Definition and Meaning

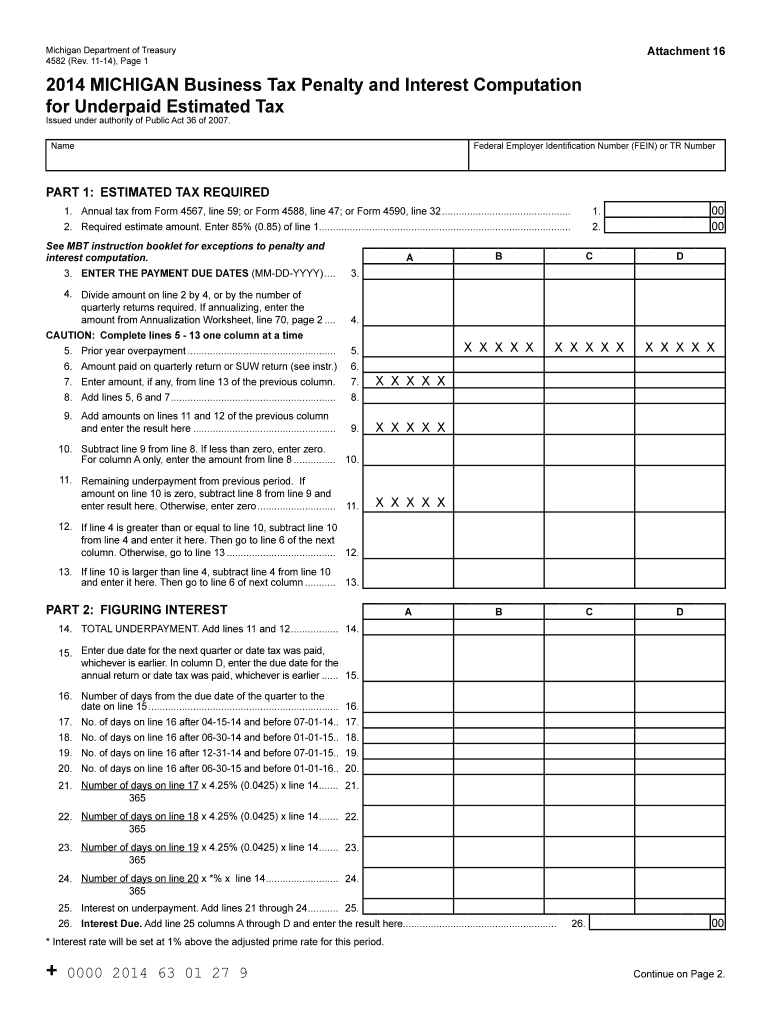

The MI-2210 penalty and interest pertain to the charges imposed by the State of Michigan on taxpayers who fail to pay their estimated taxes on time or in full. This penalty is part of the Michigan Business Tax (MBT) framework, which applies if individuals or businesses underpay their estimated tax liabilities throughout the year. The form helps taxpayers calculate and resolve these penalties and interests, ensuring compliance with Michigan's tax regulations. By understanding this form, taxpayers can properly assess their situations to avoid unnecessary fines.

Steps to Complete the MI-2210 Form

-

Gather Information: Begin by collecting all relevant financial documents, including income statements, previous tax returns, and proof of estimated tax payments.

-

Estimate Tax Obligations: Determine your estimated tax liability for the year. This includes all income sources, deductions, and credits applicable to your situation.

-

Calculate Underpayment: Compare your estimated taxes with what was actually paid during the year. Use the form’s specific sections to assess any underpayment amounts.

-

Compute Penalty and Interest: Follow the detailed instructions provided on the form to calculate any penalties and interest owed. These calculations consider the timing and total amount of underpayment.

-

Fill in the Form: Complete all required sections of the form based on your calculations. Ensure all entries are accurate to avoid further penalties.

-

Submit the Form: Submit the completed MI-2210 form through the appropriate channel, whether online, via mail, or in person, as instructed by Michigan’s Department of Treasury.

Key Elements of the MI-2210 Form

- Personal Information: Includes sections for taxpayer identification details, such as name, address, and Social Security or taxpayer identification number.

- Income Calculation: Details on how to compute total taxable income for the purpose of estimating taxes.

- Estimated Tax Payments: Sections to record quarterly estimated tax payments, including due dates and amounts.

- Underpayment Worksheet: Area designated for calculating discrepancies between estimated payments and actual liabilities.

- Penalty and Interest Computation: Detailed explanation of the formulas used to assess penalties based on both the amount and duration of underpayment.

IRS Guidelines and Important Dates

The Internal Revenue Service (IRS) provides general guidelines for the payment of estimated taxes, though state-specific rules apply for Michigan residents. It is crucial to adhere to IRS schedules while also considering:

- Estimated Tax Payment Deadlines: Typically due quarterly on April 15, June 15, September 15, and January 15 of the following year.

- Year-End Final Calculations: Complete the MI-2210 form soon after the tax year ends to ensure timely submission and avoid additional penalties.

Eligibility Criteria

Taxpayers, both individuals, and businesses, may be required to file the MI-2210 form if they:

- Owe more than $500 in Michigan taxes after credits and withholding.

- Paid less than 70% of the total tax liability through withholding or quarterly estimated payments.

- Receive income not subject to withholding.

Understanding these criteria helps determine whether completion of the MI-2210 form is necessary for your tax situation.

Examples of Using the MI-2210 Form

-

Example for Individuals: Jane, an independent contractor, receives inconsistent income throughout the year without tax withholding. She uses the MI-2210 form to calculate penalties on her underestimated tax payments.

-

Example for Businesses: A small LLC discovers an underpayment in its quarterly tax obligations due to fluctuating seasonal sales. The business uses the form to ascertain its penalty and interest charges.

Penalties for Non-Compliance

Non-compliance with estimated tax payment requirements can result in significant penalties. These include:

- Monetary Fines: Penalties based on the portion of tax underpaid and the length of delay in payment.

- Increased Interest Rates: Additional interest accrues on overdue amounts, potentially compounding the initial penalty.

Properly calculating and submitting the MI-2210 form helps mitigate these financial burdens.

State-Specific Rules for Michigan

Michigan imposes specific rules and penalties distinct from federal regulations. Key differences include:

- Penalty Rates: Michigan may apply different interest rates on underpayments compared to federal rates.

- State Income Discrepancies: Unique income formats and deductions applicable only under Michigan tax code must be considered.

Understanding these state-specific regulations is essential when addressing tax liabilities in Michigan.