Definition & Meaning

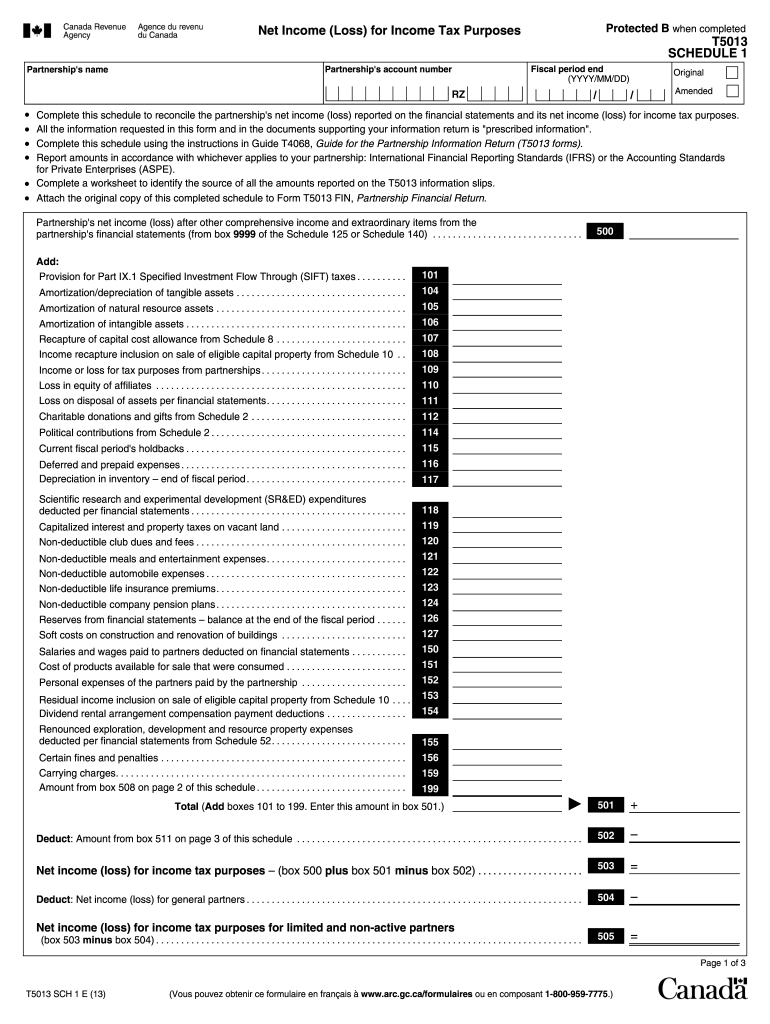

The 2013 Canada T5013 Schedule 1 E is a tax form used by partnerships in Canada to reconcile their net income or loss as reported on financial statements with the net income or loss for income tax purposes. It is necessary for ensuring accurate tax reporting and compliance with government regulations. This form is integral to the Canadian tax system, as it provides detailed instructions for completing the schedule, including various adjustments and deductions.

Key Elements of the Form

- Net Income Reconciliation: Assists partnerships in reconciling financial statement income with the tax return income.

- Adjustments & Deductions: Includes provisions for taxes, amortization, and non-deductible expenses.

- Partnership Financial Data: Requires specific financial data which must accompany the Partnership Financial Return.

How to Use the 2013 Canada T5013 SCH 1 E

The 2013 Canada T5013 Schedule 1 E is used by partnerships to ensure their financial statements align with the tax regulations set by the Canada Revenue Agency (CRA). To properly use this form:

- Gather Financial Statements: Ensure you have complete and accurate financial records for the fiscal year.

- Complete Adjustments: Reflect various adjustments and deductions not present in the financial statements.

- Submit Form Together: File this schedule along with the Partnership Financial Return to the CRA.

Practical Scenarios

- Amortization Adjustments: Adjust your recorded financial statements to meet CRA specifications on amortization.

- Non-Deductible Expenses: Account for items that may not be deductible for tax purposes but are present in financial statements.

Steps to Complete the 2013 Canada T5013 SCH 1 E

Filing the 2013 Canada T5013 Schedule 1 E involves distinct steps:

- Obtain the Form: Download the form from the CRA's website or obtain a physical copy.

- Gather Required Information: Assemble all financial records and other pertinent tax documents.

- Fill Out the Form: Enter financial data, make necessary adjustments, and calculate net income or loss.

- Submit the Form: File it along with the Partnership Financial Return by the specified deadline.

Common Challenges

- Understanding Tax Adjustments: Some partnerships may find it challenging to apply proper tax adjustments.

- Data Accuracy: Ensuring that the data on the form precisely reflects the financial statements.

Who Typically Uses the 2013 Canada T5013 SCH 1 E

Partnerships across Canada, ranging from small to large firms, use this form for tax filing purposes. This includes:

- Professional Service Firms: Legal, accounting, or consulting partnerships.

- Investment Partnerships: Those involved in managing pooled funds or financial assets.

- Agricultural Partnerships: Partnerships engaging in farming or agri-business operations.

Important Terms Related to the 2013 Canada T5013 SCH 1 E

- Net Income/Loss: The income remaining after expenses and other deductions.

- Amortization: The allocation of an asset's cost over its useful life.

- Non-Deductible Expenses: Costs not eligible to be subtracted from income for tax purposes.

Filing Deadlines / Important Dates

Partnerships must adhere to strict filing deadlines to avoid penalties:

- Filing Deadline: Generally, the form must be submitted within six months after the end of the partnership's fiscal year.

- Revisions: Any amendments to the submitted forms should be filed promptly.

Required Documents

Preparation and filing require several key documents:

- Financial Statements: The most recent annual financial statements.

- Previous Tax Returns: Any prior returns to ensure continuity and accuracy.

- Supplementary Documentation: Any papers supporting deductions or adjustments.

Form Submission Methods

The Canada T5013 Schedule 1 E can be submitted through various methods:

- Online Submission: Utilize the CRA's electronic filing system for a more efficient process.

- Mail-In: Traditional mail submission is an option, ensuring it is postmarked by the due date.

- In-Person: Submit directly at a CRA office if available.

Penalties for Non-Compliance

Failure to properly file the 2013 Canada T5013 Schedule 1 E can result in significant penalties:

- Late Filing Penalties: Applied for forms submitted past the deadline.

- Inaccurate Information: Penalties for providing incorrect financial data.

- Failure to Submit: Severe financial penalties can apply if the form is not submitted at all.

By following these structured guidelines and maintaining a comprehensive approach, partnerships can effectively navigate the complexities of the 2013 Canada T5013 Schedule 1 E.