Definition and Meaning

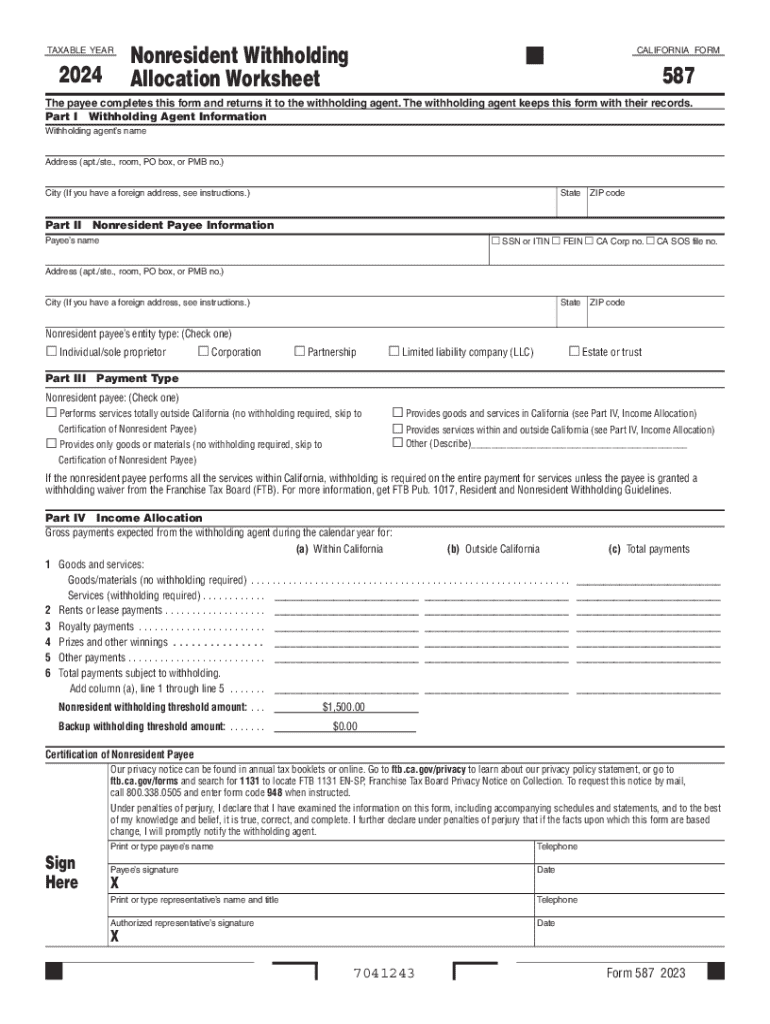

The 2024 Form 587, officially known as the Nonresident Withholding Allocation Worksheet, is a critical document used in California for nonresident payees to report their income and withholding requirements to the withholding agent. This form specifies the taxable income for nonresidents and the necessary withholding, based on services performed within California. The precise identification and allocation of nonresident income and related withholding are essential to comply with the state's tax regulations, avoiding any potential legal complications.

Steps to Complete the 2024 Form 587

-

Gather Required Information:

- Collect personal details such as full legal name, address, and taxpayer identification number.

- Ensure you have information on the withholding agent, like their name, address, and withholding identification number.

-

Fill Out Payment Information:

- Specify the type of payment involved, like wages, services, or royalties.

- Indicate payment dates and amounts applicable for withholding purposes.

-

Income Allocation:

- Accurately allocate the income related to work performed in California.

- Calculate the portion subject to withholding based on residency status and nature of work.

-

Records of Certification:

- Accuracy certification is a crucial part, as non-compliance can lead to penalties.

- Certify under penalty of perjury that the information provided is correct and complete.

-

Review and Submit:

- Double-check all entries for completeness and precision.

- Submit the form to the withholding agent, keeping a copy for personal records.

Who Typically Uses the 2024 Form 587

-

Nonresident Individuals and Contractors:

- Individuals performing temporary or freelance work within California but reside elsewhere use this form to allocate income properly.

-

Out-of-State Business Entities:

- Businesses operating in California without physical locations may need this form to declare income derived from Californian sources.

-

Entertainers and Athletes:

- Professionals attending events or performing gigs in California must regulate their earnings and corresponding state tax obligations through this form.

Key Elements of the 2024 Form 587

-

Withholding Agent and Payee Information:

- This section captures essential details such as names and IDs which serve as identifiers for taxation purposes.

-

Payment Type Specification:

- Understanding how the nature of the income (e.g., wages vs royalties) affects withholding is critical for accurate reporting.

-

Income Allocation Breakdown:

- An itemized list of work or services attributed to California helps in determining the withholding amount needed.

Legal Use of the 2024 Form 587

The form serves to ensure compliance with California's tax laws, reflecting income accurately and determining the relevant withholding for nonresident services. Filing this form hinders tax evasion by documenting taxable income accurately, maintaining legal standing with the state's taxation authority.

State-Specific Rules for the 2024 Form 587

-

Service Location Impact:

- California law demands withholding not just based on residency but the location of actual service delivery.

-

Nonresident Status Verification:

- Filing may require proof of nonresident status to ascertain valid exclusion from California's general tax provisions.

Required Documents

-

Identification Proof:

- Usually a government-issued ID is necessary to validate person or entity claims.

-

Transaction Records:

- Contracts, invoices, or receipts confirming the nature and amount of payment.

-

Proof of Service:

- Evidence of work conducted within California, such as itineraries or contracts demonstrating business operations.

Penalties for Non-Compliance

Failure to file or inaccurately completing the 2024 Form 587 may result in penalties, including fines or increased withholding obligations. Non-compliance could compound classed as felony charges under certain circumstances, posing serious legal ramifications for both payees and withholding agents. Regular consultations with tax specialists or legal advisors can mitigate the risk of penalties while ensuring compliance.