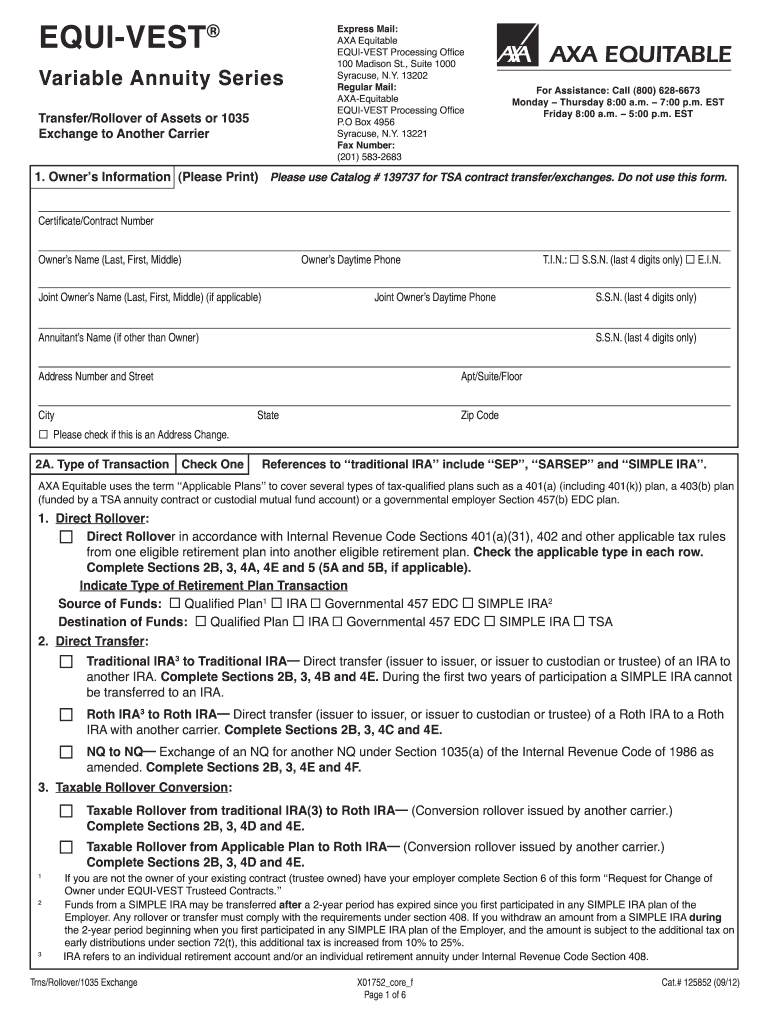

Understanding the Equitable Rollover Form

The equitable rollover form serves as a critical document for transferring retirement assets between different accounts or carriers, maintaining tax-deferred status for the funds involved. It is essential for participants looking to move assets from one plan, such as a 403(b) or an annuity, to another without incurring penalties or tax liabilities. This process adheres to specific IRS regulations ensuring compliance and protection of retirement savings.

Key Features of the Equitable Rollover Form

- Tax Advantages: Utilizing an equitable rollover form allows individuals to avoid triggering taxes on the transferred funds, provided that the rollover is completed correctly. This feature is particularly beneficial for individuals moving retirement savings across plans.

- Multiple Transfer Options: The form facilitates various types of transfers, including direct rollovers and 1035 exchanges, allowing flexibility in how participants manage their retirement funds.

- Ease of Use: The form's design ensures that it is user-friendly, guiding users through the necessary steps to complete their rollover or transfer efficiently.

Detailed Process for Completing the Equitable Rollover Form

- Gather Required Information: Before filling out the equitable rollover form, collect all necessary information related to both the current and receiving accounts, including account numbers, plan details, and personal identification.

- Identify the Type of Transfer: Clearly indicate whether the transfer is a direct rollover, a transfer, or a 1035 exchange, as this impacts the processing and outcome.

- Fill Out the Form: Accurately complete all sections of the form. Essential fields typically include:

- Owner Information: Accurate personal details of the account holder.

- Transaction Types: Specify the nature of the rollover.

- Required Signatures: Ensure that both the owner and relevant plan administrators sign where necessary to authenticate the transaction.

- Submit the Form: The completed equitable rollover form can generally be submitted online, by mail, or in person, depending on the policies of the receiving financial institution.

- Follow Up: After submission, it is advisable to confirm with both the current and new plan administrators that the rollover has been processed successfully.

Important Considerations and Tips

- Consult a Financial Advisor: It is prudent to seek advice from a tax professional or financial advisor before initiating a rollover. They can provide insights into potential tax implications and strategies for managing retirement funds.

- Timely Submissions: Pay attention to any deadlines associated with the submission of the form, such as those pertaining to tax years or plan-specific rules.

- Maintain Documentation: Keep copies of all submitted forms and communications for personal records, as these may be necessary for future reference or audits.

Variants of the Equitable Rollover Form

There are different versions and types of the equitable rollover form tailored to specific retirement plans, such as the equitable 403(b) rollover form or the equitable direct transfer form. Each variant may have slight differences in requirements and processing protocols, so users must ensure they are using the correct form for their specific situation.

Real-World Applications and Examples

- Intermediary Asset Transfers: An employee transitioning between jobs may use the equitable rollover form to facilitate the transfer of their 403(b) retirement savings into their new employer's plan, ensuring that their funds continue to grow tax-deferred.

- Investment Strategy Adjustments: An individual looking to reposition their investment strategy may opt for a 1035 exchange using the equitable rollover form to transfer annuity values into another product that better suits their financial goals, meeting the IRS requirements to avoid penalties.

Understanding the equitable rollover form is vital for effective management of retirement funds, ensuring compliance, and maximizing tax benefits during asset transfers.