Definition & Understanding of Form 12N

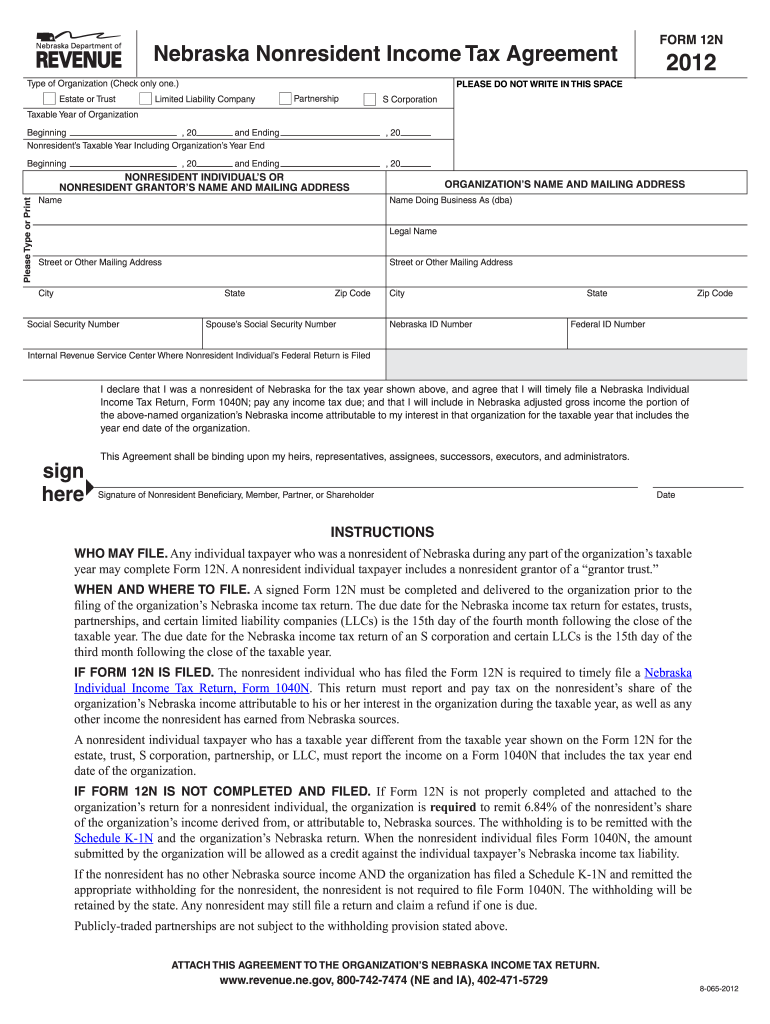

Form 12N, officially referred to as the "2012 Nebraska Nonresident Income Tax Agreement," is a crucial tax form for nonresident individuals, including grantors of trusts, who need to report their share of income from Nebraska-based organizations. This form outlines specific filing requirements, ensuring compliance with Nebraska state tax regulations. Understanding the purpose and function of Form 12N is essential for those needing to report income sourced from Nebraska, especially if they reside and primarily operate from other states.

Key Aspects of the Form

- Purpose: Allows nonresidents to report Nebraska-sourced income.

- Target Users: Nonresident individuals and grantors of trusts.

- Importance: Ensures legal compliance with Nebraska tax laws by facilitating proper reporting.

How to Use the Form 12N

Utilizing Form 12N involves several steps to accurately report income. The form is designed for nonresident individuals and requires detailed information regarding income earned from Nebraska-based activities.

Detailed Steps for Usage

- Gather Necessary Information: Collect all required documents detailing income from Nebraska sources.

- Complete Form Fields: Fill in personal details and income information precisely as instructed.

- Review Filing Requirements: Ensure all necessary sections of the form are completed, especially those relevant to income tax calculation.

Real-World Example

- A nonresident business consultant earning through Nebraska contracts must use Form 12N to report their income.

Steps to Complete the Form 12N

Completing Form 12N involves following a sequence of detailed instructions to ensure all necessary information is accurately recorded.

Step-by-Step Completion Process

- Personal Information Entry: Provide basic details such as name, address, and social security number.

- Income Reporting: Enter precise income figures derived from Nebraska-based activities.

- Deductions and Credits: Apply eligible deductions or credits applicable to nonresidents.

- Final Review and Submission: Double-check for accuracy before submitting either online or via mail.

Important Tips

- Consult a tax professional for complex income scenarios.

- Use past Nebraska tax returns as references to avoid discrepancies.

Who Typically Uses the Form 12N

The primary users of Form 12N are nonresident individuals who derive income from Nebraska-based enterprises.

Common User Scenarios

- Freelancers and Consultants: Those offering services to Nebraska companies.

- Remote Workers: Employees telecommuting for a Nebraska-based employer.

- Trust Grantors: Individuals managing trusts with income sourced from Nebraska.

Case Study

- A freelance web developer living in Iowa but creating websites for Nebraska firms would require Form 12N to declare their income.

Important Terms Related to Form 12N

Understanding the terminology associated with Form 12N is essential for accurate completion.

Glossary of Key Terms

- Nonresident: An individual residing outside Nebraska with Nebraska income.

- Trust Grantor: A person who establishes a trust receiving Nebraska income.

- Income Source: The origin of income, necessitating state tax reporting.

Further Clarification

- Withholding Taxes: Taxes withheld at the source for Nebraska, which may need adjustment on Form 12N.

Legal Use of the Form 12N

Form 12N serves a legally binding role in the reporting of nonresident Nebraska income taxes.

Legal Implications

- Compliance: Ensures adherence to Nebraska state taxation laws.

- Tax Liability Management: Helps nonresidents calculate and manage their Nebraska tax obligations to avoid penalties.

Critical Considerations

- Consult legal advisors to understand state-specific tax implications.

- Ensure accurate documentation to prevent future audits.

Filing Deadlines / Important Dates

Adhering to deadlines associated with Form 12N is crucial to ensure timely compliance and avoid penalties.

Key Filing Dates

- Annual Due Date: Typically aligns with federal tax return deadlines, often around mid-April.

- Extensions: May be available in specific circumstances; ensure requests are filed promptly to avoid late fees.

Example of Timeline Management

- A contractor receiving Nebraska payments should mark April 15 for filing Form 12N, along with their federal taxes, unless filing for an extension.

Penalties for Non-Compliance

Failure to comply with Form 12N filing requirements can result in significant penalties.

Consequences of Non-Compliance

- Monetary Fines: Late submissions or incorrect filings can lead to fines.

- Interest on Unpaid Taxes: Accrues on outstanding amounts until resolved.

Preventative Measures

- Ensure complete and accurate form submission before the deadline.

- Regularly update and verify all tax-related documents pertaining to Nebraska activities.

Form Variants and Alternatives

Various versions and related forms may apply depending on the specific circumstances of the taxpayer and the nature of their income.

Available Variants

- Older Versions: Use as historical reference if needed, ensuring the latest form is utilized for current filings.

Comparison with Alternatives

- Form 1040N: Used by individuals required to file a Nebraska Individual Income Tax Return, often in conjunction with Form 12N.

By understanding these comprehensive details of Form 12N, nonresidents can efficiently manage their Nebraska tax obligations.