Definition & Meaning

The CM-2 (Rev 2024), Statement of Financial Condition and Other Information, is a document used primarily in the State of Hawaii for individuals to report their financial status to the Department of Taxation. This form requires a comprehensive declaration of one's financial situation, including assets, liabilities, income, and expenses. The purpose of this form is to provide the department with a detailed picture of the taxpayer's financial condition, helping to ensure accurate tax assessments and compliance with state tax laws.

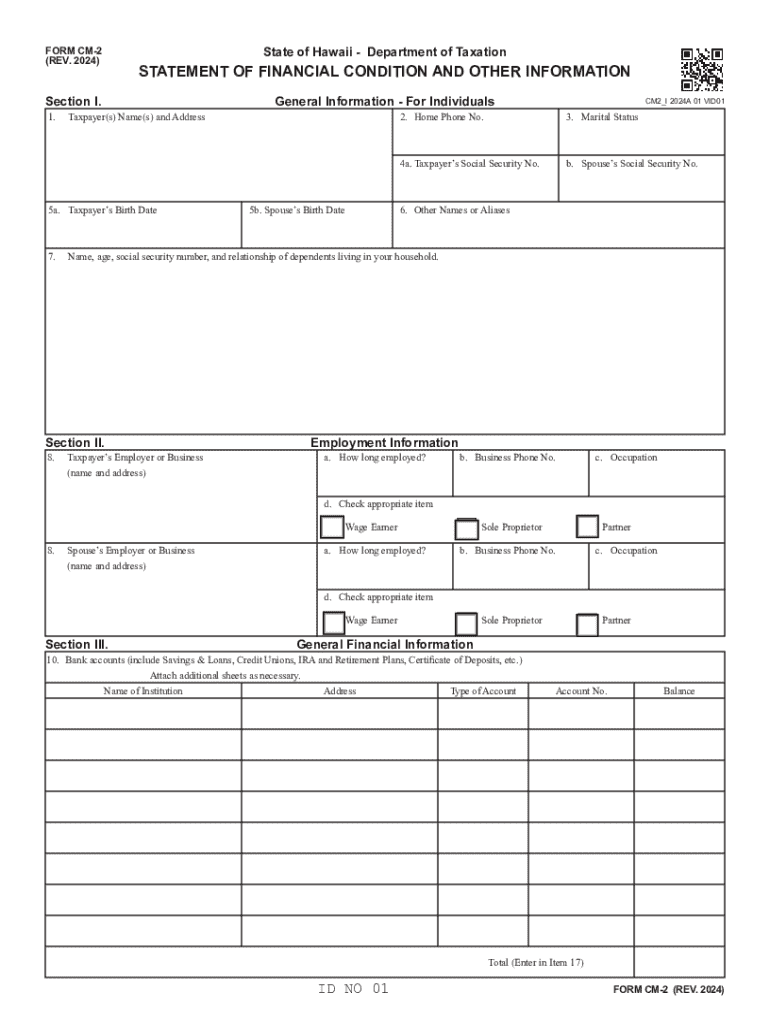

Key Elements of the CM-2 (Rev 2024)

The CM-2 form comprises several key sections that organize the financial data of the individual. These sections include:

- Personal Information: Requires basic identity data such as name, address, and Social Security number.

- Employment Details: Requires the taxpayer's current employment information, including employer name and job title.

- Assets Declaration: Lists all owned assets, including cash, investments, real estate, and personal property.

- Liabilities Section: Captures the total liabilities such as loans, credit card debts, and mortgages.

- Income and Expense Analysis: Details monthly or annual income sources and typical monthly expenses.

- Certification Section: Requires the taxpayer's signature to authenticate the information provided.

Steps to Complete the CM-2 (Rev 2024)

- Gather Necessary Documents: Collect financial documents, such as bank statements, pay stubs, and loan records.

- Enter Personal and Employment Information: Fill in the personal and employment details section using precise and updated data.

- List Assets and Liabilities: Provide an accurate account of all assets and liabilities. Ensure all figures are up-to-date.

- Detail Income and Expenses: Calculate and enter average monthly income and expenses for accuracy.

- Review and Certify: Double-check all entries for accuracy, sign the form in the certification section, then prepare for submission.

Eligibility Criteria

Individuals required to file the CM-2 form often include those with complex financial situations or significant changes in their financial status. These criteria can vary, but typically involve:

- Changes in income levels

- New significant assets acquisition

- Large financial liabilities incurred

- Changes in employment status

- Those involved in state tax disputes or audits

Required Documents

Completing the CM-2 form necessitates various supporting documents to validate the provided information:

- Copies of recent pay stubs or employment contracts

- Bank statements showing current account balances

- Loan and mortgage documentation

- Records of any investment or property ownership

- Current bills to verify expense claims

State-specific Rules for the CM-2 (Rev 2024)

The CM-2 form is specifically used within the jurisdiction of Hawaii and reflects the state's tax policies. Key points include:

- Guidelines align with the Hawaii Department of Taxation's requirements, different from other states.

- Detailed financial disclosure is emphasized to support fair tax assessments.

- Variations in reporting methods and document requirements may apply compared to similar forms in other states.

How to Obtain the CM-2 (Rev 2024)

The CM-2 form can be acquired through several avenues:

- Online Download: Available on the Hawaii Department of Taxation's official website for direct download.

- Mail Request: Can be requested via mail by contacting the department and specifying the need for the CM-2 form.

- Tax Offices: Physical copies can be picked up at local tax offices within Hawaii.

Form Submission Methods

Taxpayers have multiple options for submitting the completed CM-2 form:

- Online Submission: Can often be filed directly through the state's official tax website.

- Mail: Physical copies of the completed form can be sent via postal service to the designated mailing address.

- In-Person: Completed forms can be submitted at local tax offices for those preferring direct interaction with tax officials.

Penalties for Non-Compliance

Failing to file the CM-2 form accurately or timely can result in several penalties:

- Potential fines or interest charges on any outstanding tax amounts

- Legal complications or audits by the state's tax department

- Reputational risks with future financial and tax dealings in Hawaii