps to Complete the Arizona Form 322

-

Gather Contribution Information: Collect details of all contributions made to qualifying public schools, including receipt dates, school names, and amounts.

-

Complete Taxpayer Information: Enter your personal information, such as name, address, and Social Security number. For married couples filing jointly, include spouse information.

-

Enter Contribution Details: Fill in the contribution section with precise amounts and beneficiary school names.

-

Calculate Credit: Use the form's calculation section to determine the credit amount you're eligible to claim for the tax year.

-

Include Carryover Credit: If applicable, include any carryover credits from previous years in the designated section.

-

Review and Attach: Double-check all entries for accuracy, attach the completed form to your Arizona income tax return, and ensure all documentation is in order before submission.

Eligibility Criteria

Eligible individuals for Arizona Form 322 are those who have made financial contributions to public schools to fund extracurricular school-approved programs or activities. Eligibility extends to anyone paying Arizona state taxes, including those filing as single or married couples jointly. It's essential that contributions align with what the state categorizes as eligible donations, which most commonly include monetary gifts to school athletic programs, arts, and educational field trips.

Legal Use of the Arizona Form 322

Legally, Arizona Form 322 requires truthful reporting of contributions to receive a tax credit. The form is only valid for contributions made within the specified tax year and must reflect actual donations to approved schools and programs. It's illegal to claim credit for non-qualifying amounts or falsify any part of the form. Inaccurate information can lead to penalties or a rejection of the credit claim. Therefore, maintaining a detailed record of contributions and corresponding documentation is critical for legal compliance.

State-Specific Rules for the Arizona Form 322

Arizona state law specifies that for contributions to qualify for credit, they must be monetary (not goods or services) and directed to certified public schools, focusing on extracurricular activities. The rules also stipulate limitations on the credit amount depending on the taxpayer's filing status—for instance, limits are set per filing type (single versus married). Changes in the enacted budget or tax legislation can influence credit caps or qualifying criteria, necessitating taxpayers to check for annual updates from the Arizona Department of Revenue.

Examples of Using the Arizona Form 322

Consider a taxpayer, Jane, who donated $400 to her son's public school to support the band program. Jane can use Arizona Form 322 to claim a credit for this donation, directly reducing her state tax liability by this amount, provided it does not exceed her allowed credit limit. For a married couple, John and Mary, who contributed $800 collectively to their children's schools, they may claim this amount on their joint tax return, again mindful of their eligible credit ceiling.

Filing Deadlines / Important Dates

The filing deadline for Arizona Form 322 aligns with the state income tax return dates, typically due by April 15th, unless extensions apply. Contributions should be made before December 31 of the tax year to qualify. Taxpayers are encouraged to submit the form along with their state tax return by the due date to avoid penalties or a forfeiture of the credit. Any revisions to deadlines, generally resulting from legislative changes, are communicated by the Arizona Department of Revenue.

Penalties for Non-Compliance

Failure to accurately complete and file Arizona Form 322 can result in penalties, including the disallowance of the tax credit. In instances of negligent reporting or fraudulent claims, taxpayers could face additional fines or interest charges on their tax liability. Compliance with form instructions and state guidelines is imperative to avoid these ramifications and ensure a smooth credit claiming process.