Definition & Meaning

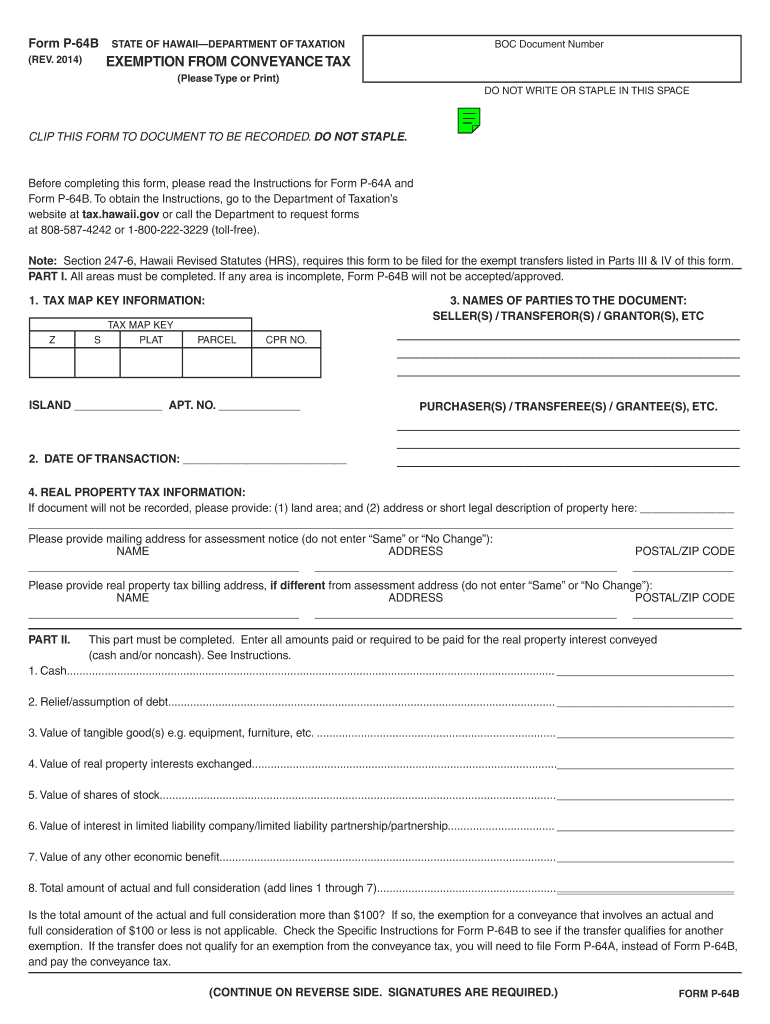

The tax conveyance 2014 form, officially known as Form P-64B, is issued by the State of Hawaii's Department of Taxation. It is utilized to apply for an exemption from conveyance tax on certain real property transactions. The form necessitates comprehensive information regarding the parties involved, the transaction date, property tax details, and the monetary consideration associated with the property transfer. This application form is designed to ease the process for taxpayers who qualify for specific exemptions under state law.

How to Use the Tax Conveyance 2014 Form

To effectively use the tax conveyance 2014 form, it's important to understand its structure and mandatory sections. Primary users must:

- Identify the relevant exemption category applicable to their transaction.

- Accurately fill out details such as the property's location, transaction date, and involved parties.

- Provide documentation that supports the exemption claim, such as prior tax returns or financial statements that prove the eligibility status.

- Ensure all fields are complete and legible, focusing on mandatory sections to avoid processing delays.

For added efficiency, it is recommended to use platforms like DocHub, which can streamline the filling process through its interactive form fields, ensuring accuracy and completeness.

Steps to Complete the Tax Conveyance 2014 Form

Completing the tax conveyance 2014 form requires careful attention to detail and adherence to the following steps:

-

Start with Basic Information: Input the names and contact details of both the buyer and seller.

-

Specify Transaction Details: Record the property address and the transaction date. Ensure accuracy to prevent conflicts with public records.

-

Indicate Exemption Type: Choose from the outlined categories of tax exemptions, ensuring that the selected type matches the criteria of the transaction.

-

Detail Financials: Accurately fill in the property’s actual consideration. Supporting documentation, such as sales contracts or appraisals, should accompany this information.

-

Signatures: Both parties involved in the transaction must sign the form to validate the application. Ensuring the involvement of notaries where required can add legal weight to the document.

-

Review and Submission: Double-check all entered data for correctness and completeness. Submit the form through the accepted channels, which may include mailing options or electronic submissions using platforms like DocHub.

Key Elements of the Tax Conveyance 2014 Form

The form contains several critical elements that require attention for a valid submission:

- Transaction Basics: Includes sections for basic information like property location and involved parties.

- Exemption Categories: Lists various applicable exemptions that the taxpayer can avail of based on their specific transaction.

- Monetary Consideration: Details the financial aspects of the property transfer, such as agreed-upon sales price and any adjustments.

- Signature and Authentication: Ensures legal standing through authorized signatures and, where applicable, notarial acknowledgments.

Careful completion of each section increases the likelihood of a successful application for conveyance tax exemption.

Legal Use of the Tax Conveyance 2014 Form

The tax conveyance 2014 form is legally designed to serve taxpayers seeking exemptions from property conveyance tax in Hawaii. Legal use of the form includes:

- Exemption Claims: Validating the taxpayer's claim to an exemption by appropriately filling the designated sections and providing requisite documentation.

- Compliance with State Law: Ensuring compliance with Hawaii Department of Taxation regulations, which necessitate full disclosure of all relevant transaction details.

- Documentation for Audits: Acting as a record for potential audits or inquiries, showcasing that the taxpayer has met all legal requirements for a conveyance tax exemption.

State-Specific Rules for the Tax Conveyance 2014 Form

The tax conveyance form is subject to state-specific guidelines, influenced by Hawaii's unique tax code:

- Hawaii-Based Transactions Only: The form is applicable solely for transactions involving property located within the state of Hawaii.

- Exemption Eligibility Criteria: Hawaii's Department of Taxation stipulates distinct criteria for exemption eligibility tailored to its residents and property circumstances.

- State-Funded Initiatives: Some exemptions are categorized under state-funded initiatives aimed at encouraging economic growth or housing development within Hawaii.

Understanding these state-specific rules is vital for proper form submission and successful exemption claims.

Penalties for Non-Compliance

Failure to comply with the requirements of the tax conveyance 2014 form can lead to financial and legal repercussions:

- Delayed or Invalidated Exemptions: Errors or omissions may result in the delayed processing or outright invalidation of the exemption application.

- Penalties and Interest: Incorrect or fraudulent filings can attract monetary penalties and interest charges on unpaid taxes.

- Legal Proceedings: Persistent non-compliance might result in legal actions initiated by the state, potentially leading to additional costs and liabilities.

Ensuring compliance with filing instructions mitigates the risk of encountering punitive measures.

Form Variants and Alternatives

While the tax conveyance 2014 form is the definitive document for seeking conveyance tax exemptions in Hawaii, understanding alternatives and older versions is crucial in unique scenarios:

- Related Forms: Variants or complementary documents might be necessary for related transactions, such as accompanying contracts or financial disclosures.

- Adaptations for Updates: Taxpayers must stay informed about updates or alterations to the form, which may affect how exemptions are claimed or processed.

- Historical Versions: Older versions may be referenced for transactions initiated before current standards or where historical tax data is required for audits.

Keeping abreast of different form types and their specific uses can be a useful strategy for effective tax planning and management.