Definition and Purpose of the 2014 Form 990-T

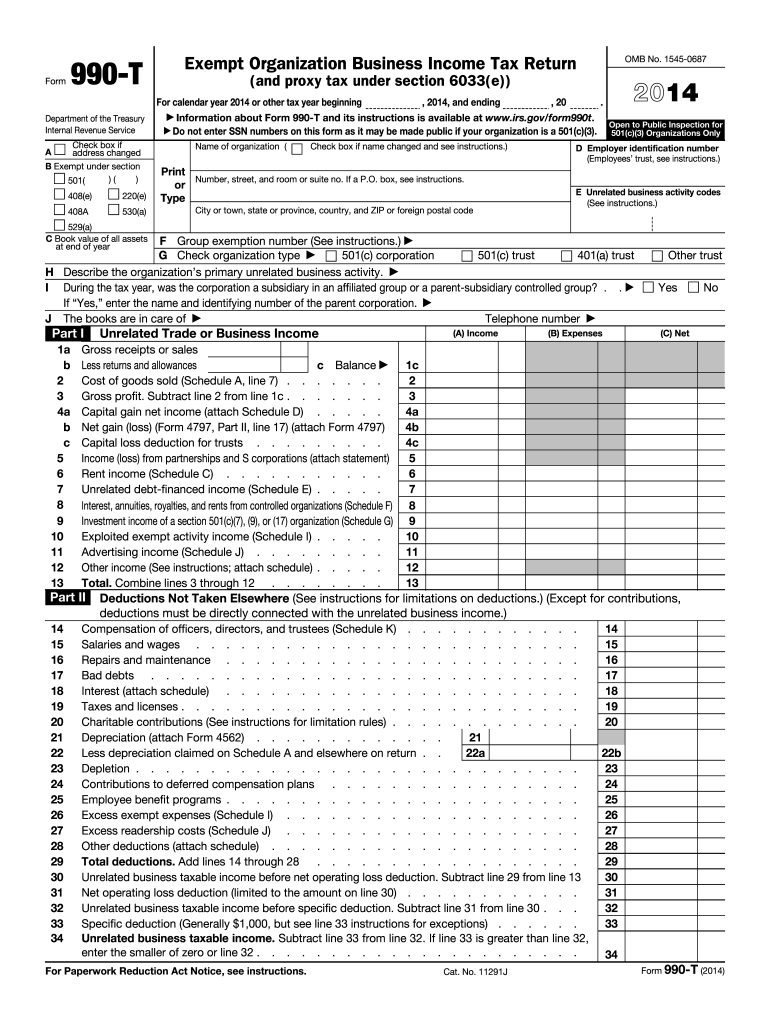

The 2014 Form 990-T, or the Exempt Organization Business Income Tax Return, is a federal tax form utilized by tax-exempt organizations to report unrelated business income and calculate proxy tax under section 6033(e) - i. These organizations must disclose income not directly related to their exempt purpose, ensuring transparency and compliance with U.S. tax laws. The form requires the disclosure of various financial activities, effectively documenting income, expenses, and taxes due on unrelated business income.

Unrelated Business Income

Unrelated business income refers to income derived from a trade or business activity that is not substantially related to the organization's tax-exempt purpose. This type of income is subject to federal income taxation to prevent nonprofit organizations from having competitive advantages over for-profit businesses.

Proxy Tax Details

Proxy tax under section 6033(e) - i focuses on specific tax obligations related to political activities. Organizations must report and pay taxes on lobbying expenditures and political campaign intervention, as outlined by the IRS guidelines.

Obtaining the 2014 Form 990-T

To obtain the 2014 Form 990-T, organizations can access it directly from the IRS website. It is available for download as a PDF document, making it accessible for electronic completion or printing and manual completion if preferred. Tax professionals and organizations can also use tax preparation software compatible with IRS forms to obtain and fill out the form electronically.

Software Compatibility

Several tax preparation software packages, such as TurboTax and QuickBooks, support the 2014 Form 990-T. These software programs offer the advantages of automated data entry, error checking, and electronic filing, streamlining the process and reducing the likelihood of errors.

Steps to Complete the Form

Completing the 2014 Form 990-T involves detailed steps to ensure accurate reporting:

- Organizational Information: Begin by entering the organization's name, address, and employer identification number (EIN).

- Income Reporting: Detail all sources of unrelated business income, including sales, services, and other revenue-generating activities.

- Expense Deduction: Calculate and report all allowable deductions related to generating the unrelated business income.

- Tax Computation: Determine the total tax due based on the calculated net income by applying the appropriate tax rate.

- Schedules and Attachments: Complete any additional schedules required to report specific income and deductions in detail.

- Signatures and Verifications: Ensure the form is signed and dated by an authorized officer of the organization.

Common Challenges

Organizations often face challenges in distinguishing between related and unrelated business income and accurately reporting lobbying expenditures. Consulting a tax professional can assist in navigating these complexities.

Filing Deadlines and Submission Methods

The 2014 Form 990-T is due by the 15th day of the 5th month after the fiscal year ends. Organizations following the calendar year must file by May 15 of the following year.

Submission Options

- Electronic Filing: Use IRS-authorized methods for electronic submission to reduce processing times.

- Mail Submission: Alternatively, paper forms can be sent via U.S. Postal Service or private delivery services to designated IRS addresses.

- In-Person Submission: Rarely used, but forms can be hand-delivered to local IRS offices when applicable.

Penalties for Non-Compliance

Failure to file the 2014 Form 990-T or submitting it with inaccuracies can lead to significant penalties. The IRS imposes fines based on the size of the organization and the duration of non-compliance, emphasizing the importance of accurate and timely filing to avoid financial repercussions.

Penalty Prevention

To mitigate penalties, organizations should maintain precise financial records, regularly review IRS updates for changes in reporting requirements, and consider engaging tax professionals for preparation and review of the form.

Important Terms and Concepts

Understanding key terms is vital for accurate form preparation:

- Unrelated Business Income (UBI): Income from activities not aligned with the organization's exempt purpose.

- Lobbying Expenditures: Costs associated with political advocacy activities, which may be subject to proxy tax.

- Employer Identification Number (EIN): A unique identifier issued by the IRS for organizational tax purposes.

Real-World Scenarios

Several practical scenarios illustrate the application of Form 990-T:

- Nonprofit Museums: Museums hosting unrelated profit-generating events need to report associated income.

- Educational Institutions: Universities that lease property unrelated to educational activities must document this revenue.

- Charitable Organizations: Organizations engaging in substantial political activities must assess lobbying expenditures for proxy tax liability.

Key Takeaways

- Form 990-T is central to maintaining the fiscal transparency of tax-exempt organizations.

- Unrelated business income, proxy taxes, and compliance with IRS deadlines are crucial for avoiding penalties.

- Understanding specific terms and preparing forms accurately is necessary for fulfilling federal tax obligations effectively.