Definition and Purpose of UCLA Form

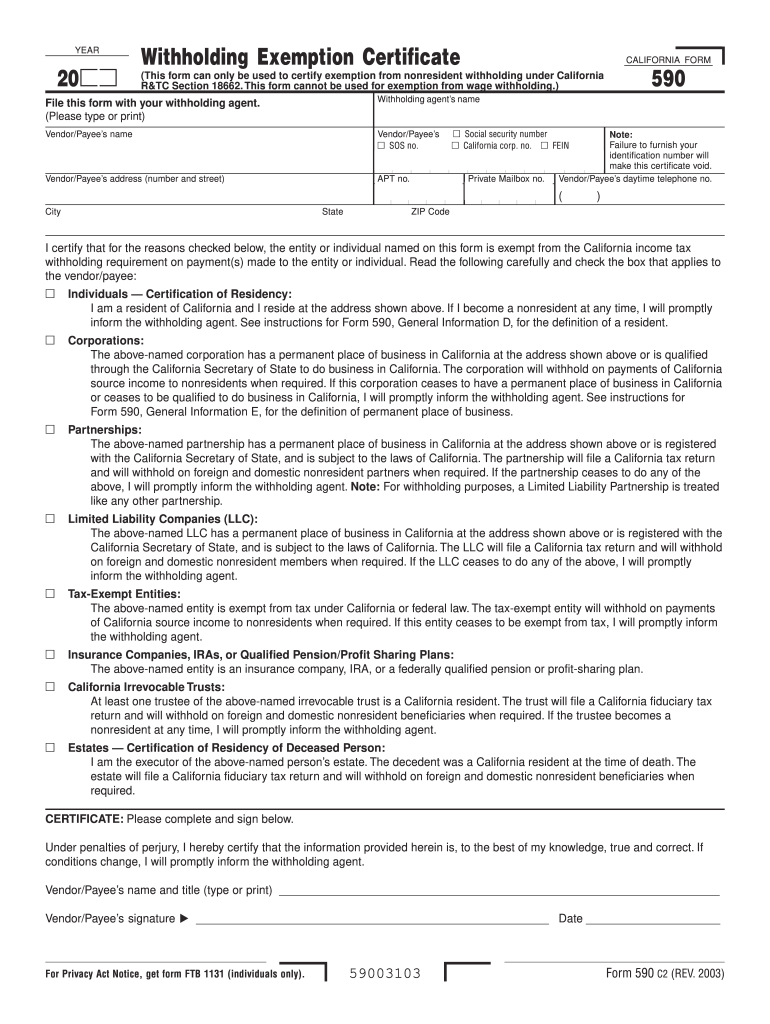

The UCLA Form 590 for 2003, relevant to California's withholding tax laws, is known as the "Withholding Exemption Certificate." Primarily utilized to certify exemption from nonresident withholding, this form is vital for vendors and payees operating in California. Its purpose is to ensure that applicable parties declare their exemption from withholding tax when they fulfill certain conditions that negate the need for such withholdings under California tax regulations.

Steps to Complete the UCLA Form

- Gather Personal Information: Include essential identification details, such as your full name, business name (if applicable), and tax identification number (TIN).

- Residency Status: Declare your residency status. This determines your eligibility for exemption from withholding.

- Reason for Exemption: Specify the grounds for claiming withholding exemption. Common reasons include having a permanent place of business in California or being a resident of the state.

- Signature: Provide your signature to certify the accuracy of the information and your exemption claim. An unsigned form is considered invalid.

How to Obtain the UCLA Form

UCLA's Form 590 for 2003 can be acquired through multiple channels. Traditionally, it is found on the UCLA website or requested through the California Franchise Tax Board for any alterations that remained consistent through 2003. These forms are also often available through companies or contractors involved in transactions requiring such documentation. Ensure you access the correct version to match your specific tax year needs.

Key Elements of the UCLA Form

- Tax Chapter Reference: Highlights the specific tax laws governing nonresident withholding in California.

- Field Descriptions: Each section and field explains the necessary information to be completed by the vendor/payee.

- Nonresident Situations: Details circumstances under which nonresidents can claim exemption (e.g., business structure, permanent California address).

- Responsible Party Information: Section dedicated to identifying who is responsible for understanding changes in eligibility status.

Legal Use of the UCLA Form

Legal compliance is crucial when using the UCLA Form 590. It establishes lawful exemption from withholding taxes for qualifying entities based on their residency or business presence. Misrepresenting information on this form could lead to legal ramifications or penalties. It is advised to consult legal or tax professionals to ensure proper use of the form under current and relevant laws.

Form Submission Methods

- Online Submission: While this may not have been available in 2003, some updates or alternative filing practices may now allow for online submission or consultation for historical inquiries.

- Mail: Forms traditionally submitted through mail should be addressed to the correct department to ensure timely processing.

- In-Person Submission: An option for those who prefer direct delivery or require assistance from the relevant office.

Penalties for Non-Compliance

Failure to comply with the requirements specified in the UCLA Form could result in penalties or fines imposed by the state tax authorities. Non-compliance could include non-disclosure of necessary information, providing false information, or neglecting to update the form when circumstances change. Penalties typically depend on the severity and nature of the non-compliance.

State-Specific Rules for the UCLA Form

California's tax regulations dictate specific enforcement and compliance relating to withholding. The UCLA Form 590 closely follows these state-specific laws to define when an individual or business is subject to withholding or when they can rightfully claim an exemption. Different rules may apply depending on whether the entity is a resident, nonresident, or if they maintain a permanent business in the state, necessitating a thorough understanding of these regulations to use the form appropriately.