Definition and Meaning

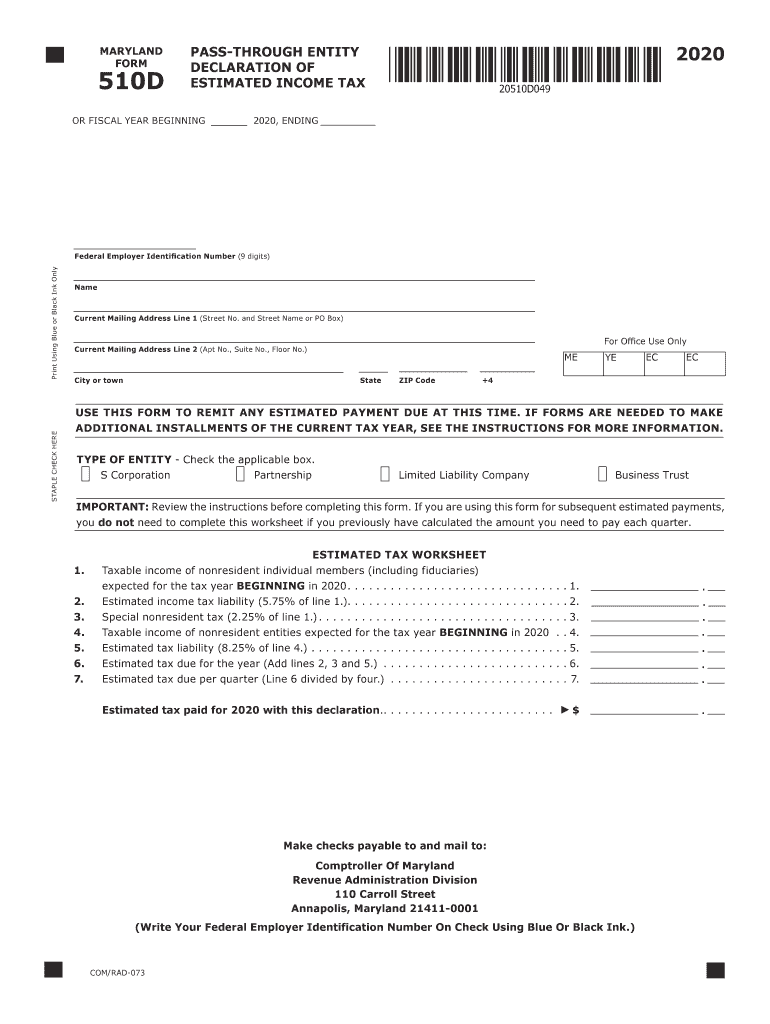

The TY-2020-510D PTE Estimated Income Tax Form is crucial for pass-through entities (PTEs) operating in Maryland. These entities use the form to declare and remit estimated income tax payments on behalf of their nonresident members. The form is specifically designed to ensure that income derived from sources within Maryland is appropriately taxed, according to state laws. This requirement aligns with the state's aim to capture taxes from income earned within its jurisdictions by nonresident entities.

Key Features:

- Pass-Through Entity Focus: This form applies specifically to PTEs, which may include partnerships and S corporations.

- Nonresident Member Component: Aimed at capturing tax contributions from nonresident stakeholders.

- Maryland Source Income: Pertains to income generated within the state's geographical boundaries.

Steps to Complete the TY-2020-510D PTE Estimated Income Tax Form

Completing the TY-2020-510D involves a structured process to ensure accuracy and compliance. Here’s a step-by-step guide:

-

Gather Necessary Information:

- Collect financial data for your PTE, including income statements and balance sheets.

- Have details about your nonresident members and their respective shares of income ready.

-

Calculate Estimated Tax Liabilities:

- Utilize the included worksheet to determine estimated taxes based on projected income and applicable state tax rates.

- Make adjustments for any prior year overpayments, if applicable.

-

Fill Out the Form:

- Enter calculated amounts in the specified sections for each nonresident member.

