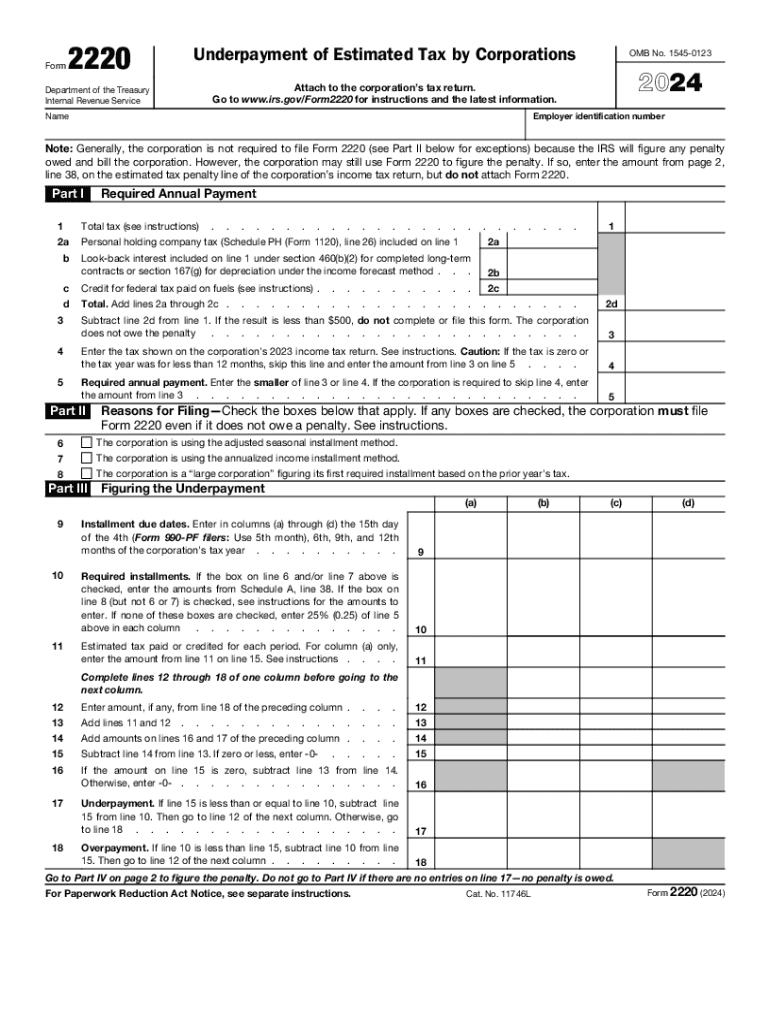

Definition and Purpose of 2024 Form 2220

The 2024 Form 2220, Underpayment of Estimated Tax by Corporations, serves as a critical document for corporations needing to report any underpayment of estimated taxes to the Internal Revenue Service (IRS). This form is primarily used to figure out if a corporation might owe a penalty for underpaying estimated taxes throughout the tax year. Under federal tax regulations, corporations are required to make estimated tax payments if their anticipated tax liability is expected to be $500 or more. The form allows corporations to calculate the total tax owed, assess whether any penalties apply due to underpayment, and determine the underpayment amount over each quarter.

How to Use the 2024 Form 2220

Corporations must carefully follow several steps to utilize the 2024 Form 2220 effectively. Firstly, gather all relevant financial data to ascertain the total estimated tax due for the fiscal year. Corporations will then need to document all estimated tax payments made during the year. The form outlines a detailed calculation method to compare the required annual payment amount with the actual payments made. If this assessment reveals an underpayment, the form provides sections to compute the penalty owed based on IRS guidelines.

Steps to Complete the Form

- Gather Required Documents: Collect all tax payment records and financial statements.

- Calculate Required Annual Payment: Determine the lesser of 100% of prior year's tax liability or 100% of the current year's estimated tax liability.

- Record Quarterly Estimated Payments: List all payments made in the appropriate sections.

- Compute Underpayment: Use the form to figure discrepancies between required payments and actual payments.

- Calculate Penalty: Follow specified steps to determine any penalty using IRS risk factors and scenarios.

- Submit the Form: Ensure all details are accurate before completing submission through the preferred method.

Who Uses the 2024 Form 2220

Typically, medium to large corporations within the United States use the 2024 Form 2220. These corporations are ones that generally anticipate a tax liability of $500 or more. While smaller entities like LLCs or partnerships might utilize other forms or filing methods, the Form 2220 is essential for larger entities that need to consistently monitor their tax obligations throughout the year.

Important Terms and Concepts

- Estimated Taxes: Quarterly tax payments made based on projected annual tax liability.

- Underpayment: The difference between required and actual tax payments made in the fiscal year.

- Penalty: A fine calculated when there is a deficit in estimated tax payments.

Understanding these terms ensures that corporations can accurately complete their filings and comply with IRS expectations.

IRS Guidelines and Penalties

The IRS stipulates that corporations must make accurate estimated tax payments to avoid penalties. The agency provides specific guidance on assessing underpayments and calculating corresponding penalties via percentage rates applied to underpayments for each under-fulfilled quarter. If a corporation fails to file or files incorrectly, the IRS retains the authority to impose significant financial penalties.

Filing Deadlines and Important Dates

The IRS mandates that corporations make their estimated tax payments quarterly. These deadlines typically fall on the 15th day of April, June, September, and the following January. However, when these dates coincide with a holiday or weekend, the deadline is extended to the next business day. Adherence to these deadlines is critical to avoid potential penalties.

Submission Methods and Software Compatibility

Corporations can submit their 2024 Form 2220 via traditional mailing methods or through electronic submissions on IRS-approved e-filing platforms. Platforms such as TurboTax and QuickBooks can assist in managing the calculation and submission processes. E-filing is recommended for its security and timeline efficiency.

Eligibility Criteria and Business Types

Eligibility to use the 2024 Form 2220 primarily encompasses corporate entities like C Corporations and, occasionally, S Corporations that expect a total tax liability exceeding $500. While smaller entities might not need this form, businesses with complex, varied revenue streams rely on it to ensure compliance with federal tax policies.