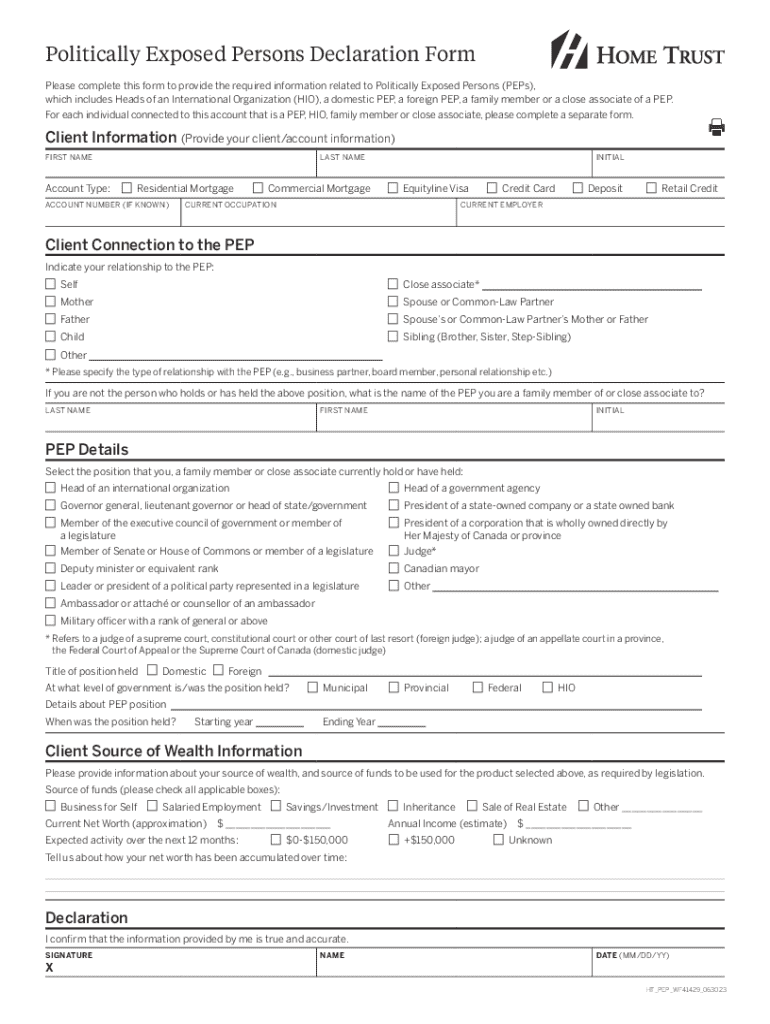

Definition & Meaning

"Guidance for Licensed Financial Institutions on the Risks" serves as a crucial advisory document for financial institutions in the U.S. Its primary purpose is to provide comprehensive insights into the various risks that licensed financial bodies might encounter during their operations. This guidance aids institutions in identifying, assessing, and managing potential threats in areas like compliance, market fluctuations, and operational integrity. By adhering to this guidance, institutions can improve their risk management practices and safeguard their financial and operational health.

How to Use the Guidance for Licensed Financial Institutions on the Risks

Financial entities must systematically approach this guidance to maximize its utility. Begin by thoroughly reading the entire document to understand the overall structure. Identify key sections that pertain specifically to your institution's operational focus, such as regulatory compliance or financial risk exposure. It's essential to involve various departments, including compliance, risk management, and operations, to collaborate in interpreting and implementing the recommendations. Regular internal training sessions can also help ensure that the guidance principles are effectively integrated into daily practices.

Key Elements of the Guidance for Licensed Financial Institutions on the Risks

Several core components form the foundation of this guidance:

-

Risk Identification: The document outlines methodologies to detect potential risks in operational processes.

-

Regulatory Compliance: Comprehensive details on adhering to federal and state regulations.

-

Financial Health: Strategies to maintain liquidity and capital adequacy.

-

Cybersecurity Measures: Instructions for protecting digital assets against cyber threats.

These elements collectively support a robust risk management framework that financial institutions can tailor to their specific needs.

Steps to Complete the Guidance for Licensed Financial Institutions on the Risks

-

Assessment Initiation: Start by gathering cross-departmental insights to evaluate current risk management frameworks.

-

Data Collection: Accumulate relevant data from financial reports, audits, and past incidents to inform risk analysis.

-

Implementation: Apply the recommended strategies and mechanisms from the guidance across your institution.

-

Review and Adjust: Continuously monitor and analyze the effectiveness of implemented strategies, making adjustments as necessary.

These steps ensure that the guidance is actively applied and remains relevant to the evolving financial landscape.

Important Terms Related to Guidance for Licensed Financial Institutions on the Risks

Understanding certain key terms is vital:

-

Compliance: The practice of adhering to laws, regulations, guidelines, and specifications relevant to operations.

-

Liquidity: The ability of an institution to meet its financial obligations as they come due.

-

Market Risk: The possibility of experiencing losses due to changes in market conditions.

-

Operational Risk: Risks arising from inadequate or failed internal processes, personnel, or systems.

Accurate comprehension of these terms facilitates a more nuanced and effective application of the guidance.

Legal Use of the Guidance for Licensed Financial Institutions on the Risks

The legal application of this guidance is to ensure institutions operate within the bounds of established laws and regulations. Financial institutions are legally obligated to report certain types of risks to regulatory bodies and demonstrate compliance with standardized risk management practices. Failure to adhere to these legal requirements could result in penalties, sanctions, or even the revocation of operating licenses.

Examples of Using the Guidance for Licensed Financial Institutions on the Risks

Consider a scenario where a financial institution faces potential exposure due to volatile market conditions. By applying the guidance principles, the risk management team analyzes historical market data and implements hedging strategies to mitigate potential losses. Another example is a bank enhancing its cybersecurity protocols to safeguard customer information, following specific recommendations in the guidance to counteract increasing cyber threats.

Required Documents

Institutions may need various documents to implement the guidance effectively, including:

-

Financial Statements: For internal audits and risk assessments.

-

Regulatory Reports: To ensure compliance with legal standards.

-

Incident Reports: Detailing past security breaches or operational failures for risk evaluation.

-

Insurance Policies: To ascertain coverage against specific risks.

Gathering these documents assists in creating a comprehensive risk management strategy tailored to the institution's unique needs.

Eligibility Criteria

Every licensed financial institution in the U.S. can benefit from this guidance. However, the applicability and relevance may vary depending on:

-

Type of Institution: Banks, credit unions, investment firms, and other financial entities.

-

Operational Scope: Institutions with expansive operations may require a more detailed risk management framework.

-

Regulatory Environment: Institutions operating under specific state regulations may need to align the guidance with local laws.

Analyzing these criteria ensures that the guidance is appropriately scaled to each institution's operational context.

Who Typically Uses the Guidance for Licensed Financial Institutions on the Risks

Primarily, compliance officers, risk management professionals, and senior executives use this guidance. These individuals are responsible for overseeing the institution's adherence to risk management standards and ensuring that all practices align with both the guidance and legal requirements. Additionally, regulatory bodies might use the guidance to assess and audit a financial institution's risk management framework during periodic evaluations.