Definition & Meaning

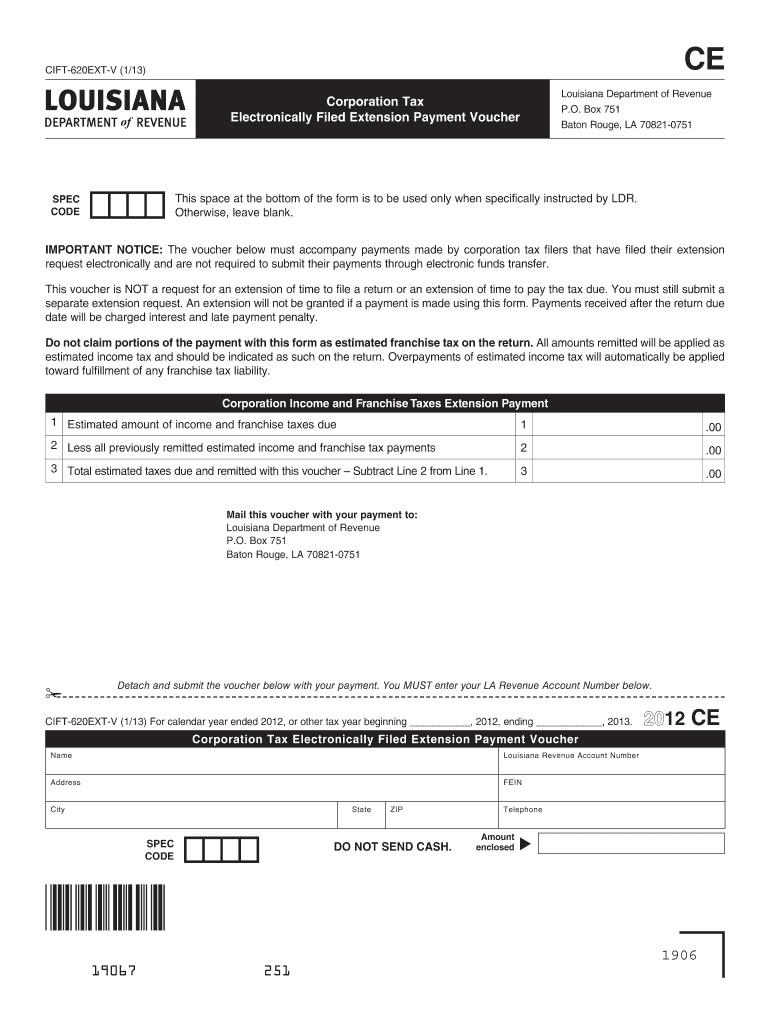

Form 620EXT for LA 2012 is a Corporation Tax Electronically Filed Extension Payment Voucher provided by the Louisiana Department of Revenue. It is specifically designed for corporations that have electronically filed a request for an extension to submit their corporate tax returns. This form facilitates the payment of estimated taxes, ensuring compliance with state tax obligations while allowing businesses additional time to complete and file their tax returns.

How to Use the Form 620EXT for LA 2012

To effectively use Form 620EXT for LA 2012, corporations must follow a series of steps to ensure correct and timely payment of estimated taxes. First, businesses should review their tax records to accurately calculate the estimated taxes owed. Afterward, the form should be completed with the required details, such as the corporation's name, Louisiana Revenue Account Number, and the total estimated tax payment. This voucher then accompanies the payment, submitted by mail or through approved electronic payment platforms.

Steps to Complete the Form 620EXT for LA 2012

- Gather Required Information: Collect the corporation’s essential details, including the Louisiana Revenue Account Number and current tax year data.

- Calculate Estimated Tax Payment: Use your financial records to estimate the amount due based on projected earnings and tax obligations for the specified year.

- Fill Out the Form: Enter all relevant data accurately, ensuring there are no errors in the corporation's identifying information or the calculated payment.

- Submit the Form: Choose a submission method. This may involve mailing the form along with a check to the Department of Revenue or completing the process through an approved electronic payment option.

Who Typically Uses the Form 620EXT for LA 2012

This form is primarily used by corporations operating within Louisiana that require an extension on filing their corporate income tax returns. It is particularly beneficial for businesses that need additional time to reconcile their financial records but still intend to adhere to their tax payment deadlines. Companies that anticipate complex tax filings or those experiencing unanticipated delays in paperwork preparation often utilize this form.

Key Elements of the Form 620EXT for LA 2012

- Corporate Identification: Includes fields for entering identifying information like the business name and Louisiana Revenue Account Number.

- Estimated Tax Amount: Requires the calculation and entry of the expected tax payment due for the filing year.

- Payment Details: Provides instructions for payment methods, ensuring that payments are directed correctly to avoid penalties or misallocations.

State-Specific Rules for the Form 620EXT for LA 2012

Businesses completing this form must adhere to Louisiana-specific tax regulations, which outline the requirements for estimated tax payments and filing extensions. It's crucial for companies to understand that submitting Form 620EXT is not a request for an extension of time to pay the tax due but rather a voucher indicating payment during the granted filing extension period.

Important Terms Related to Form 620EXT for LA 2012

- Filing Extension: A period granted by the Louisiana Department of Revenue allowing corporations additional time to file their tax returns.

- Estimated Tax Payment: A provisional amount paid before the actual tax filing, based on the estimated earnings of the corporation.

- Tax Voucher: A document accompanying payments sent to the revenue department, indicating the purpose and details of the payment.

Penalties for Non-Compliance

Failing to submit the Form 620EXT or the corresponding estimated tax payment on time can result in penalties. These may include interest charges on unpaid taxes and additional late fees. Corporations must be vigilant in adhering to deadlines and ensuring accuracy in their tax documents to avoid costly non-compliance penalties.

Filing Deadlines / Important Dates

The deadline for submitting Form 620EXT and the estimated tax payment generally aligns with the original tax return due date. However, businesses requesting an extension must ensure their payments are made by this date to avoid penalties. Typically, the deadline falls on the 15th day following the close of the corporation's tax year, but exact dates can vary based on business fiscal schedules and state guidelines.