hud addendum

TECHNICAL LITERATURE

Addendum to Broad Band Linear Power Amplifiers using push-pull Transistors Information is presented in the form of Application Notes and ArticleRead more

Learn more

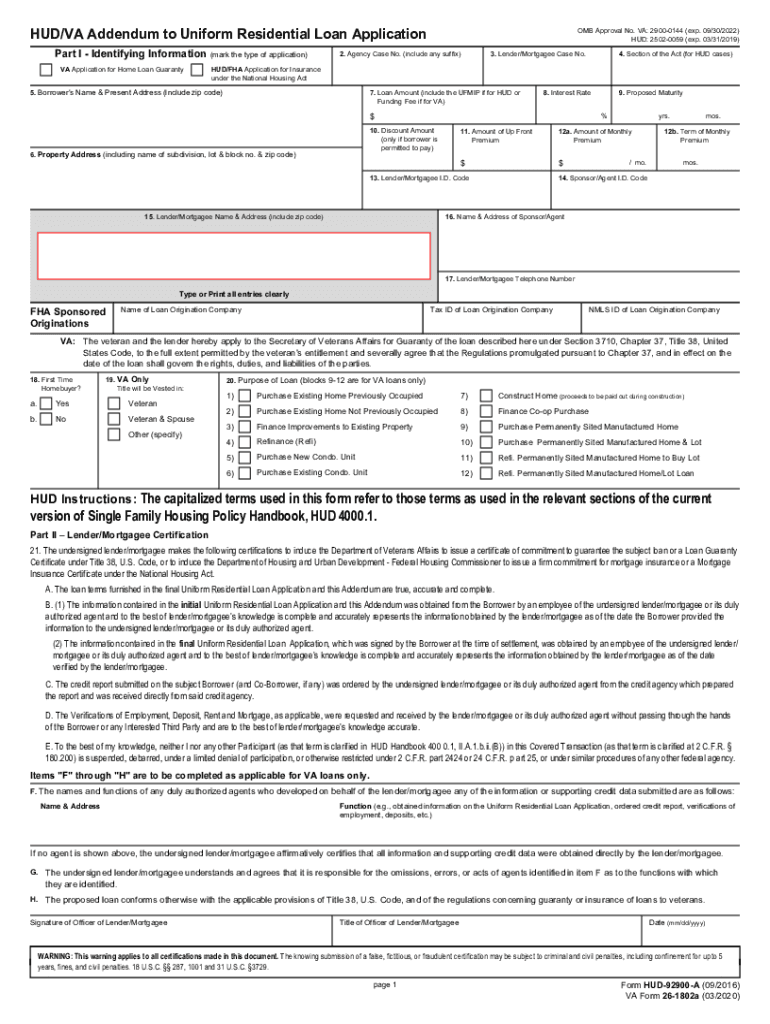

HUD/VA Addendum to Uniform Residential Loan Application

The loan terms furnished in the Uniform Residential Loan Application and this Addendum are true, accurate and complete. VA Form 26-1802a.Read more

Learn more

Vermont Technical College

Please visit the GI Bill website and complete the VA form that applies: 22-1990 if you have served in the military and are applying for educationRead more

Learn more