- Double-check entries to avoid discrepancies.

-

Review and Verify:

- Ensure all information aligns with business records and intended fiscal projections.

- Consult with a tax professional if needed for complex situations or large entities.

-

Submit the Form:

- Choose an appropriate submission method (online, mail, or in-person) that fits your preference and timeline.

Examples:

- Scenario: A small LLC with three nonresident partners calculates its estimated income tax based on projected income of $500,000. Using the worksheet, they determine proportional payments required by each partner.

- Case Study: An S corporation reviews previous filings and notes an overpayment which they apply as a credit to their estimated taxes for TY-2020.

Filing Deadlines and Important Dates

Understanding the timeline for filing the TY-2020-510D is essential for avoiding penalties:

-

Quarterly Payments: Typically required in four installments throughout the fiscal year.

- April 15: First payment due for the calendar year.

- June 15: Second installment ensures ongoing compliance.

- September 15: Third payment aligns with end-of-summer assessments.

- January 15: Final payment wraps up the fiscal obligations.

-

Extensions: While Maryland does not automatically grant extensions specific to the TY-2020-510D, aligning federal extension requests with state provisions can provide additional time if necessary.

Considerations:

- Noncompliance Penalties: Late payments or filings can result in fines; timely filing is critical.

Key Elements of the TY-2020-510D PTE Estimated Income Tax Form

A thorough understanding of the form’s core components will facilitate accurate completion:

- Details of Nonresident Members: Required to ensure accurate record-keeping and tax responsibility delineation.

- Income Declaration: Segregating Maryland-sourced income from other revenue streams.

- Payment Calculations: Aligning estimated taxes with anticipated earnings.

- State-Specific Instructions: Guidance for PTEs with unique operational structures or income scenarios.

Example:

- A partnership operating in several states allocates income proportionately, ensuring Maryland-sourced revenue is emphasized in the TY-2020-510D.

Important Terms Related to the TY-2020-510D PTE Estimated Income Tax Form

Familiarity with the following terms is critical when navigating the TY-2020-510D:

- Pass-Through Entity (PTE): Business structure where income is passed directly to owners, bypassing corporate tax obligations.

- Nonresident Member: Stakeholder residing outside the jurisdiction where income is earned.

- Estimated Tax: Projections of tax liabilities based on anticipated earnings, paid periodically.

- Taxable Year: Period over which tax obligations are calculated, often aligning with the calendar year.

Form Submission Methods

Efficiency in submission can impact timeliness and record-keeping. The TY-2020-510D offers multiple channels:

Online Submission:

- Efficient and immediate, enabling electronic payments and record generation.

- Utilize DOCHub or official Maryland tax portals for optimal results.

Mail:

- Traditional method for entities preferring paper records.

- Ensure timely delivery by confirming postal deadlines are met.

In-Person:

- Suitable for complex filings requiring personal interaction.

- Ensure appointment or visiting hours align with submission timelines.

Penalties for Non-Compliance

Avoiding penalties starts with understanding the consequences of non-compliance:

- Late Payment Fees: Imposed when payments are delayed beyond due dates.

- Underpayment Charges: Applied when estimated taxes significantly deviate from actual liabilities.

Example:

- An S corporation was fined for a significant shortfall in their third-quarter estimate, learning that accurate projections are critical for cost minimization.

Who Typically Uses the TY-2020-510D PTE Estimated Income Tax Form

Identifying appropriate users ensures the form serves its intended purpose:

- Limited Liability Companies (LLCs): Especially those with income originating entirely or partially in Maryland.

- S Corporations: When corporate structures include nonresident stakeholders.

- Family Partnerships: Utilizing the form to maintain compliance with state taxation guidelines on collectively owned assets.

Practical Insight:

- A real estate partnership, with diverse asset holdings in multiple states, annually refines their tax approach using the TY-2020-510D, ensuring comprehensive compliance with Maryland’s taxation laws.