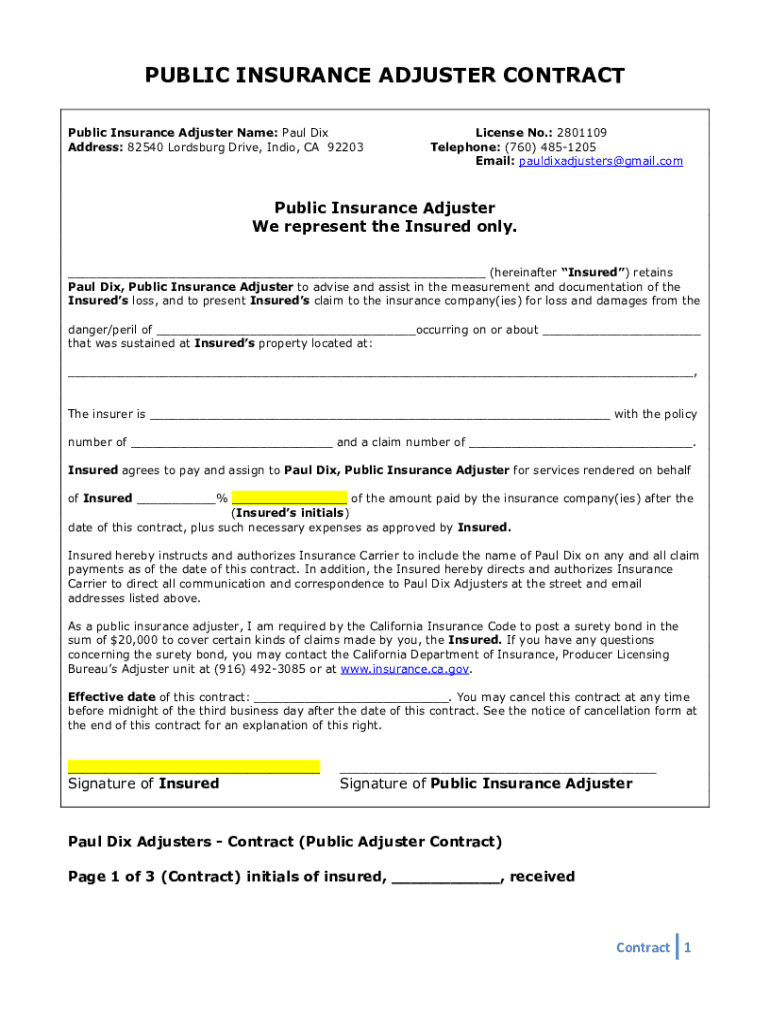

Definition and Purpose of the Public Insurance Adjuster Contract

The k3claims Public Insurance Adjuster Contract is a formal agreement between the insured party and a licensed public insurance adjuster. This contract outlines the terms and conditions under which the adjuster will represent the insured in filing an insurance claim. It specifies the responsibilities of the adjuster, including negotiating and advocating on behalf of the insured to ensure they receive a fair settlement. This contract ensures that the adjuster works exclusively for the insured, safeguarding their rights and interests during the claims process.

Key Responsibilities of the Public Insurance Adjuster

-

Assessment and Documentation: The adjuster is responsible for assessing the damage and documenting all necessary details to support the claim.

-

Claim Negotiation: They negotiate with the insurance company to secure a favorable outcome for the insured.

-

Settlement Advice: The adjuster provides guidance on the settlement amount, ensuring it meets the insured's expectations and needs.

-

Process Management: They manage all administrative tasks related to filing and following up on the claim, relieving the insured of this burden.

Steps to Complete the Public Insurance Adjuster Contract

-

Review and Understand Terms: Carefully read through the contract to understand the scope of services, fees, and obligations.

-

Provide Required Information: Fill out personal details and any relevant information about the insurance policy and claim.

-

Agree to Fee Structure: Acknowledge the adjuster's fee, typically a percentage of the claim settlement, and confirm understanding.

