Definition & Meaning

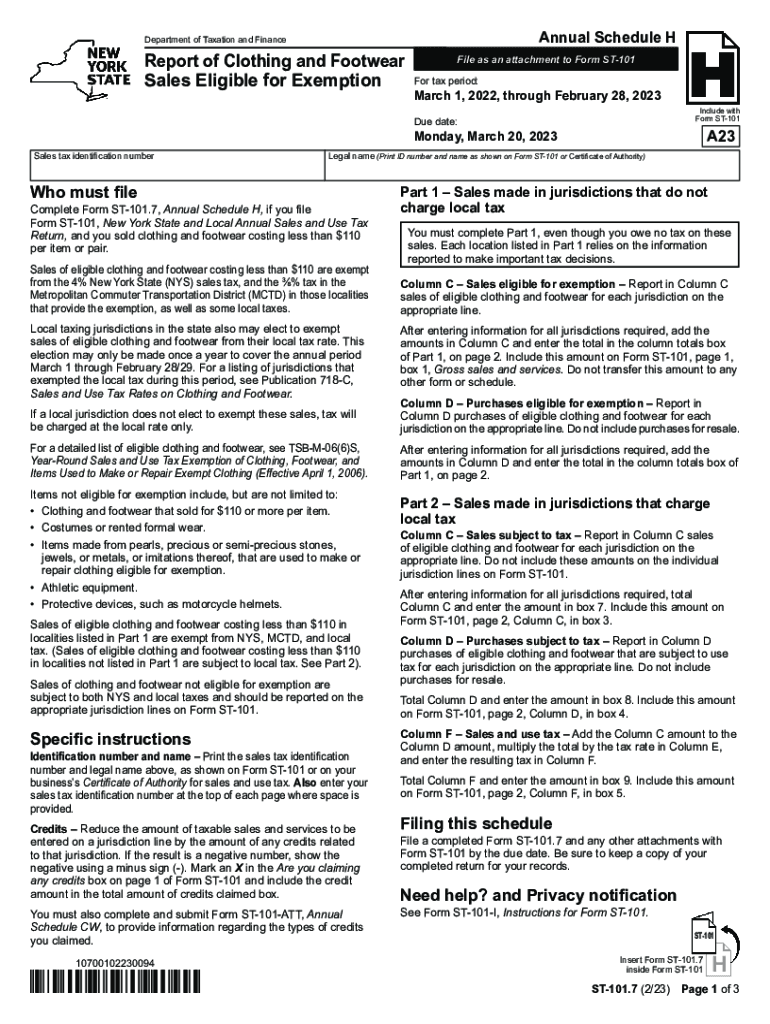

The Form ST-101.7, also known as the Report of Clothing and Footwear Sales, is an official document required by the New York State Department of Taxation and Finance. This form is specifically designed for reporting sales transactions of clothing and footwear that qualify for a tax exemption. These items must be priced under $110 to be eligible for this exemption, and the form helps businesses accurately report and itemize these sales for tax purposes. Understanding whether an item falls within these guidelines is crucial for compliance.

How to Use the Form ST-101.7 Report of Clothing and Footwear Sales

To effectively use Form ST-101.7, retailers need to accurately track the sales of qualifying items throughout the tax period. This involves documenting each sale that is eligible for the exemption, ensuring all transactions are correctly categorized. Retailers must report total sales amounts and the corresponding tax-exempt sales to ensure compliance with state regulations. Retailers should use consistent and thorough record-keeping practices to prevent discrepancies when submitting this form.

Steps to Complete the Form ST-101.7 Report of Clothing and Footwear Sales

- Collect Necessary Information: Gather records of all clothing and footwear sales eligible for tax exemption.

- Enter Sales Data: Record individual sales that meet the exemption criteria on the form, ensuring accuracy in the transaction details.

- Calculate Totals: Sum the exempt and non-exempt sales figures, verifying all calculations align with your records.

- Review Requirements: Double-check local tax regulations to ensure all sales are compliant and correctly reported.

- Submit the Form: File the form alongside Form ST-101 within the specified deadlines to avoid penalties.

Legal Use of the Form ST-101.7 Report of Clothing and Footwear Sales

Legally, the submission of Form ST-101.7 ensures compliance with the state's tax laws, particularly regarding sales tax exemption for certain clothing and footwear items. Accurate reporting is essential to avoid legal repercussions, such as fines or audits. Businesses must be aware of potential changes in legislation regarding exemptions and ensure all reported items meet the specified criteria.

Important Terms Related to Form ST-101.7

- Tax Exemption: This refers to the allowance of certain sales to be excluded from sales tax due to qualifying criteria, such as price thresholds.

- Qualifying Items: In the context of this form, qualifying items refer to clothing and footwear priced below $110.

- Sales Documentation: Maintaining thorough sales records, including receipts and transaction logs, is vital to support data reported on the form.

Penalties for Non-Compliance

Failing to properly report sales through Form ST-101.7 can lead to significant penalties. These may include financial fines, interest on overdue taxes, and potential audits by the tax authorities. Businesses need to ensure completeness and accuracy in filing to avoid these penalties.

Filing Deadlines / Important Dates

Form ST-101.7 should be filed in conjunction with Form ST-101 by the deadlines set forth by the New York State Department of Taxation and Finance. The filing period typically covers sales from March 1st to February 28th of the following year, with specific submission deadlines announced annually. It is essential for businesses to monitor these deadlines closely.

Examples of Using the Form ST-101.7

An example scenario involves a clothing retail store in New York City. Throughout the year, the store records the sale of various clothing items priced below $110. At the end of the tax period, the store compiles these sales and reports them using Form ST-101.7 to ensure they are accurately reflected as exempt sales. This practice safeguards the store from penalties and ensures compliance with state regulations.

Business Types That Benefit Most from Form ST-101.7

Retail businesses that specialize in selling clothing and footwear are the primary users of Form ST-101.7. These include brick-and-mortar stores, online retailers, and department stores. By filing this form accurately, these businesses can take advantage of tax exemptions, enhancing their economic advantage and simplifying compliance with state tax laws.

Who Issues the Form

The New York State Department of Taxation and Finance issues Form ST-101.7. This agency is responsible for creating guidelines and ensuring retailers comply with tax laws related to exempt sales of clothing and footwear.

State-Specific Rules for the Form ST-101.7 Report of Clothing and Footwear Sales

New York's tax laws uniquely define the qualifications for tax exemption using this form. It is important to distinguish between state, local, and special district tax rules, as some areas may have additional requirements or exemptions beyond the state-level guidelines. Understanding these intricacies is vital for businesses operating in multiple jurisdictions within New York.