-

Sign the Contract: Once all sections are completed and understood, sign the document to formalize the agreement.

-

Keep a Copy: Retain a copy of the signed contract for personal records and future reference.

Important Considerations

-

Cancellation Options: Contract stipulates cancellation rights, allowing insured to rescind the agreement within three business days without penalty.

-

Confidentiality Clauses: Ensure that personal information and claim details are kept confidential by the adjuster.

Legal Use of the Public Insurance Adjuster Contract

The contract is designed to comply with legal standards, ensuring that the insured is legally protected during the claim process. It aligns with regulations that govern public insurance adjusters in the U.S., such as maintaining transparency in fees and services. The contract is structured to avoid conflicts of interest, emphasizing the adjuster's role in solely representing the insured's best interests.

Compliance and Regulations

-

State Licensing Requirements: Public insurance adjusters must be licensed in the state where the claim is filed, adhering to specific state regulations.

-

Ethical Standards: Adjusters are obligated to follow ethical guidelines, ensuring fair and honest representation of the insured.

Key Elements of the Public Insurance Adjuster Contract

The contract consists of several critical components that outline the agreement's framework:

-

Parties Involved: Clearly names the insured and the public insurance adjuster, establishing the contractual relationship.

-

Scope of Services: Details the specific duties the adjuster will perform, including filing, negotiating, and finalizing claims.

-

Payment Terms: Outlines the fee structure based on a percentage of the final settlement, with no upfront fees required.

-

Cancellation Policy: Provides the insured with a three-day period to cancel the contract without any financial obligation.

Who Typically Uses the Public Insurance Adjuster Contract

This contract is commonly used by homeowners, business owners, and individuals who have experienced a loss and need professional assistance in managing and negotiating their insurance claims. It is particularly beneficial for:

-

Homeowners: Experiencing property damage due to events like fire, flood, or theft.

-

Business Owners: Managing complex claims related to business interruption or substantial property loss.

-

Policyholders: Lacking the time or expertise to handle detailed negotiations with their insurance provider.

State-Specific Rules for Public Insurance Adjuster Contracts

Each state in the U.S. may have unique regulations governing the execution and terms of public insurance adjuster contracts. These variations can affect the following areas:

-

Contract Cancellation Periods: Some states might extend or reduce the cancellation window.

-

Fee Structures: Maximum allowable fees may be capped by state law.

-

Disclosure Requirements: States can mandate specific disclosures that adjusters must provide to insured parties.

Notable State Differences

-

California: Requires additional disclosures related to the insured's rights.

-

Florida: Regulates the percentage cap on adjuster fees more strictly.

Penalties for Non-Compliance with Public Insurance Adjuster Contracts

Failure to adhere to the terms of a public insurance adjuster contract can lead to several penalties, including:

-

Loss of Licensure: Adjusters may lose their license to operate if found violating state regulations.

-

Legal Consequences: Breach of contract could result in lawsuits or fines for either party.

-

Claim Disputes: Non-compliance can lead to disputed claims, delaying the settlement process and potentially reducing payout amounts.

Examples of Non-Compliance

-

Unauthorized Fee Changes: Adjusters altering their fee structure without consent from the insured.

-

Incomplete Scope of Services: Failing to provide the agreed-upon services as outlined in the contract.

Form Variants and Alternatives to the Public Insurance Adjuster Contract

While the k3claims Public Insurance Adjuster Contract is a standardized document, variations can exist based on individual adjuster practices or specific insurance needs. Alternatives and related documents include:

-

Custom Contracts: Some adjusters may offer tailored contracts specific to unique client situations.

-

Alternate Forms: Other industry-standard templates might be used depending on the insurer or adjuster preferences.

Choosing the Right Form

-

Assess Needs: Determine whether a standard or customized form best suits the claim situation.

-

Consultation: Engage with the adjuster to understand available options and pick the most effective contract type.